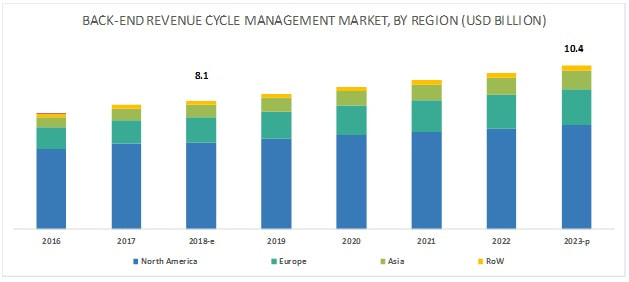

The research report "Back-End Revenue Cycle Management Market by Product and Services (Claim Processing, Denial Management, Payment Integrity), Delivery Mode (On-Premise, Cloud Based), End-User (Payer, Provider (Inpatient, Outpatient)), and Region - Global Forecast to 2027", is projected to reach USD 12.2 billion by 2027 from USD 8.6 billion in 2019, at a CAGR of 4.4%. Growing importance of denials management; To reduce costs and maximize profits, insurance companies are increasingly denying claims as well as coverage to patients being treated for chronic or persistent illnesses. This is putting an extra burden on healthcare providers to manage operating costs, and in turn is supporting the adoption of back-end revenue cycle management solutions (with a growing number of healthcare providers focusing on properly analyzing denied claims and appealing them). Many healthcare providers across the globe still use manual and paper-oriented approaches to manage denials. This results in errors, delayed follow-ups, and miscommunication between healthcare providers and insurance companies. The use of back-end revenue cycle management solutions over manual and paper-oriented approaches can not only help healthcare providers overcome these issues but also help them save significant costs. As a result, the demand for back-end revenue cycle management solutions is expected to increase among end users during the forecast period. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=204439794 Leading Key Players and Analysis: Athenahealth (US), Cerner Corporation (US), Allscripts Healthcare Solutions, Inc. (US), eClinicalWorks (US), Optum, Inc. (US), McKesson Corporation (US), Conifer Health Solutions (US), GeBBs Healthcare Solutions (US), The SSI Group (US), GE Healthcare (US), nThrive (US), DST Systems (US), Cognizant Technology Solutions (US), and Quest Diagnostics (US) are the key players in the Back-End RCM Market. Cerner has a strong foothold in the back-end revenue cycle management market. The company caters to the healthcare technology and financial management needs of its global customers. Cerner focuses on research and development activities, deploying products, and acquisitions to enhance its market presence. For instance, in the past three years, the company deployed more than 15 back-end revenue cycle management solutions across various hospitals, care centers, and medical centers. The acquisition of Siemens Health Services in January 2015 further strengthened its back-end revenue cycle management portfolio. Geographical Analysis in Detailed? The back-end revenue cycle management market is divided into North America, Europe, Asia, and the Rest of the World (RoW). North America is expected to account for the largest share in 2018 owing to factors such as growing HCIT investments in the region and the presence of regulatory mandates. North America is followed by Europe and Asia. The market in Asia is relatively nascent; however, it is projected to be the fastest-growing market during the forecast period. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=204439794 Industry Segmentation: The Services segment to dominate the back-end revenue cycle management market. By product & service, segmented into software and services. The services segment is expected to account for the largest share of the Back-End RCM Market in 2018. The large share of this segment can be attributed to the recurring nature of services such as training and development, installation, software upgrades, consulting, and maintenance. However, due to the need for periodic software upgrades, the software segment is expected to witness the highest growth during the forecast period. The cloud-based systems to register the highest CAGR during the forecast period On the basis of delivery mode, segmented into on-premise and cloud-based systems. The cloud-based segment is expected to register the highest CAGR of the back-end revenue cycle management market during the forecast period. Growth in this segment can be attributed to the comparatively lower capital expenses and operational costs incurred in this model, alongside its scalability, flexibility, and affordability. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=204439794

0 Comments

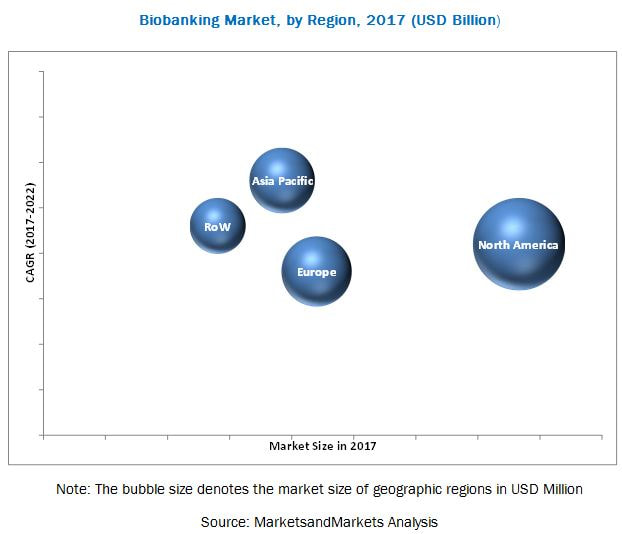

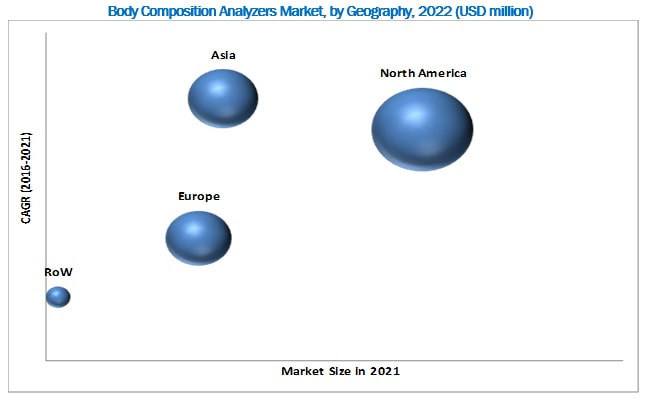

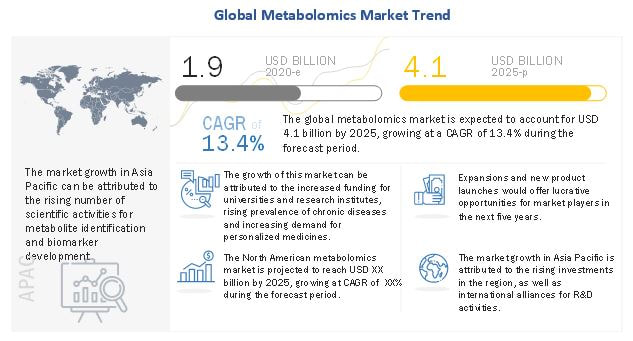

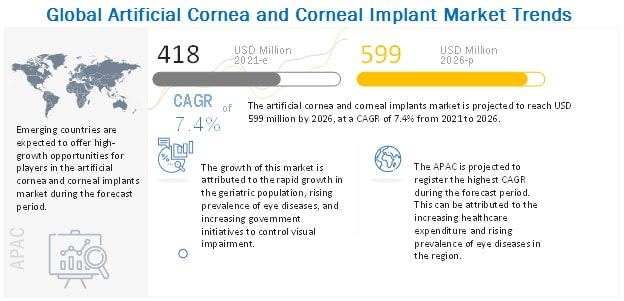

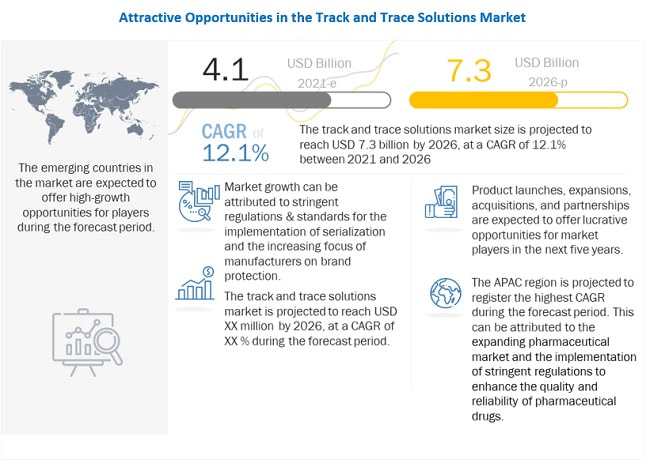

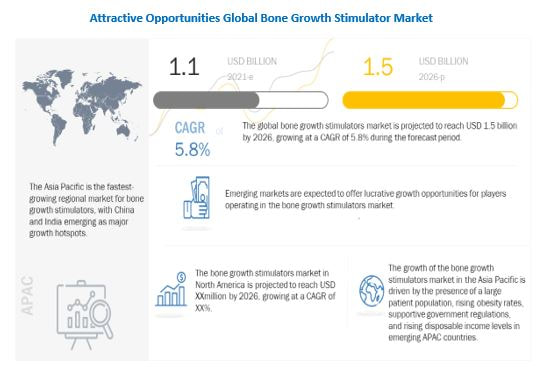

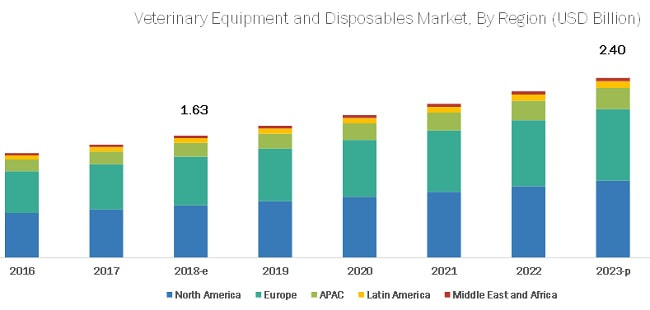

According to the new market research report “Orthodontic Supplies Market by Product (Braces (Removable, Fixed), Brackets (Ligating, Lingual, Metal), Archwires (Ni-Ti, steel), Anchorage, Ligature(Elastomeric, wire), Patient(Adult, Children), Users(Hospitals, Clinics, OTC) – Global Forecast to 2026″, published by MarketsandMarkets™, the Orthodontic Products Market is projected to reach USD 8.3 billion by 2026 from USD 5.4 billion in 2021, at a CAGR of 9.1% during the forecast period. Opportunity: Emerging markets in APAC and RoW; Emerging markets such as China, India, Brazil, and Mexico are expected to offer significant growth opportunities for players in the orthodontic supplies market. Growth in these markets can be attributed to the presence of a large patient population, rising disposable incomes among the middle-class population, and the increasing focus of public and private organizations on increasing the awareness about orthodontic treatments and dental hygiene. To leverage the significant growth opportunities in emerging countries, players are increasingly focusing on undertaking strategic developments to increase their presence in these markets and tap a large number of customers. Along with this, many players are focusing on strategic investments to develop end-to-end digital software solutions with 3D digital scanning, diagnostics, outcome visualization, treatment planning, custom appliances, and custom lab products. For instance, in September 2020, Light Force Orthodontics, a manufacturer of customizable 3D-printed bracket systems, raised USD 14 million from Series B round led by Tyche Partners with follow-on investment from Matrix Partners and AM Ventures. This 3D printing technology helps to create customized braces for each patient. This plays a critical role in significantly reducing the number of visits to orthodontic clinics for the adjustment of braces. These developments are expected to provide a wide range of opportunities for players to capture a large customer base in the orthopedic supplies market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=236529189 The Increasing prevalence of malocclusion, rising emphasis on effective orthodontic treatment and t the initiatives undertaken by governments to increase the awareness about orthodontic treatments are fueling the demand for orthodontic supplies during the forecast period. The orthodontic supplies market includes major Tier I and II suppliers of orthodontic products are 3M (US), Envista Holdings Corporation (US), Dentsply Sirona (US), Align Technology (US), American Orthodontics (US), Rocky Mountain Orthodontics (US), G&H Orthodontics (US), Dentaurum (Germany), TP Orthodontics (US), Great Lakes Dental Technologies (US), DB Orthodontics (UK), Morelli Orthodontics (Brazil), ClearCorrect (US), and Ultradent Products (US). These suppliers have their manufacturing facilities spread across regions such as North America and Europe. COVID-19 has impacted their businesses as well. Due to the pandemic, the orthodontic supplies market experienced short-term negative growth, which can be attributed to a sharp reduction in access to hospital and dental clinics and the temporarily shutdown of orthodontic clinics. Orthodontic practices around the globe are facing challenges amid the pandemic. The adoption of strict protocols outside and inside dental clinics, increasing usage of teleorthodontics in case of urgent appointments, and opting for minimal orthodontic treatment procedures by many orthodontic clinics are likely to have a positive impact on the market. Moreover, post lockdown, as dental practices reopen, it is expected that patient volumes are anticipated to rebound at a higher pace. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=236529189 Demand for invisible braces among the target population due to their aesthetic benefits drives the growth of removable braces Removable braces offer advantages over traditional braces, including easy removal of braces, reduced risk of periodontal diseases & tooth decay, and enhanced comfort. Factors such as strong focus on product innovation by players and growing awareness about the benefits associated with removable braces and the growing demand for invisible braces among teens and adults due to their aesthetic benefits is augumenting the growth of removable braces. Asia Pacific likely to emerge as the fastest growing orthodontic supplies market, globally Geographically, the emerging Asian countries, such as China, India, Japan and Singapore, are offering high-growth opportunities for market players. The Asia Pacific point of care market is projected to grow at the highest CAGR of 10.8% from 2021 to 2026. Expansion of healthcare infrastructure and increase in disposable personal income, increase patient population with malocclusion and tooth decay are factors likely to support the growth of market in the region. Moreover, the growing focus toward aesthetics products among adults and emergence of small manufacturers in the market are driving the growth of the APAC orthodontic supplies market. Prominent players in this market are 3M (US), Envista Holdings Corporation (US), Dentsply Sirona (US), Align Technology (US), Rocky Mountain Orthodontics (US), G&H Orthodontics (US), Dentaurum (Germany), TP Orthodontics (US), Great Lakes Dental Technologies (US), DB Orthodontics (UK), among others. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=236529189  According to the new market research report “Biobanking Market by Product and Service(Equipment, Consumables, Services, Software), Sample Type (Blood Products, Human Tissues, Cell Lines, Nucleic Acids), Application( Regenerative Medicine, Life Science, Clinical Research) – Global Forecast”, published by MarketsandMarkets™, the biobanking devices market is expected to reach USD 2.69 Billion by 2022 from USD 1.85 Billion in 2017, at a CAGR of 7.8%. Regenerative medicine applications for biobanking market will drive the market; The Biobanking Devices Market plays an integral role in advancing biomedical and translational research, through the collection and preservation of biological samples, such as blood, tissues, and nucleic acids, which are then made available for use in research to discover disease-relevant biomarkers; this is further used for diagnosis, prognosis, and predicting drug responses. Growth in the number of research activities in this segment forms a major driver for the market. The availability of government funding for regenerative medicine, stem cell therapeutics, and cell & gene therapy is supporting research activities in this segment. Apart from this, the increasing trend of cord blood banking will also aid growth of this market segment. Future prospects including advancements in orthopedic procedures with the use of stem cells are expected to further support market growth for regenerative medicine. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=594 The Factors driving the growth of this market include the increasing number of genomics research activities for studying diseases; advances in biobanking and the growing trend of conserving cord blood stem cells of newborns; government & private funding to support regenerative medicine research; and the growing need for cost-effective drug discovery and development. The equipment segment is expected to dominate the biobanking devices market. By product and service, the biobanking market is segmented into equipment, consumables, services, and software. The equipment segment is expected to dominate the global market in 2017. Rising number of biobanks and the increasing number of biospecimens are factors increasing the demand for biobanking equipment. Blood products are estimated to command the largest biobanking devices market share. The biobanking market is segmented by sample type into blood products, human tissues, nucleic acids, human waste products, cell lines, and biological fluids. In 2017, the blood products segment is expected to account for the largest share of the market, by sample type. Rising incidence of blood disorders and the increasing demand for various types of blood products across the globe are driving the growth of this segment. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=594 North America is expected to account for the largest share of the biobanking devices market. Based on region, the biobanking market is segmented into North America, Europe, Asia-Pacific, and Rest of the World (RoW). North America is expected to dominate the market in 2017, this is attributed to factors like increasing research activities in regenerative medicine, cell and gene therapy; growing interest in personalized medicine and biomarker discovery; increasing number of biotechnology and pharmaceutical companies; and rising investments in genomics and proteomics research in the region as compared to other regions. Key players in the biobanking market include Thermo Fisher Scientific Inc. (U.S.), Tecan Group Ltd. (Switzerland), Qiagen N.V. (Germany), Hamilton Company (U.S.), Brooks Automation (U.S.), TTP Labtech Ltd (U.K.), VWR Corporation (U.S.), Promega Corporation (U.S.), Worthington Industries [(Taylor Wharton, U.S.)], Chart Industries (U.S.), Becton, Dickinson and Company (U.S.), Merck KGaA (Germany), Micronic (Netherlands), LVL Technologies GmbH & Co. KG (Germany), Panasonic Healthcare Holdings Co. Ltd (Japan), Greiner Bio One [Greiner Holding AG, Austria)], Biokryo GmbH (Germany), Biobank AS (Norway), Biorep Technologies Inc. (U.S.), Cell & Co Bioservices (France), RUCDR infinite biologics (U.S.), Modul-Bio (France), CSols Ltd (U.K.), Ziath (U.K.), and LabVantage Solutions Inc. (U.S.). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=594  According to the new market research report “Body Composition Analyzers Market by Product (Bio-impedance analyzer/DEXA/Skinfold calipers/ADP/Hydrostatic weighing), & End-users (Hospitals/Fitness & wellness centers/Academic & Research Center/Home-users) – Analysis & Global Forecast”, published by MarketsandMarkets™, is poised to reach USD 668.16 Million, growing at a CAGR of 12.7%. The Body composition analysis is the process to evaluate the amount of fat, muscle, and bone in the body. It gives the precise measurement of body fat in relation to lean body mass. Evaluation of body composition is essential in order to determine the risks associated with high or low levels of body fat. The growth of the overall body composition analyzers market can be contributed to rise in obese population across the globe, growing health and fitness consciousness among people, increasing government initiatives to encourage physical activity and technological advancements. In the coming years, the body composition analyzers market is expected to witness the highest growth rate in the Asia-Pacific region. North America is expected to account for the largest share of the global body composition analyzers market. However, inconsistency in the accuracy of different analyzers and high cost of equipment is likely to restrain the growth of the market during the forecast period. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=248209133 Increasing adoption of body composition analyzers to assess the nutritional status in patients is driving the growth of this market; Hospitals; In hospitals, body composition analysis is majorly used for the diagnosis of osteoporosis. For this application, DEXA is utilized to measure bone density for diagnosing osteoporosis and assessing the risk of developing fractures. As a result, the growing prevalence of osteoporosis is expected to increase the adoption of DEXA in various hospitals. Moreover, various hospitals across the globe, such as the Jackson Hospital (U.S.), Ramsay Health Care (U.K.), Apollo Hospitals (India), and Elkhart General Hospital (U.S.), have now included body composition testing as a part of their patient care and wellness programs. Such developments are expected to support the growth of this end-user segment in the coming years Fitness clubs and wellness centers; Over the past few years, the number of fitness clubs has increased significantly as a result of the growing focus on health and fitness among people. At gyms and wellness centers, body composition analyzers not only measure the amount of body fat for weight loss but also provide complete body composition assessment to maintain health. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=248209133 The global body composition analyzers market is segmented on the basis of product type, end users and region. Based on product, the market is segmented into bio-impedance analyzer, dual energy X-ray absorptiometry (DEXA), skin fold Calipers, air displacement plethysmography (ADP) and hydrostatic weighing. The bio-impedance analyzer is expected to account for the largest share of the body composition analyzers market, by product in 2016 and is expected to grow at highest CAGR. This large share can be attributed to the simplicity, low cost, and better accuracy as compared to other body composition analyzers. Based on end users, the market is segmented into hospitals, fitness clubs and wellness centers, academic and research centers. In 2016, hospitals segment is estimated to account for the largest share of the body composition analyzer market, by end users in 2016 and is expected to grow at highest CAGR. The growth of this segment can be attributed to the rise in osteoporosis cases, increasing adoption of body composition analyzers to assess the nutritional status in patients and increasing health consciousness among masses. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=248209133 basis of region, the Body Composition Analyzers Market is divided into North America, Europe, Asia-Pacific, and the Rest of the World (RoW). In 2016, North America is expected to account for the largest share of the body composition analyzer market. Its large share can be attributed to rising obesity rates and increasing health clubs and fitness centers in the U.S. However, the Asia-Pacific market is slated to grow at the highest CAGR during the forecast period due to rising trend of overweight and obesity in China, and foothold of local players in Japan. The major players in body composition analyzers market include InBody Co., Ltd (South Korea), Tanita Corporation (Japan), Omron Corporation (Japan), Hologic, Inc. (U.S.) and GE Healthcare (U.S.) among others.  According to the new market research report “Metabolomics Market by Product (GC,UPLC, CE, Surface based Mass Analysis), Application (Biomarker Discovery, Drug Discovery, Functional Genomics), Indication (Cardiology, Oncology, Inborn Errors), End User (Academic Institute, CROs) – Global Forecast to 2025″, published by MarketsandMarkets™, the global Metabolomics Technology Market size is projected to reach USD 4.1 billion by 2025, at a CAGR of 13.4% between 2020 and 2025. Opportunity:Biomarker development; Metabolomics is used to identify new biomarkers through bioinformatics tools, which indicate the changes in the physiological state of a cell or tissue. Biomarkers are important for developing in-vitro diagnostic tools, environmental toxicology screening methods, and drug discovery and development techniques. The omics revolution of the last decade has increased the application of metabolomics in biomedical research. As a result of these technological developments, new biomarkers are being regularly discovered. These biomarkers are required in medical sciences to better define and diagnose diseases, predict adverse drug events, and identify patient groups who would benefit from specific treatments. Moreover, in the near future, identifying biomarkers related to safety, sensitivity, and resistance to commercially available drugs will present significant growth opportunities for the metabolomics market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=900 The major factors driving the growth of this market are the growing R&D expenditure in the pharmaceutical & biopharmaceutical industry, growing demand for personalized medicine and increasing use of metabolomics in toxicology testing are driving the growth of the global metabolomics industry. Separation tools accounted for the largest share in the metabolomics market in 2019. Based on the product & service, the market is categorized into metabolomics instruments and bioinformatics tools and services. The metabolomics instruments segment is further categorized into separation tools and detection tools. Separation tools is sub segmented into gas chromatography, high-performance liquid chromatography, ultra-performance liquid chromatography, and capillary electrophoresis. Similarly, detection tools are categorized into nuclear magnetic resonance (NMR) spectroscopy, mass spectrometry (MS), and surface-based mass analysis. The separation tools segment accounted for the largest share of the market in 2019. The widespread use of separation tools in research activities, increase in funds for research projects, development of innovative technologies in these tools, and their extensive application in the drug discovery process are fueling the growth of this segment. Cancer accounted for the largest share in the market in 2019 Based on indication, the metabolomics market has been segmented into into cancer, cardiovascular disorders, neurological disorders, metabolic disorders, inborn errors of metabolism, and other indications. The cancer segment is expected to account for the largest market share in 2020, with the highest growth rate as well. This can primarily be attributed to the growing use of metabolomics in cancer research and increasing number of cancer patients. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=900 Academic and research institutes accounted for the largest share the metabolomics market in 2019 Based on end user, the market has been segmented into academic and research institutes, pharmaceutical & biotechnology companies, contract research organizations, and other end users. The academic and research institutes segment accounted for the largest share of the market in 2019. The increasing number of research activities in the field of metabolomics and funding to the academic and research institutes to conduct metabolomics research are the factors responsible for the largest share of the segment. Biomarker Discovery accounted for the largest share of the metabolomics market Based on application, the Metabolomics Technology Market has been segmented into biomarker discovery, drug discovery, toxicology testing, nutrigenomics, functional genomics, personalized medicine, and other applications. Biomarker discovery accounted for the largest share of the market in 2019. The growing implications of metabolic biomarkers to access the pathophysiological health status of patients are expected to drive market growth. North America accounted for the largest share of the metabolomics market in 2019. Based on the region, the global Metabolomics Technology Market is segmented into North America, Europe, the Asia Pacific, Latin Ametica and Middle East & Africa. In 2019, North America accounted for the largest share of the metabolomics technologies market. The large share of the North America region can be attributed to the presence of major players operating in the market in the US, growing biomedical research in the US, and rising preclinical activities by CROs and pharmaceutical companies in the region. The metabolomics market is dominated by a few globally established players such as Waters Corporation (US), Agilent Technologies (US), Shimadzu Corporation (Japan), Thermo Fisher Scientific (US), Danaher Corporation (US), Bruker Corporation (US), PerkinElmer (US), Merck KGaA (Germany), GE Healthcare (US), Hitachi High-Technologies Corporation (Japan), Human Metabolome Technologies, Inc. (Japan), LECO Corporation (US), Metabolon, Inc. (US), Bio-Rad Laboratories (US), Scion Instruments (US), DANI Instruments S.p.A. (Italy), GL Sciences (Japan), SRI Instruments (US), Kore Technology Ltd. (UK), and JASCO, Inc. (US) among others. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=900  According to the new market research report “Artificial Cornea Implant Market by Type (Human Cornea, Artificial Cornea), Transplant Type (Penetrating Keratoplasty, Endothelial Keratoplasty), Disease Indication, End Users (Hospitals, Specialty Clinics & ASCs) – Global Forecast to 2026″, published by MarketsandMarkets™, the global Artificial Cornea Implant Market is projected to reach USD 599 million by 2026 from USD 418 million in 2021, at a CAGR of 7.4% from 2021 to 2026. Opportunity: Shortage of corneal donors; There is a significant requirement of corneal donors across the globe, as approximately 10 million people are in need of corneal transplants. Densely populated counties such as India suffer from a significant shortage of donor corneas, and there is a waiting period of more than six months for corneal transplants among patients suffering from corneal blindness. Approximately 6.8 million people in the country have poor vision in one eye, and nearly one million people have poor vision in both eyes due to corneal disorders. It was estimated that by the end of 2020, India would suffer from 10.6 million cases of unilateral corneal blindness. In 2019, around 120,000 people were affected by corneal blindness. Around 250,000 corneas are needed annually in the country; however, the total number of corneas donated each year is around 25,000. The high burden of corneal blindness, coupled with a shortage of corneal donors, is expected to offer high-growth opportunities to manufacturers of corneal implants. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=182165973 The Corneal Implant Market growth is largely driven by the The growing geriatric population and the rising prevalence of eye diseases are the major drivers for the artificial cornea and corneal implants market. The increasing prevalence of eye disorders and government initiatives to control visual impairment are further boosting the market growth. The artificial cornea segment is projected to witness fastest growth during the forecast period On the basis of type, the artificial cornea and corneal implants market is segmented into human cornea and artificial cornea. The artificial cornea segment is projected to witness fastest growth during the forecast period. An artificial corneal transplant, also known as keratoprosthesis (KPro), enables the restoration of vision in conditions wherein the cornea and the eye surface is affected or damaged. The scarcity of human eye donors has resulted in the development of innovative solutions such as artificial corneas. Additionally, individuals with a history of multiple previous graft failures, Stevens-Johnson syndrome, chemical burns, severe dry eyes, congenital aniridia, or limbal stem cell deficiency are indications for KPro. One of the commonly used keratoprosthesis is Boston Keratoprosthesis (Boston KPro). To date, over 15,000 Boston KPro have been implanted across the globe. Penetrating keratoplasty segment accounted for the largest share of artificial corneal implant market in 2020. On the basis of transplant type, the Artificial Cornea Implant Market is segmented into penetrating keratoplasty, endothelial keratoplasty, and other transplants (including anterior lamellar keratoplasty (ALK) and keratoprosthesis). In 2020, the penetrating keratoplasty segment accounted for the largest share of the global artificial cornea and corneal implants market. The large share of this segment can be attributed to the rising number of people suffering from eye disorders such as infectious keratitis and injury of the eyeball. In 2020, Fuchs’ dystrophy segment accounted for the largest share of artificial cornea market On the basis of disease indication, the corneal implants market is segmented into fungal keratitis, Fuchs’ dystrophy, keratoconus, and other diseases. In 2020, the Fuchs’ dystrophy segment accounted for the largest share of artificial cornea and corneal implant market. The rising incidence of the disease and the growing awareness among people regarding early disease diagnosis are the key factors driving the growth of this segment. In 2020, hospitals segment accounted for the largest share of corneal implant market Based on end users, the artificial cornea and corneal implants market is segmented into hospitals and specialty clinics and ambulatory surgery centers (ASCs). In 2020, hospitals segment accounted for the largest share of artificial corneal implant market. The rising prevalence of eye disorders, growth in the geriatric population, increasing awareness about the innovative artificial corneal technology, the willingness of patients to spend more on advanced treatments, and the growing number of hospitals in developing countries such as India, China, and Brazil are some of the key factors driving the growth of the artificial cornea and corneal implants market for hospitals. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=182165973 Asia Pacific is expected to witness fastest growth during the forecast period of 2021–2026. Geographically, the artificial cornea and corneal implant market is segmented into North America, Europe, the Asia Pacific, Latin America, and Middle East & Africa. Asia Pacific is projected to witness highest CAGR during the forecast period of 2021–2026. The Asia Pacific forms the most lucrative region in the artificial cornea and corneal implants market, owing to the large population in countries such as China and India, rapid growth in the geriatric population, improving healthcare infrastructure, growing per capita income, and the rising focus of key market players on this region. The prominent players in artificial cornea implant market are AJL Ophthalmic (Spain), CorneaGen Inc. (US), Addition Technology, Inc. (US), LinkoCare Life Sciences AB (Sweden), Presbia plc (Ireland), Mediphacos (Brazil), Aurolab (India), Cornea Biosciences (US), DIOPTEX GmbH (Austria), EyeYon Medical (Israel), Massachusetts Eye and Ear (US), Florida Lions Eye Bank (US), SightLife (US), Advancing Sight Network (US), San Diego Eye Bank (US) and L V Prasad Eye Institute (LVPEI, India). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=182165973  According to the new market research report “Track and Trace Solutions Market by Product (Plant Manager, Checkweigher, Barcode Scanner, Monitoring), Technology (2D Barcode, RFID), Application (Serialization, Aggregation, Reporting), End User (Pharma, Food, Medical Devices) – Global Forecast to 2026″, published by MarketsandMarkets™, is projected to reach USD 7.3 billion by 2026 from USD 4.1 billion in 2021, at a CAGR of 12.1% during the forecast period. Opportunities: Remote authentication of products; Traditional brand protection technologies such as anti-theft and authentication are intended to protect individual items rather than safeguard the entire supply chain. There is a high possibility of fake products being introduced at any stage in the supply chain. To combat counterfeiting and identify massive product items, a solution with automatic and non-line-of-sight capabilities is required. The demand for technologies with modular designs, which fit enterprise needs, has increased in the last few years. For instance, track and trace technologies based on RFID maintain an electronic pedigree that records the transaction information of products within the supply chain. This approach proved to be a standout for protecting the supply chain against infiltration, theft, and fraud and supporting remote authentication in the brand protection supply chain. Technologies that are scalable from a single production line to a multi-facility/multi-line infrastructure while minimizing the initial investment are projected to gain attention in the coming future. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=158898570 “The Software segment accounted for the largest market share in 2020.” Based on products, the market is segmented into software, hardware components, and standalone platforms based on product. The software segment accounted for the largest share—60.1%—of the track and trace solutions market in 2020. Market growth is largely driven by the increasing awareness about secure packaging, the rising number of counterfeit drugs and related products, and growing awareness of brand protection. In addition, regulatory compliance is further supporting the growth of this market. The standalone platforms segment is expected to register the highest CAGR of 15.9% during the forecast period. The growth in this market is mainly attributed to the stringent government regulations for implementing serialization and UDI codes in the pharma and medical device industry, increasing pressure on pharmaceutical companies to adopt serialization, and increasing demand for standalone platforms to reduce the serialization implementation timeframe. “The Serialization solutions segment accounted for the largest market share in 2020.” Based on application, the track and trace solutions market is segmented into serialization solutions; aggregation solutions; and tracking, tracing, and reporting. The serialization solutions segment accounted for the largest share—62.3%—of the applications market. This segment is projected to grow at a CAGR of 12.0% during the forecast period to reach USD 2,560.9 million by 2026. Stringent regulations for the implementation of serialization solutions in packaging and supply chain applications drive this segments growth. The tracking, tracing and reporting segment is expected to register the highest CAGR of 16.1% during the forecast period owing to the increasing number of regulations such as DSCSA, UDI, and Medical Device Reporting (MDR) for medical devices and pharmaceutical products. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=158898570 “The 2D Barcode segment accounted for the largest market share in 2020.” Based on technology, the track and trace solutions market is segmented into linear barcodes, 2D barcodes, and radiofrequency identification (RFID). The 2D barcodes segment accounted for the largest share of 76.2% of the technology market in 2020. This segment is projected to grow at a CAGR of 12.4% to reach USD 5,641.3 million by 2026. The large share of the 2D barcodes technology segment can be attributed to the increasing use of 2D barcodes in the packaging industry. They have higher data storage capacities than linear barcodes and contain larger amounts of data with fewer variations in image size. The RFID segment is expected to register the highest CAGR of 13.7% during the forecast period due to the growing demand for these systems in automated pharmaceutical distribution and medical devices due to low labor costs and improved visibility & planning. “The Pharmaceutical and Biopharmaceutical Company segment accounted for the largest market share in 2020.” Based on technology, the track and trace solutions market is segmented into linear barcodes, 2D barcodes, and radiofrequency identification (RFID). The 2D barcodes segment accounted for the largest share of 76.2% of the technology market in 2020. This segment is projected to grow at a CAGR of 12.4% to reach USD 5,641.3 million by 2026. The large share of the 2D barcodes technology segment can be attributed to the increasing use of 2D barcodes in the packaging industry. They have higher data storage capacities than linear barcodes and contain larger amounts of data with fewer variations in image size. The RFID segment is expected to register the highest CAGR of 13.7% during the forecast period due to the growing demand for these systems in automated pharmaceutical distribution and medical devices due to low labor costs and improved visibility & planning. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=158898570 “North America was the largest regional market for track and trace solutions market in 2020” Geographically; divided into five major regions, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2020, North America accounted for the largest share of 42.9% of the global market, followed by Europe (33.5%). The presence of developed healthcare systems in the US & Canada; the presence of many pharmaceutical & biotechnology companies and medical device manufacturers; stringent regulations regarding serialization; and the growing medical devices market are major factors driving market growth in North America. Asia Pacific (APAC) is the fastest-growing market and is projected to grow at the highest CAGR of 13.8% for track and trace solutions. Growing regulatory requirements in the healthcare industry to comply with manufacturing and distribution practices, the rising number of pharmaceutical and biotechnology companies, and the significant economic development in emerging Asia Pacific countries such as China and India are the major factors driving the demand for track and trace solutions in the APAC region. Some of the prominent players in the track and trace solutions market are OPTEL GROUP (Canada), Mettler-Toledo International Inc. (US), Systech International Inc. (US), TraceLink Inc. (US), Antares Vision (Italy), SAP (US), Xyntek Inc. (US), SEA Vision Srl (Italy), Syntegon (Germany), Körber Medipak Systems AG (Switzerland), Siemens AG (Germany), Uhlmann Group (Germany), JEKSON VISION (India), Videojet Technologies, Inc. (US), Zebra Technologies Corporation (US), Axway Inc. (US), ACG Worldwide (India), Laetus GmbH (Germany), and WIPOTEC-OCS (Germany).  According to the new market research report “Bone Growth Stimulator Market by Product (Device (Implant, External), Bone Morphogenetic Protein, PRP), Application (Spinal Fusion, Delayed Union, Non-union Bone Fracture, Maxillofacial Surgery), Care Setting (Hospital, Homecare) – Global Forecasts to 2026″, published by MarketsandMarkets™, the global bone growth stimulation devices market is projected to reach USD 1.5 billion by 2026 from USD 1.1 billion in 2021, at a CAGR of 5.8% during the forecast period. Growth Driver: Growing patient preference for non-invasive and minimally invasive surgical treatments The demand for minimally invasive procedures has witnessed a significant increase owing to the advantages offered by these procedures over traditional treatment procedures. The key advantages of minimally invasive procedures include fewer operative complications, shorter hospitalization, less pain, smaller and more cosmetic incisions, lower risk of infection, reduced postoperative care, and quicker recovery. Minimally invasive procedures make use of advanced technologies to diagnose and treat various diseases, including cancer. These procedures are used as an effective approach for removing cancer tumors and lymph nodes without scarring. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=82341383 The Rise in the global incidence of AKI and increase in the demand for effective renal replacement therapy among ICU patients and initiatives undertaken by governments to increase the awareness about BGS therapy along with the increase in the launch of advanced BGS system area anticipated to fuel the bone growth stimulation devices market growth during the forecast period. These suppliers have their manufacturing facilities spread across regions such as North America and Europe. COVID-19 has impacted their businesses as well. The growing patient preference for non-invasive and minimally invasive surgical treatments, the rising prevalence of target conditions, and the growing number of sports and accident-related orthopedic injuries are the key factors driving the growth of the bone growth stimulators market. However, limited medical reimbursement for bone stimulation devices, high treatment costs associated with BMP and PRP products, and side effects associated with BMP-based orthopedic treatment are the key factors restraining the growth of bone growth stimulation devices market. The growing demand for orthopedic injuries to support the market growth during the forecast period. The significant rise in demand for BGS in the treatment of orthopedic patients. Moreover, the development and commercialization of BGS products also support Bone Growth Stimulator Market growth. Furthermore, many companies are expanding their BGS (PRP products) product portfolios. Similarly, the companies are also expanding their presence in the market. For instance, in 2021, Orthofix entered into an exclusive license agreement to commercialize the innovative portfolio of IGEA’s bone, cartilage, and soft tissue stimulation products in the US and Canada. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=82341383 Asia Pacific likely to emerge as the fastest-growing BGS market. Geographically, the emerging Asian countries, such as China, India, Japan and Singapore, are offering high-growth opportunities for Bone Growth Stimulator Market players. The Asia Pacific point of care market is projected to grow at the highest CAGR of 8.7% from 2021 to 2026. Expansion of healthcare infrastructure and increase in disposable personal income, increase patient population with orthopedic disease, are factors likely to support the growth of market in the region. The prominent players operating in the global Bone Growth Stimulator Market include Orthofix Medical, Inc. (US), DJO Finance, LLC (US), Zimmer Biomet (US), Bioventus LLC (US), Medtronic plc (Ireland), Stryker (US), DePuy Synthes (US), Arthrex, Inc. (US), Isto Biologics (US), Terumo Corporation (Japan), Ember Therapeutics, Inc. (US), Ossatec Benelux Ltd. (Netherlands), Altis Biologics (Pty) Ltd. (South Africa), Regen Lab SA (Switzerland), ITO Co., Ltd. (Japan), Elizur Corporation (US), BTT Health GmbH (Germany), Stimulate Health Inc. (Canada), VQ OrthoCare (US), Kinex Medical Company, LLC (US), Fintek Bio-Electric Inc. (Canada), Biomedical Tissue Technologies Pty Ltd. (Germany), T-Biotechnology (Turkey), DrPRP America LLC (US), Ivy Sports Medicine, LLC (US), Glofinn Oy (Finland), and REMI GROUP (India) among others. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=82341383  According to the new market research report "Cell Culture Market by Product (Consumables (Media, Serum, Reagent, Vessels), Equipment (Bioreactor, Centrifuge, Incubator)), Application (Vaccines, mAbs, Diagnostics, Tissue Engineering), End User (Pharma, Biotech, Hospital) - Global Forecast to 2026", published by MarketsandMarkets™, the global market is projected to reach USD 41.3 billion by 2026 from USD 22.8 billion in 2021, at a CAGR of 12.6 % between 2021 and 2026. Browse in-depth TOC on "Cell Culture Market" 690 – Tables 43 – Figures 490 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=559 The growth of this market is majorly driven by the growing awareness about the benefits of cell-based vaccines, increasing demand for monoclonal antibodies (mAbs), funding for cell-based research, growing preference for single-use technologies, the launch of advanced cell culture products, and the growing focus on personalized medicine. On the other hand, the high cost of cell biology research is restraining the growth of this market. The consumables segment accounted for the largest share of the product segment in the cell culture market in 2020. Based on product, the market is segmented into equipment and consumables. The cell culture equipment market is further segmented into supporting equipment, bioreactors, and storage equipment. The cell culture consumables market is segmented into sera, media & reagents, vessels, and bioreactor accessories. In 2020, the consumables segment accounted for the largest share of the market. The large share and high growth of the consumables segment can be attributed to the repeated purchase of consumables and an increase in funding for cell-based research. The biopharmaceutical production segment accounted for the largest share of the application segment in the cell culture market in 2020. Based on application, the market is categorized into biopharmaceutical production, diagnostics, drug discovery & development, tissue engineering & regenerative medicine, and other applications. The biopharmaceutical production segment is further divided into monoclonal antibody production, vaccine production, and other therapeutic protein production. The tissue engineering & regenerative medicine segment is further divided into cell & gene therapy and other tissue engineering & regenerative medicine applications. The biopharmaceutical production segment is estimated to grow at the highest CAGR of 14.1% during the forecast period. The high growth of this segment is attributed to the commercial expansion of major pharmaceutical and biotechnology companies, the increasing demand for mAbs, and the growing regulatory approvals for the production of cell culture-based vaccines. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=559 The Asia Pacific region is the fastest-growing region of the cell culture market in 2020. Based on the region, the global market has been segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa. The Asia Pacific market is estimated to register the highest CAGR during the forecast period. Government initiatives for research on stem cell therapy, growing geriatric population, the rising prominence of regenerative medicine research, increasing number of researchers in Japan, growth of preclinical/clinical research in China, favorable changes in foreign direct investment (FDI) regulations in the pharmaceutical industry in India, and growth of the pharmaceutical & biopharmaceutical sectors in South Korea are the major factors contributing to the growth of the market in the Asia Pacific. Key players in the cell culture market include Thermo Fisher Scientific, Inc. (US), Merck KGaA (Germany), Danaher Corporation (US), and Sartorius AG (Germany). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=559  According to a new market research report “Veterinary Equipment and Disposables Market by Product (Consumables, Anesthesia Machines, Ventilators, Patient Monitoring, Oxygen Masks, Infusion Pumps), Animal (Cats, Dogs, Equines, Bovines), End User (Hospitals, Clinics) – Global Forecast to 2023″, published by MarketsandMarkets™, the global Veterinary Equipment Market is projected to reach USD 2.40 billion by 2023 from USD 1.63 billion in 2018, at a CAGR of 8.0% during the forecast period of 2018 to 2023. The Veterinary equipment and disposables are used in monitoring, surgeries, and the treatment of diseases in animals. Rising animal health expenditure and growing demand for pet insurance, increasing number of veterinary practitioners in developed regions, and growth in the companion animals market are the primary drivers for the global veterinary equipment market and veterinary disposables market during the forecast period. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=14169630 Growth in the companion animal population; The adoption of companion animals has grown globally due to the positive health benefits associated with them—reduced cardiac arrhythmias, normalization of blood pressure, decreased anxiety, greater psychological stability, and improved wellbeing. According to the APPA National Pet Owners Survey 2017–2018, the canine population in the US increased from 69.9 million in 2012 to 89.7 million in 2016, while the feline population increased from 74.05 million in 2012 to 94.2 million in 2016. According to the European Pet Food Industry Federation (FEDIAF), the canine population in Germany increased from 5.30 million in 2012 to 8.66 million in 2016, whereas the feline population increased from 8.20 million in 2012 to 13.40 million in 2016. Emerging markets such as Brazil, China, India, and Mexico are also witnessing growth in animal ownership. According to the India International Pet Trade Fair (IIPTF), the number of pets increased from 11 million in 2014 to 15 million in 2016. Approximately 600,000 pets are adopted every year in India. Such trends are expected to support the growth of the animal health industry, which, in turn, will drive the growth of dependent industries such as veterinary equipment market and veterinary disposables market. The critical care consumables segment is expected to account for the largest share of the Veterinary Equipment and Disposables Market in 2018. On the basis of type, the critical care consumables segment accounted for the largest share of the global Veterinary Equipment and Disposables Market. The large share of consumables can be attributed to the large number of consumables required and consumed in almost every veterinary care process, as opposed to the one-time cost of capital equipment. The small companion animals will continue to dominate the Veterinary Equipment and Disposables Market during the forecast period. Based on animal, the small companion animals’ segment will dominate the Veterinary Equipment and Disposables Market in 2023. The large share of this segment can be attributed to the high adoption of companion animals and rising expenditure on animal health. The veterinary clinics segment is estimated to hold the largest market share of the Veterinary Equipment and Disposables Market in 2023. Based on end user, veterinary clinics are estimated to hold the largest share of the Veterinary Equipment and Disposables Market in 2023. The large share of this segment can be attributed to the growing number of patient visits along with the increasing number of private clinical practices and increasing practice revenues. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=14169630 North America will dominate the market in 2023. North America is estimated to hold the largest share of the Veterinary Equipment and Disposables Market during the forecast period, followed by Europe and the Asia Pacific. Factors such as the increasing number of companion animals, rising companion animal healthcare expenditure, rise in the number of livestock animals in North America (primarily due to the increasing consumption of meat and dairy products), and growth in the pet insurance market are responsible for the region’s large share in the global Veterinary Equipment and Disposables Market. The prominent players in the Veterinary Equipment and Disposables Market are Mindray Medical International Limited (China), Smiths Group plc (UK), Nonin Medical (US), Digicare Biomedical Technology, Inc. (US), B. Braun Melsungen AG (Germany), Henry Schein (US), Vetland Medical Sales and Services, LLC (US), Hallowell Engineering & Manufacturing Corporation (US), Infiniti Medical, LLC (US), DRE Veterinary (US), and Midmark Corporation (US). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=14169630 |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed