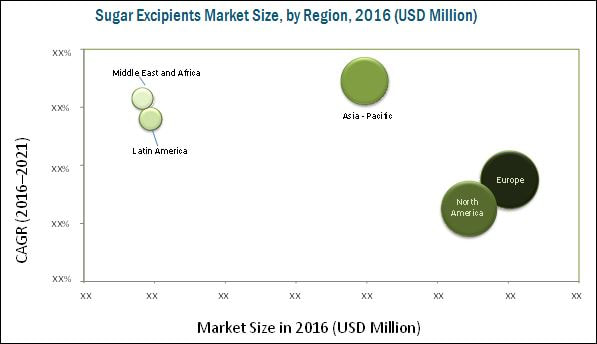

The Increasing use of co-processed excipients to improve the dissolution, bioavailability, and solubility of recently developed active pharmaceutical ingredients (APIs), rapid growth in the generics market due to the patent expiration of many blockbuster drugs, and increasing development of orally disintegrating tablets (ODTs) are expected to propel the growth of this market. However, stringent regulatory requirements leading to shortage of FDA-approved manufacturing sites can hinder their market growth to a certain extent. The report “Sugar-Based Excipients Market by Product (Actual Sugars, Sugar Alcohols, Artificial Sweeteners), Type (Powder/Granule, Crystal, Syrup), Functionality (Filler & Diluent, Tonicity Agents), Formulation (Oral, Topical, Parenteral) – Global Forecast”, the sugar excipients market has witnessed healthy growth during the last decade, and is expected to grow at a CAGR of 4.3%, to reach USD 1,060.6 Million. Request Research SamplePages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=242342136 Sugar-Based Excipients Market Segmentation in Detailed: Based on type, segmented into powders/granules, direct compression sugars, crystals, and syrups. on the basis of functionality, segmented into fillers & diluents, flavoring agents, tonicity agents, and other functionalities. Based on formulation, segmented into oral formulations, parenteral formulations, topical formulations, and other formulations. Based on the type, segmented into powders/granules, direct compression sugars, crystals, and syrups. Similarly, on the basis of functionality, the market is segmented into fillers & diluents, flavoring agents, tonicity agents, and other functionalities The actual sugar accounted for the largest share of the global sugar excipients market. The sugar alcohols segment is expected to witness the highest growth in the next five years primarily due to the rising use of mannitol in a wide range of dosage forms such as oral and topical, and its high adaptability in emerging formulation technologies, such as orally disintegrating tablets. On the basis of type, powders/granules segment accounted for the large share of the global Sugar-Based Excipients Market. The large share of the powders/granules segment is mainly attributed to its wide use in various types of formulations in the pharmaceutical industry. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=242342136 Geographical View in-detailed: Europe is the largest regional segment for the global sugar excipients market. The large share of this regional segment can be attributed to increasing investments in drug development, increasing production of generic drugs, and favorable government initiatives in the region. The market in the Asia-Pacific region is expected to register the highest CAGR owing to the significant growth in the regional healthcare market as well as the pharmaceutical industry, growing scientific base and capability, and favorable government policies, and low-cost manufacturing advantage in this region. Global Key Leaders: Roquette Group (France), DFE Pharma (Germany), BASF SE (Germany), and Ashland Inc. (U.S.), held the major share of the sugar excipients market, and are expected to dominate the market during the forecast period. Other major players in this market are Associated British Foods Plc (U.K.), Cargill, Inc. (U.S.), Colorcon, Inc. (U.S.), FMC Corporation (U.S.), MEGGLE AG (Germany), and The Lubrizol Corporation (U.S.).

0 Comments

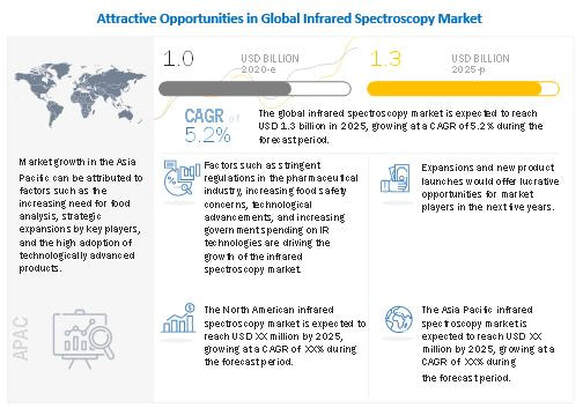

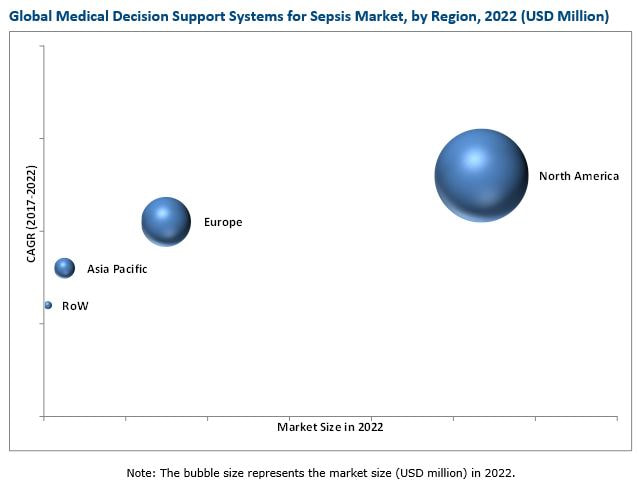

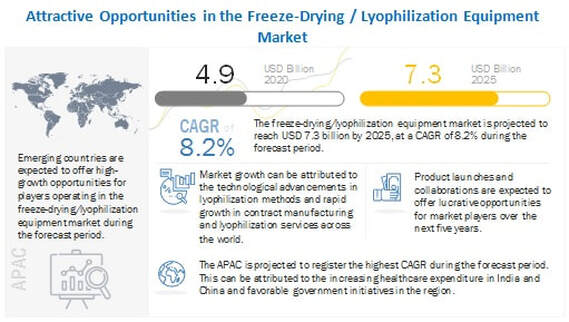

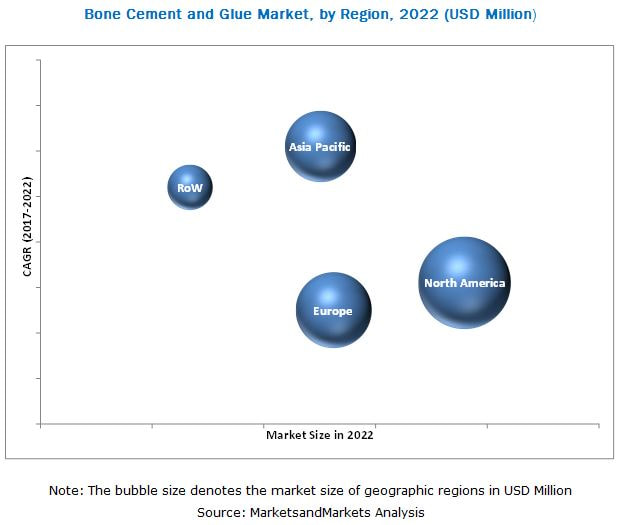

The report “Infrared and Terahertz Spectroscopy Market by Instrument Type (Benchtop Instruments, Microscopy Instruments, Portable Instruments, Hyphenated Instruments), Spectrum, Application – Global Forecast to 2025″, the infrared spectroscopy market is expected to reach USD 1.3 billion by 2025 from USD 1.0 billion in 2020, at a CAGR of 5.2% during the forecast period. The terahertz spectroscopy market is expected to reach USD 45 million by 2025 from USD 30 million in 2020, at a CAGR of 8.3% during the forecast period. Growth Opportunities Growing opportunities in emerging nations; As compared to mature markets such as the US and Europe, emerging markets such as China and India are expected to provide significant growth opportunities for players operating in this market. Huge demand for spectroscopy is generated from China and India due to the Greenfield projects set up in various end-user industries in these countries. The life sciences industry in this region is also quite robust and is expected to contribute significantly to the growth of the infrared spectroscopy market in the coming years. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=248742550 The mid-infrared radiation segment to hold the largest market share in 2020. Based on spectrum, segmented into mid-infrared radiation, near-infrared radiation and far-infrared radiation. In 2020, the mid-infrared radiation segment is expected to command the largest share of the infrared spectroscopy market. The increase in the number of healthcare and pharmaceuticals applications and extensive usage in the food industry are driving the growth of this segment. The semiconductor segment to hold the largest market share in 2020. Based on application, segmented into semiconductor, homeland security, non-destructive testing and research & development. In 2020, the semiconductor segment is expected to command the largest share of the terahertz spectroscopy market. Technologicala dvancements in the growing semiconductor industry is the major factor riving the growth of this segment. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=248742550 Based on region, the Infrared and Terahertz Spectroscopy Market is segmented into North America, Asia-Pacific, Europe and Rest of the world(RoW). Asia Pacific is expected to register the highest CAGR during the forecast period. The major factors driving the growth of the Asia Pacific market include strategic expansions by key players, increasing food safety concerns, and adoption of technologically advanced products. The prominent players in the global infrared spectroscopy market include PerkinElmer (US), Bruker Corporation (US) Shimadzu Corporation (US), Thermo Fisher Scientiific (US), Agilent Technologies (US). And the major players in the terahertz spectroscopy market include TeraView Ltd (UK), Advantest Corporation (Japan), Menlo Systems GmbH (Germany, Toptica Photonix AG (Germany).  The report “Medical Decision Support Systems for Sepsis Market Revolutionary Primer for Clinical Decision Support (Market Dynamics, Case Studies, Regional Analysis (North America, Europe, Asia Pacific, Rest of the World)) – Global Forecast to 2022″, The MDSS for Sepsis Market is expected to reach USD 35.6 Million, at a CAGR of 24.3%. Increasing funding & research grants, growing pressure to curb healthcare spending, and improving patient outcomes are the major factors propelling the growth of the market. In addition, machine learning & artificial intelligence in CDSS is posing as a lucrative opportunity for the market in the coming years. Various players in the market offer sepsis CDS solutions embedded in their EHR while there are others who offer separate surveillance solutions for sepsis. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=227232851 Objectives of the Study: – To define, describe, and forecast the global medical decision support systems for sepsis market on the basis of region – To provide detailed information regarding the major factors influencing the growth of the market (drivers, restraints, opportunities, and challenges) – To analyze micromarkets with respect to individual growth trends, future prospects, and contributions to the overall market – To analyze the opportunities in the market for stakeholders and provide details of the competitive landscape for market leaders – To forecast the size of the market segments with respect to four main regions, namely, North America, Europe, Asia Pacific, and the Rest of the World Geographically, the North American market accounted for the largest share in 2017 and is expected to register the highest CAGR during the forecast period. The large share and high growth can be attributed to factors such as increasing efforts to curb healthcare spending, federal initiatives such as the Hospital Readmissions Reduction Program, and rising investments in HCIT solutions in the country. Major players providing sepsis CDS modules include Cerner, Epic, and MEDITECH. Third-party vendors like VigiLanz, Iatric Systems, and PeraHealth are also based out of the US. The presence of these key players in the country has made the US a center of innovation in the CDSS market. Moreover, growing awareness regarding the use of HCIT solutions for sepsis management, high number of installations of CDS solutions, and various studies have been conducted to check benchmark for the efficacy of different solutions in the US. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=227232851 Global Key Leaders: Wolters Kluwer Health (US), Cerner Corporation (US), Philips Healthcare (Netherlands), Amara Health Analytics (US), McKesson Corporation (US), Ambient Clinical Analytics (US), Iatric Systems Inc. (US), PeraHealth Inc. (US), Health Catalyst Inc. (US), and Allscripts Healthcare Solutions, Inc. (US) are the key players in the global medical decision support systems for sepsis market.  The report “Freeze-Drying Equipment Market by Type (Tray, Shell, Manifold), Scale of operation (Industrial, Lab, Pilot), Application (Food, Pharma & Biotech), Accessories (Loading & Unloading, Monitoring, Vacuum Systems, Drying Chambers) – Global Forecast to 2025″, the global freeze-drying/lyophilization equipment market is projected to reach USD 7.3 billion by 2025 from USD 4.9 billion in 2020, at a CAGR of 8.2% from 2020 to 2025. Opportunities: Loss of patent protection of several biologics; The biologics market is one of the major contributors to the growth of the freeze-drying market in the healthcare industry. Biosimilars are expected to drive the growth of the biotechnology industry in the next decade. This is because several key biologics are expected to lose their patent in the coming years. An increasing number of biosimilars are being developed in the market as a cost-effective alternative for biopharmaceutical medications for chronic disorders. The growing R&D and emergence of biosimilars will drive the market for the lyophilization of biologics and biopharmaceutical products. In recent years, over 30% of US FDA-approved parenterals were lyophilized drugs. Soon, more than half of all injectable drugs will require lyophilization, which will further create the demand for lyophilization solutions in the pharmaceutical industry. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=24018886 The tray-style freeze dryers segment accounted for the largest market share in 2019. Based on type, the lyophilization equipment market is classified into tray-style freeze dryers, manifold freeze dryers, and shell (rotary) freeze dryers. In 2019, the tray-style freeze dryers segment accounted for the largest share of 72.1%. This segment is also estimated to grow at the highest CAGR of 8.2% during the forecast period. Growth in this market is largely driven by factors such as the increasing demand for contract manufacturing and contract lyophilization services in the pharmaceutical industry, the growing commercialization of labile drugs, and the rising demand for freeze-dried food products. Tray-style freeze dryers are also larger than manifold and rotary freeze dryers, enabling them to dry products in bulk. The industrial-scale lyophilization equipment segment accounted for the largest market share in 2019. Based on scale of operation, the freeze-drying market is segmented into industrial-scale lyophilization equipment, pilot-scale lyophilization equipment, and laboratory-scale lyophilization equipment. In 2019, the industrial-scale lyophilization equipment segment accounted for the largest share of 68.2% of the market. The large share of this market segment can be attributed to the high standard of quality provided by industrial-scale lyophilization equipment. Industrial-scale lyophilization equipment can also be customized as per process requirements. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=24018886 Key Market Players; Some of the prominent players in Freeze-Drying Equipment Market are GEA Group (Germany), Azbil Corporation (Japan), Shanghai Tofflon Science Technology Co., Ltd. (China), IMA S.p.A. (Italy), SP Industries, Inc. (US), HOF Enterprise Group (Germany), Labconco Corporation (US), Martin Christ Gefriertrocknungsanlagen GmbH (Germany), Millrock Technology, Inc. (US), and OPTIMA Packaging Group GmbH (Germany). Asia –Pacific was the largest regional market for lyophilization equipment market in 2019 The freeze-drying/lyophilization equipment market is segmented into five major regions, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2019, the Asia Pacific accounted for the largest share of 34.6% of the market and is projected to register the highest CAGR of 10.4% during the forecast period. The large share of the Asia Pacific regional segment can be attributed to the rising number of investments in this region, growth in R&D expenditure, and geographic expansion of lyophilization equipment companies in this region. Moreover, the presence of major players in the lyophilization market in the APAC region and the expansion of the manufacturing units of leading pharma companies in this region is expected to boost the market growth in this region in the forecast period.  The report “Bone Cement and Glue Market by Type (PMMA, Calcium Phosphate, Natural, Synthetic), Application (Arthroplasty (Total Knee, Hip, Shoulder), Kyphoplasty, Vertebroplasty), End User (Hospitals, Clinics, Ambulatory Surgery Centers) – Global Forecast to 2022″, the bone cement market is expected to reach USD 1,322.6 Million, at a CAGR of 5.9% The Factors driving the growth of this market include growing geraitic population, increasing incidence of sports injuries, rising number of road accidents, and increasing developments in the regenerative medicines field. The objectives of this study are as follows:

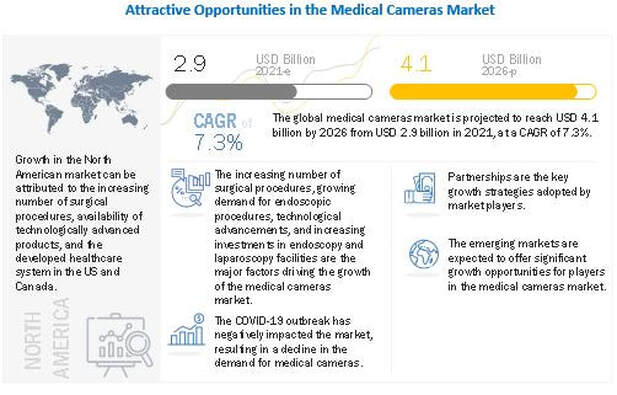

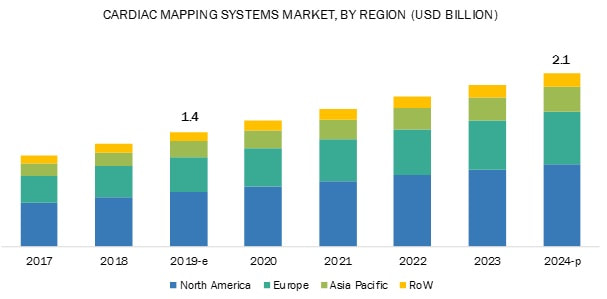

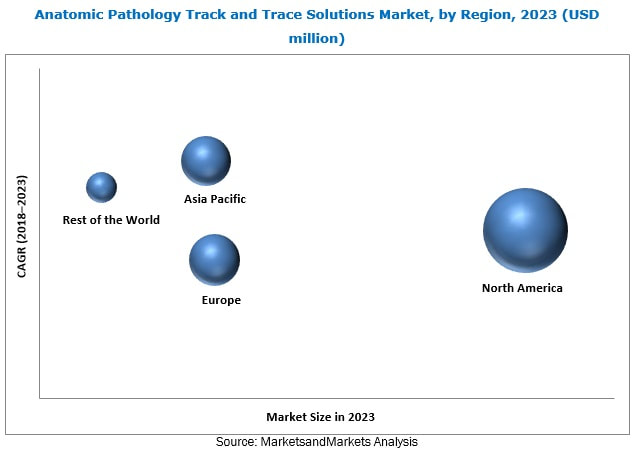

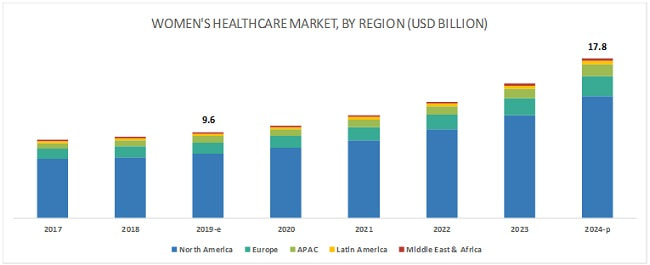

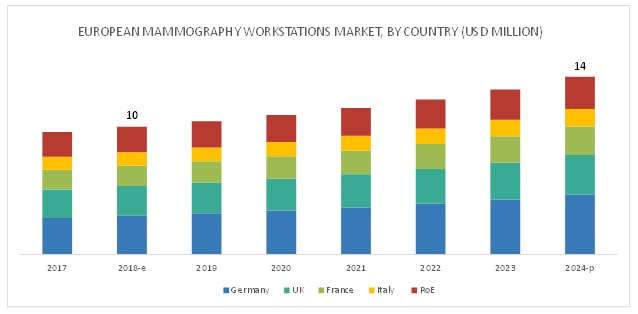

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=131540876 Bone cement is estimated to account for the largest market share On the basis of type, Classified into bone cement and bone glue. The bone cement segment is expected to lead the global bone cement and glue market in 2017. Factors driving the growth of this segment include rising incidence of osteoporosis and increasing number of arthroplasty procedures across the globe. The arthroplasty segment is estimated to dominate the market By application, the market is segmented into arthroplasty, kyphoplasty, vertebroplasty, and other applications. The arthroplasty segment is anticipated to account for the largest share of the global bone cement and glue market in 2017. The large share of this segment can be attributed to the increasing number of knee, hip, and shoulder injuries. The hospital segment is estimated to command the largest share of the market during the forecast period On the basis of end user, Categorized into hospitals, ambulatory surgery centers (ASCs), and clinics/physician offices. The hospitals segment is estimated to account for the largest share of the global bone glue market. The heavy burden of orthopaedic medical conditions (which requires implants for their management) and increasing number of hospitals are the key factors driving the growth of this end-user segment. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=131540876 Geographically; the bone cement market is segmented into North America, Europe, Asia Pacific, and the Rest of the World (RoW). North America is estimated to dominate the market in 2017. This is attributed to factors such as the increasing incidence of sports injuries, growing geriatric population, and improved healthcare infrastructure in the region. Key players in the bone cement and glue market include Stryker (US), Zimmer Biomet (US), DePuy Synthes (US), Smith & Nephew (UK), Arthrex (US), DJO Global (US), Exactech (US), TEKNIMED (France), Heraeus Medical (Germany), CryoLife (US), Cardinal Health (US), and Trimph (Australia).  The study involved four major activities in estimating the current size of the medical cameras market. Exhaustive secondary research was done to collect information on the market and its different subsegments. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation procedures were used to estimate the market size of the segments and subsegments. Expected Revenue Surge: The Medical Cameras Market is projected to reach USD 4.1 billion by 2026 from USD 2.9 billion in 2021, at a CAGR of 7.3% during the forecast period GROWTH OPPORTUNITY – Emerging countries in the Asia Pacific market; The Asia Pacific region presents significant growth opportunities for the medical cameras market. Owing to its massive patient population, the rapid expansion of the healthcare industry, and the shifting focus of manufacturers towards developing countries in this region. China and India, the two most populous countries globally, have a huge patient population mainly due to the rapidly growing senior population and the subsequent increase in the prevalence of ophthalmological & dermatological diseases. Treatment for these diseases demands the use of endoscopes, retinal cameras, and intraoral cameras. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=201071746 Market Segmentation in Detailed: Based on Type; Segmented into surgical microscopy cameras, endoscopy cameras, dermatology cameras, ophthalmology cameras, dental cameras, and other medical cameras. The Endoscopy cameras segment accounted for the largest share of global medical cameras market. This can be attributed to the increasing number of endoscopy procedures across the globe. Based on Sensor; Segmented into CMOS Sensor and CCD Sensor. In 2020, CMOS sensors accounted for the highest growth rate. The major factors driving the growth of this is the observable shift in the preference for CMOS sensors over CCD sensors due to its various advantages over CCD sensors. Based on Resolution, Segmented into standard-definition (SD) cameras and high-definition (HD) cameras. High-definition cameras accounted for the largest share of the global medical cameras market in 2020. The large share of this segment can primarily be attributed to the greater demand for HD cameras among end users due to the significant requirement of high-quality images in medical specialties. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=201071746 Geographically; The medical camera market is divided into five regions, namely, North America, Europe, Asia Pacific, and Rest of the World. North America dominated the global market. The large share of the North American region is mainly attributed to the technological advancements in medical cameras, implementation of favorable government initiatives, and rise in the number of surgical procedures. The major players in the medical camera market are Olympus Corporation (Japan), Richard WOLF GmbH (Germany), TOPCON CORPORATION (Japan), Sony Corporation (Japan), Stryker Corporation (US), Danaher Corporation (US), Canon Inc. (Japan), Carl Zeiss AG (Germany), Smith & Nephew (UK), Carestream Dental LLC (US), and Basler AG (Germany)  The report “Cardiac Mapping Market by Product (Contact Mapping Systems (Electroanatomical Mapping, Basket Catheter Mapping), Non-contact Mapping Systems), Indication (Atrial Fibrillation, Atrial Flutter, AVNRT), Region – Global Forecast to 2024″, the Cardiac Mapping System Market is expected to reach USD 2.1 billion by 2024 from USD 1.4 billion in 2019, at a CAGR of 8.7%. The Growth in the cardiac mapping industry is driven primarily by factors such as new entrants in the market, growing investments, funds, and grants, increasing incidence of target diseases, and growth in the geriatric population. Market Size Estimation; Both top-down and bottom-up approaches were used to estimate and validate the total size of the cardiac mapping market. These methods were also used extensively to determine the extent of various subsegments in the market. The research methodology used to estimate the market size includes the following: – The key players in the industry and markets have been identified through extensive secondary research – The industry’s supply chain and market size, in terms of value, have been determined through primary and secondary research processes – All percentage shares, splits, and breakdowns have been determined using secondary sources and verified through primary sources Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=89853405 Atrial fibrillation is the primary application areas of the global cardiac mapping market The market is segmented into atrial fibrillation, atrial flutter, atrioventricular nodal reentry tachycardia (AVNRT), other arrhythmias. The atrial fibrillation segment estimated to command the largest share of the market in 2019, and this segment is also projected to register the highest CAGR owing to the rise in incidences of AF worldwide and the subsequent increase in the ablation procedures. Geographical View in-detailed: North America held the largest share of the market in 2019 and is projected to continue to do so during the forecast period. Factors such as the increase in approval rate of mapping systems and clinical trials validating cardiac mapping systems in the US, high incidence of CVDs, growing focus of government organizations on providing funding for research, and increasing geriatric population in Canada are driving the North American cardiac mapping market. Key Market Players; The major vendors in the cardiac mapping market include Biosense Webster (US), Abbott (US), and Boston Scientific Corporation (US). These leading players offer a strong suit of products for cardiac mapping and have a broad geographic presence. The other players in this market include Medtronic (Ireland), MicroPort Scientific Corporation (China), EP Solutions SA (Switzerland), Acutus Medical (US), Koninklijke Philips N.V. (Royal Philips) (Netherlands), Lepu Medical (China), BIOTRONIK (Germany), AngioDynamics (US), BioSig Technologies (US), APN Health (US), CoreMap (US), Kardium (Canada), Catheter Precision (US), and Epmap-System (Germany). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=89853405 Biosense Webster (US) held the dominant position in the cardiac mapping market in 2018. The large share of this company can be attributed to its strong suite of cardiac mapping systems, software, and catheters. The company provides products mainly targeted at the diagnosis and treatment of several cardiac arrhythmias, such as atrial fibrillation. Moreover, the firm has a strong geographic presence in all regions of the world. The company focuses on product launches to create a strong foothold in the market. In 2019, Biosense introduced the CARTONET, a cloud-based networking and data analytics software solution. Abbott (US) held the second-largest share of the cardiac mapping market in 2018. The company offers an advanced EnSite Precision cardiac mapping system, along with sensor-enabled catheters compatible with the mapping system. The firm’s Cardiovascular and Neuromodulation Products segment offers rhythm management, electrophysiology, heart failure, vascular, and structural heart devices for the treatment of cardiovascular diseases. The firm focuses on organic & inorganic growth strategies.  The report “Anatomic Pathology Track and Trace Solutions Market by Product (Software, Hardware (Printer & Labeling Systems), Consumables), Technology (Barcode, RFID), Application (Tissue Cassette, Slide Tracking), End User (Hospital Labs) – Global Forecast to 2023″, the Track and Trace Solutions Market Projected to Reach USD 695.7 Million by 2023. The increasing volume of diagnostic tests performed in anatomic pathology laboratories, rising number of legal cases around cancer misdiagnosis, benefits of automated labeling solutions, increasing consolidation among anatomic pathology laboratories, and the growing adoption of automated systems to enhance the efficiency of laboratories are the major factors driving the growth of this market. However, the high cost associated with the implementation of track and trace solutions in anatomic pathology laboratories is expected to restrain the growth of this market during the forecast period. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=124099392 Software segment is expected to account for the largest share of the anatomic pathology track and trace solutions market. On the basis of product, the track and trace solutions market is broadly segmented into software, hardware, and consumables. In 2018, the software segment is expected to account for the largest share of this market. This can majorly be attributed to the growing need to automate the sample labeling process for reducing manual errors, increasing focus on improving the efficiency of anatomic laboratories, growing adoption of cloud-based LIMS, and the increasing workload in anatomic pathology laboratories. Slide tracking segment is expected to register the highest CAGR in the anatomic pathology track and trace solutions market. Based on application, the track and trace solutions market is segmented into slide tracking, tissue cassettes and blocks tracking, and specimen tracking. The slide tracking segment is estimated to register the highest CAGR during the forecast period primarily due to the implementation of tracking systems for reducing specimen identification errors and increasing workflow efficiency in anatomic pathology laboratories. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=124099392 Geographical View in-detailed: North America is expected to account for the largest share of the anatomic pathology track and trace solutions market in 2018, followed by Europe. The increasing volume of diagnostic tests performed in anatomic pathology laboratories, easy accessibility to advanced technologies, growing demand for advanced cancer diagnostic testing and screening, favorable reimbursement scenario for anatomic pathology diagnostic tests, increasing healthcare expenditure, and the strong presence of leading market players in the region are the major factors responsible for the large share of North America in the anatomic pathology market. Global Key Leaders: The key players operating in the global anatomic pathology track and trace solutions market are Thermo Fisher Scientific (US), Leica Biosystems (Germany), General Data Healthcare (US), Ventana Medical Systems (US), Agilent Technologies (US), Sunquest Information Systems (US), Zebra Technologies Corporation (US), Primera Technology (US), Cerebrum Corporation (US), AP Easy Software Solutions (US), and LigoLab (US).  The report “Women’s Health Care Market by Drugs (Prolia, Xgeva, Evista, Mirena, Zometa, Reclast, Nuvaring, Primarin, Actonel), Application (Female Infertility, Postmenopausal Osteoporosis, Endometriosis, Contraception, PCOS, Menopause) – Global forecast to 2024″, is projected to reach USD 17.8 billion by 2024 from USD 9.6 billion in 2019, at a CAGR of 13.2% during the forecast period. The Market growth is largely driven by the growing incidence of chronic health conditions among women, government initiatives to curb population growth, growing demand for contraceptives to prevent unintended pregnancies, and the growing focus on R&D by key players for the development of advanced products. On the other hand, the reluctance to use contraceptives is a major factor limiting the market growth. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=136585329 Prolia is the largest and fastest-growing segment of the market. Based on drug, the women’s healthcare market is segmented into EVISTA, XGEVA, Prolia, Mirena, Zometa, Reclast/Aclasta, Minastrin 24 Fe, NuvaRing, FORTEO, Premarin, ACTONEL, and ORTHO-TRI-CY LO (28). Prolia is the largest and fastest-growing segment of the market. Prolia has shown a considerable year-on-year growth primarily due to increasing unit demand. Prolia has witnessed positive market growth owing to the increasing prevalence of postmenopausal osteoporosis in the US. The postmenopausal osteoporosis segment is expected to grow at the highest CAGR during the forecast period. On the basis of application, the women’s healthcare market is segmented into hormonal infertility, postmenopausal osteoporosis, endometriosis, contraceptives, menopause, PCOS, and other applications. The postmenopausal osteoporosis segment is expected to grow at a higher CAGR during the forecast period. The growing prevalence of postmenopausal osteoporosis and a high risk of osteoporosis fractures are the prime factors that contribute towards the large share of this segment. Furthermore, the focus of pharmaceutical players on providing effective drugs for postmenopausal osteoporosis also supports the growth of this segment. The postmenopausal osteoporosis segment also holds the largest share of the market owing to these factors. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=136585329 North America accounted for the largest share of the women’s health care market in 2019. The global women’s healthcare market is segmented into five major regions, namely, North America, Europe, APAC, Latin America, and the Middle East & Africa. In 2018, North America (US and Canada) was the largest and the fastest-growing regional market for women’s healthcare. The major factors supporting market growth include the growing prevalence of PCOS and postmenopausal osteoporosis, increasing median age of first-time pregnancies, and increased healthcare spending in the US and Canada. Also, the high awareness and understanding regarding contraceptives among American women and the easy access to modern contraception as compared to developing countries propel the market growth in this region. Key players in the women’s healthcare market; The market is fragmented in nature, with a large number of players, including tier 1 and mid-tier companies competing for market shares. The prominent players in the global market include Bayer AG (Germany), Allergan (Dublin), Merck & Co. (US), Pfizer Inc. (US), Amgen (US), Agile Therapeutics Inc. (US), Ferring Pharmaceuticals (US), Mylan N.V. (US), Lupin (India), Blairex Laboratories (US), and Apothecus Pharmaceutical (US). Amgen (US): Amgen (US) is one of the leading providers of the women’s healthcare market. The company’s sales and marketing activities are greatly focused on the US and Europe. The company provides Prolia and Xgeva for the treatment of osteoporosis in postmenopausal women. These drugs have shown a year-on-year double-digit value gain as well as volume growth, and constitute the largest share of the market. Amgen’s EVENITY, meant for the treatment of osteoporosis in postmenopausal women, is also in phase 3 of development. It is being developed in collaboration with UCB (Belgium). The company’s high brand recognition and focus on product innovation have helped it to maintain its foothold in the market.  The report “European Mammography Workstations Market by Modality (Multimodal, Standalone), Application (Diagnosis, Advanced Imaging, Clinical Review), End User (Hospital, Breast Care Centers, Academia), Country (Germany, UK, France, Italy, Spain) – Forecast to 2024″, the mammography workstations market is projected to reach USD 14 million by 2024 from USD 10 million in 2018, at a CAGR of 5.5% during the forecast period. The Factors such as the rising burden of breast cancer, increasing market availability of multimodality diagnostic platforms, and the increasing patient awareness about the clinical benefits associated with the early diagnosis of breast conditions are driving the growth of the market. Recent Developments in Depth:

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=101392240 The multimodality mammography workstations segment accounted for the largest share of the mammography workstations market. On the basis of modality, segmented into mammography (X-ray) workstations and multimodality mammography workstations. In 2018, the multimodality mammography workstations segment accounted for the larger share of the European mammography workstations market. This can be attributed to the increasingly supportive government initiatives/regulations in Europe, increasing awareness about the diagnostic efficacy of contrast-enhanced digital mammography, growing market availability of integrated mammography solutions, techno-commercial advantages associated with multimodality mammography workstations, and the rising prevalence of breast cancer. The breast care centers segment is expected to register the highest growth rate in the mammography workstations market. On the basis of end users, segmented into hospitals, surgical clinics, & diagnostic imaging centers; breast care centers; and researchers & academia. The breast care centers segment is projected to witness the highest growth rate in the European mammography workstations market during the forecast period. This can be attributed to the increased utilization of multimodal diagnostic imaging (such as PET-CT, MRI, ultrasound, and mammography) in advanced breast cancer diagnosis, rising number of breast screening programs across major European countries, increasing number of training & awareness programs to sensitize healthcare professionals about the advantages of multimodality mammography workstations, and the growing number of public-private breast care centers across key European countries. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=101392240 Germany accounted for the largest share of the mammography workstations market in 2018 This report covers the European mammography workstations market across Germany, the UK, France, Italy, Spain, and RoE. Germany accounted for the largest share of this market in 2018. The large share of Germany is primarily attributed to the better reimbursement scenario in the country as compared to other European countries, wider acceptance of multimodality mammography workstations among major end users (such as hospitals, surgical clinics, and breast care centers), and the rising patient demand for improved cancer screening. Key Market Players; General Electric (US), Koninklijke Philips N.V. (Netherlands), Hologic Inc. (US), Siemens (Germany), and FUJIFILM Corporation (Japan) are the major players in the European mammography workstations market. Other prominent players in this market include Carestream Health (US), EIZO Corporation (Japan), Agfa-Gevaert Group (Belgium), Barco (Belgium), Konica Minolta, Inc. (Japan), Benetec Advanced Medical Systems (Belgium), PLANMED OY (Finland), Sectra AB (Sweden), Aycan Medical Systems, LLC. (US), and Esaote SPA (Italy) |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed