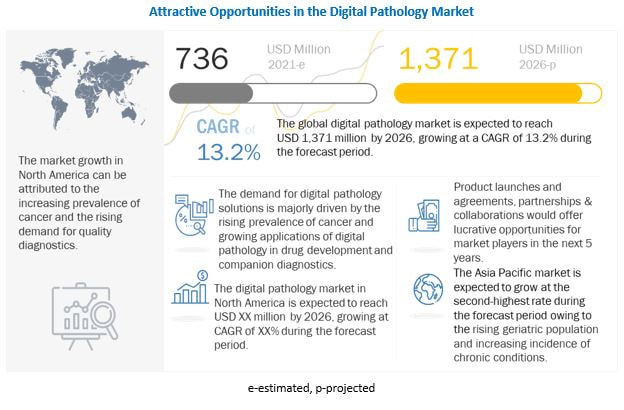

According to the new market research report "Digital Pathology Market by Product( Artificial Intelligence, Scanner, Software, Storage), Type(Human, Veterinary), Application( Teleconsultation, Training, Disease Diagnosis, Drug Discovery), End User( Pharma, Academia, Hospitals ) - Global Forecast to 2026", published by MarketsandMarkets™, the global market is projected to reach USD 1,371 million by 2026 from USD 736 million in 2021, at a CAGR of 13.2% during the forecast period. Browse and in-depth TOC on "Digital Pathology Market" 279 - Tables 43 - Figures 257 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=844 The growth in the Digital Pathology Market is mainly driven by factors such as the increasing adoption of digital pathology to enhance lab efficiency, rising incidence of cancer, and growing applications of digital pathology in drug development and companion diagnostics. On the other hand, the high costs of digital pathology systems are expected to restrain market growth to a certain extent. The scanners segment accounted for the largest share of the Digital Pathology Market in 2020. Based on products, the market has been segmented into scanners, software, and storage systems. The large share of the scanners segment can be attributed to the high price of scanners and the increasing adoption of digital pathology solutions. The human pathology segment accounted for the largest share of the Digital Pathology Market in 2020. Based on type, the global market is segmented into human pathology and veterinary pathology. The human pathology segment accounted for the largest share of the market in 2020. This is due to the increasing number of cancer research activities and growing collaborations among research institutes, universities, and pathology laboratories. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=844 The drug discovery, segment accounted for the largest share of the Digital Pathology Market in 2020. Based on application, the market is segmented into drug discovery, disease diagnosis, and training & education. The drug discovery segment accounted for the largest share of the market in 2020. Growth in R&D expenditure fueled by the need for numerous preclinical and clinical studies performed during the drug discovery and development process is a major factor responsible for market growth. The pharmaceutical & biotechnology companies, segment accounted for the largest share of the Digital Pathology Market in 2020. Based on end users, the global market is segmented into pharmaceutical & biotechnology companies, hospitals & reference laboratories, and academic & research institutes. The pharmaceutical & biotechnology companies segment accounted for the largest share of the Digital Pathology Market in 2020. The large share of this segment can be attributed to the increasing use of digital pathology for drug discovery studies and drug toxicology testing. Biotechnology companies also use digital pathology for biobanking, biopharmaceutical studies, molecular assays, and the development of individualized medicine. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=844 The market in North America is projected to witness the highest growth rate during the forecast period (2021–2026). North America accounted for the largest share of the Digital Pathology Market in 2020. The increasing prevalence of cancer, rising demand for quality diagnostics, the introduction of favorable reimbursement policies, and the implementation of favorable initiatives by the governments in the US and Canada are major factors driving the growth of the market in North America. The major players in the global Digital Pathology Market include Leica Biosystems (US), Koninklijke Philips N.V. (Netherlands), Hamamatsu Photonics (Japan), F. Hoffmann-La Roche Ltd. (Switzerland), 3DHISTECH (Hungary), Apollo Enterprise Imaging (US), XIFIN, Inc. (US), Huron Digital Pathology (Canada), Visiopharm A/S (Denmark), Aiforia Technologies Oy (Finland), Akoya Biosciences (US), Corista (US), Indica Labs (US), Objective Pathology Services (Canada), Sectra AB (Sweden), OptraSCAN (US), Glencoe Software (US), KONFOONG BIOTECH INTERNATIONAL CO., LTD. (China), Inspirata, Inc. (US), PathAI (US), Proscia Inc. (US), Kanteron Systems (Spain), Mikroscan Technologies (US), Motic (US), and Paige (US).

0 Comments

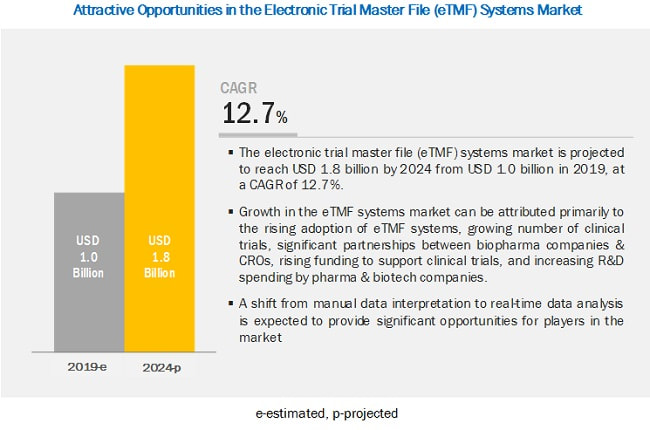

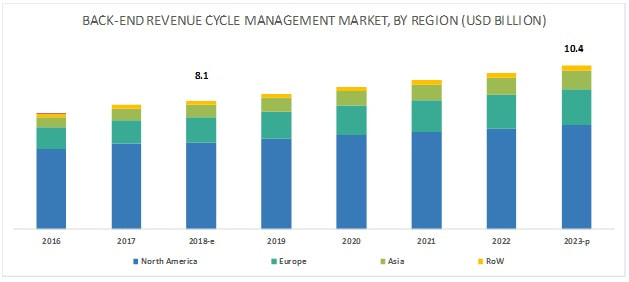

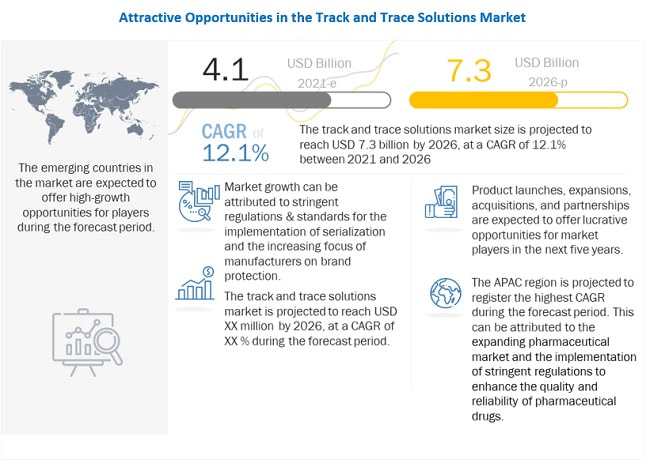

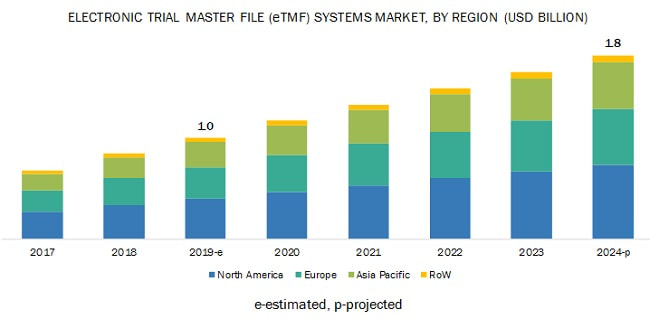

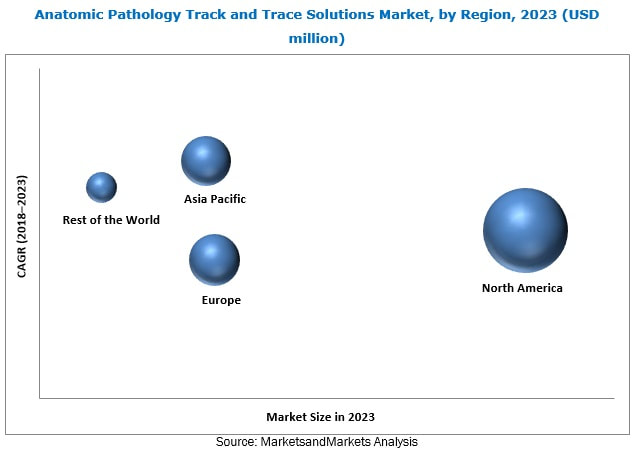

Electronic Trial Master File Systems Market - Emerging Industry Trends and Global Future Forecast3/9/2022  The Research Report on “Electronic Trial Master File Systems Market by Component (Services, Software), End-User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations), Delivery Mode (On-Premise, Cloud-Based), and Region – Global Forecast to 2024″, the eTMF systems market is projected to reach USD 1.8 billion by 2024 from USD 1.0 billion in 2019, at a CAGR of 12.7% The Growth in the Electronic Trial Master File (eTMF) Systems Market can be attributed primarily to the rising adoption of eTMF systems, rising number of clinical trials, partnerships between biopharma companies & CROs, increasing funding to support clinical trials, and the growth in the R&D spending by pharma & biotech companies. Emerging countries are expected to provide significant opportunities for players in the market. However, budget constraints, data privacy issues, and a dearth of skilled professionals will challenge market growth in the coming years Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=94357456 Industry Segmentation In Detailed: The cloud-based eTMF segment accounted for the largest share of the Electronic Trial Master File Systems Market in 2018. Based on delivery mode, the market is segmented into on-premise and cloud-based eTMF. In 2018, the cloud-based eTMF segment accounted for the largest share of the market. The large share of this segment is primarily due to the flexible, scalable, and affordable nature of this delivery mode. The heavy dependence of end-users on service providers will drive the services segment in the eTMF systems market Based on the component, the market is segmented into services and software. The services segment accounted for the largest market share in 2018. The large share of this segment can be attributed to their indispensable nature and repetitive requirement. End-users of eTMF systems rely heavily on service providers for consulting, data storage, implementing services, training, maintenance, and regular upgrades of solutions. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=94357456 Leading Key Players and Analysis: Veeva Systems (US), Oracle Corporation (US), Phlexglobal Limited (UK), TransPerfect Global Inc. (US), Aurea Software (US), LabCorp (US), ePharmaSolutions (US), Wingspan Technology, Inc. (US), MasterControl (US), SureClinical, Inc. (US), Dell EMC (US), Paragon Solutions (US), PharmaVigilant (US), Mayo Clinic (US), Database Integrations, Inc. (US), CareLex (US), Ennov (France), Forte Research (US), Freyr (US), Montrium (US), NCGS Inc. (US), SAFE-BioPharma (US), SterlingBio Inc. (US), BIOVIA Corp. (US), and arivis AG (Germany) are the key players in the eTMF systems market Veeva Systems was the leading player in the electronic trial master file (eTMF) systems market in 2018. The company’s dominant position can be attributed to its solution, Veeva Vault eTMF. The company focuses on various inorganic and organic growth strategies such as solution deployments and expansions to maintain and enhance its market share. In the last three years, Veeva Systems has deployed its solutions at more than ten pharmaceutical companies, CROs, and other sites in the US to expand its user base with the development of innovative solutions. The company also has a strategic focus on expansions in growing emerging markets, such as the Middle East and Asia. Geographical Analysis in Detailed: The eTMF systems market is divided into North America, Europe, Asia Pacific, and the Rest of the World (RoW). The North American market accounted for the largest share of the Electronic Trial Master File Systems Market in 2018, primarily due to the increasing government funding for clinical research and a large number of clinical trials. Several major global players are also based in the US, owing to which the country has become a center of innovation in the electronic trial master file (eTMF) systems market. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=94357456 Back-end Revenue Cycle Management Market - Global Industry Leaders & Growth Strategies Adopted2/2/2022  MarketsandMarkets Research Report’s View on Revenue Impact? The Back-end Revenue Cycle Management Market is projected to reach USD 10.4 billion by 2023 from USD 8.1 billion in 2018, at a CAGR of 5.0%. Factors Responsible for Growth and In-Depth Analysis? The Factors such as the growing importance of denials management, increasing patient volume, process improvements in healthcare organizations, and declining reimbursement rates are driving the growth of the market. However, the high cost of deployment, integration of back-end revenue cycle management solutions, data breaches and loss of confidentiality, and lack of skilled IT professionals in healthcare are expected to limit market growth to a certain extent in the coming years. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=204439794 Leading Key Players and Analysis: Athenahealth (US), Cerner Corporation (US), Allscripts Healthcare Solutions, Inc. (US), eClinicalWorks (US), Optum, Inc. (US), McKesson Corporation (US), Conifer Health Solutions (US), GeBBs Healthcare Solutions (US), The SSI Group (US), GE Healthcare (US), nThrive (US), DST Systems (US), Cognizant Technology Solutions (US), and Quest Diagnostics (US) are the key players in the Back-End RCM Market. Cerner has a strong foothold in the back-end revenue cycle management market. The company caters to the healthcare technology and financial management needs of its global customers. Cerner focuses on research and development activities, deploying products, and acquisitions to enhance its market presence. For instance, in the past three years, the company deployed more than 15 back-end revenue cycle management solutions across various hospitals, care centers, and medical centers. The acquisition of Siemens Health Services in January 2015 further strengthened its back-end revenue cycle management portfolio. Geographical Analysis in Detailed? The back-end revenue cycle management market is divided into North America, Europe, Asia, and the Rest of the World (RoW). North America is expected to account for the largest share in 2018 owing to factors such as growing HCIT investments in the region and the presence of regulatory mandates. North America is followed by Europe and Asia. The market in Asia is relatively nascent; however, it is projected to be the fastest-growing market during the forecast period. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=204439794 Industry Segmentation: The Services segment to dominate the back-end revenue cycle management market. By product & service, segmented into software and services. The services segment is expected to account for the largest share of the Back-End RCM Market in 2018. The large share of this segment can be attributed to the recurring nature of services such as training and development, installation, software upgrades, consulting, and maintenance. However, due to the need for periodic software upgrades, the software segment is expected to witness the highest growth during the forecast period. The cloud-based systems to register the highest CAGR during the forecast period On the basis of delivery mode, segmented into on-premise and cloud-based systems. The cloud-based segment is expected to register the highest CAGR of the back-end revenue cycle management market during the forecast period. Growth in this segment can be attributed to the comparatively lower capital expenses and operational costs incurred in this model, alongside its scalability, flexibility, and affordability. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=204439794  The implementation of track and trace solutions and technologies is an important strategy adopted by many manufacturing companies and regulatory bodies in recent years. The Research Report on “Track and Trace Solutions Market by Product (Plant Manager, Checkweigher, Barcode Scanner, Monitoring), Technology (2D Barcode, RFID), Application (Serialization, Aggregation, Reporting), End User (Pharma, Food, Medical Devices) – Global Forecast to 2026″, is projected to reach USD 7.3 billion by 2026 from USD 4.1 billion in 2021, at a CAGR of 12.1% during the forecast period. Growth Opportunities: Remote authentication of products; Traditional brand protection technologies such as anti-theft and authentication are intended to protect individual items rather than safeguard the entire supply chain. There is a high possibility of fake products being introduced at any stage in the supply chain. To combat counterfeiting and identify massive product items, a solution with automatic and non-line-of-sight capabilities is required. The demand for technologies with modular designs, which fit enterprise needs, has increased in the last few years. For instance, track and trace technologies based on RFID maintain an electronic pedigree that records the transaction information of products within the supply chain. This approach proved to be a standout for protecting the supply chain against infiltration, theft, and fraud and supporting remote authentication in the brand protection supply chain. Technologies that are scalable from a single production line to a multi-facility/multi-line infrastructure while minimizing the initial investment are projected to gain attention in the coming future. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=158898570 Industry Segmentation In Detailed: “The Software segment accounted for the largest market share in 2020.” Based on products, the track and trace solutions market is segmented into software, hardware components, and standalone platforms based on product. The software segment accounted for the largest share—60.1%—of the track and trace solutions market in 2020. Market growth is largely driven by the increasing awareness about secure packaging, the rising number of counterfeit drugs and related products, and growing awareness of brand protection. In addition, regulatory compliance is further supporting the growth of this market. The standalone platforms segment is expected to register the highest CAGR of 15.9% during the forecast period. The growth in this market is mainly attributed to the stringent government regulations for implementing serialization and UDI codes in the pharma and medical device industry, increasing pressure on pharmaceutical companies to adopt serialization, and increasing demand for standalone platforms to reduce the serialization implementation timeframe. “The Serialization solutions segment accounted for the largest market share in 2020.” Based on application, the track and trace solutions market is segmented into serialization solutions; aggregation solutions; and tracking, tracing, and reporting. The serialization solutions segment accounted for the largest share—62.3%—of the applications market. This segment is projected to grow at a CAGR of 12.0% during the forecast period to reach USD 2,560.9 million by 2026. Stringent regulations for the implementation of serialization solutions in packaging and supply chain applications drive this segments growth. The tracking, tracing and reporting segment is expected to register the highest CAGR of 16.1% during the forecast period owing to the increasing number of regulations such as DSCSA, UDI, and Medical Device Reporting (MDR) for medical devices and pharmaceutical products. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=158898570 Leading Key Players and Analysis: Some of the prominent players in the track and trace solutions market are OPTEL GROUP (Canada), Mettler-Toledo International Inc. (US), Systech International Inc. (US), TraceLink Inc. (US), Antares Vision (Italy), SAP (US), Xyntek Inc. (US), SEA Vision Srl (Italy), Syntegon (Germany), Körber Medipak Systems AG (Switzerland), Siemens AG (Germany), Uhlmann Group (Germany), JEKSON VISION (India), Videojet Technologies, Inc. (US), Zebra Technologies Corporation (US), Axway Inc. (US), ACG Worldwide (India), Laetus GmbH (Germany), and WIPOTEC-OCS (Germany). Geographical Analysis in Detailed: The track and trace solutions market studied in this report is divided into five major regions, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2020, North America accounted for the largest share of 42.9% of the global track and trace solutions market, followed by Europe (33.5%). The presence of developed healthcare systems in the US & Canada; the presence of many pharmaceutical & biotechnology companies and medical device manufacturers; stringent regulations regarding serialization; and the growing medical devices market are major factors driving market growth in North America. Asia Pacific (APAC) is the fastest-growing market and is projected to grow at the highest CAGR of 13.8% for track and trace solutions. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=158898570 MarketsandMarkets Research Report’s View on Revenue Impact? The Global Track and Trace Solutions Market is projected to reach USD 7.3 billion by 2026 from USD 4.1 billion in 2021, at a CAGR of 12.1% during the forecast period. Factors Responsible for Growth and In-Depth Analysis? The implementation of track and trace solutions and technologies is an important strategy adopted by many manufacturing companies and regulatory bodies in recent years. Growth is largely driven by stringent regulations & standards for the implementation of serialization, increasing focus of manufacturers on brand protection, growth in the number of packaging-related product recalls, high growth in the generic and OTC markets, and growth in the medical device industry. On the other hand, the high costs and long implementation time frame associated with serialization and aggregation and the huge setup costs are expected to limit market growth to a certain extent. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=158898570 Leading Key Players and Analysis: Some of the prominent players in the track and trace solutions market are OPTEL GROUP (Canada), Mettler-Toledo International Inc. (US), Systech International Inc. (US), TraceLink Inc. (US), Antares Vision (Italy), SAP (US), Xyntek Inc. (US), SEA Vision Srl (Italy), Syntegon (Germany), Körber Medipak Systems AG (Switzerland), Siemens AG (Germany), Uhlmann Group (Germany), JEKSON VISION (India), Videojet Technologies, Inc. (US), Zebra Technologies Corporation (US), Axway Inc. (US), ACG Worldwide (India), Laetus GmbH (Germany), and WIPOTEC-OCS (Germany). TraceLink; It was the leading market player in the track and trace software solutions market in 2020. TraceLink forms the worlds largest track and trace network that provides cloud-based track and trace solutions to pharmaceutical companies, wholesale distributors, contract manufacturers, and packagers. The company’s Life Sciences Cloud is the world’s largest pharmaceutical track and trace network with its serialization application for supply chain efficiency. TraceLink offers suitable solutions for regulatory requirements in countries like the US, China, Brazil, India, and South Korea. Geographical Analysis in Detailed? The track and trace solutions market studied in this report is divided into five major regions, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2020, North America accounted for the largest share of 42.9% of the global track and trace software solutions market, followed by Europe (33.5%). The presence of developed healthcare systems in the US & Canada; the presence of many pharmaceutical & biotechnology companies and medical device manufacturers; stringent regulations regarding serialization; and the growing medical devices market are major factors driving market growth in North America. Asia Pacific (APAC) is the fastest-growing track and trace solutions market and is projected to grow at the highest CAGR of 13.8% for track and trace solutions. Growing regulatory requirements in the healthcare industry to comply with manufacturing and distribution practices, the rising number of pharmaceutical and biotechnology companies, and the significant economic development in emerging Asia Pacific countries such as China and India are the major factors driving the demand for track and trace solutions in the APAC region. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=158898570 Industry Segmentation: “The 2D Barcode segment accounted for the largest market share in 2020.” Based on technology, the track and trace solutions market is segmented into linear barcodes, 2D barcodes, and radiofrequency identification (RFID). The 2D barcodes segment accounted for the largest share of 76.2% of the technology market in 2020. This segment is projected to grow at a CAGR of 12.4% to reach USD 5,641.3 million by 2026. The large share of the 2D barcodes technology segment can be attributed to the increasing use of 2D barcodes in the packaging industry. They have higher data storage capacities than linear barcodes and contain larger amounts of data with fewer variations in image size. The RFID segment is expected to register the highest CAGR of 13.7% during the forecast period due to the growing demand for these systems in automated pharmaceutical distribution and medical devices due to low labor costs and improved visibility & planning. The Pharmaceutical and Biopharmaceutical Company segment accounted for the largest market share in 2020.” Based on technology, the track and trace solutions market is segmented into linear barcodes, 2D barcodes, and radiofrequency identification (RFID). The 2D barcodes segment accounted for the largest share of 76.2% of the technology market in 2020. This segment is projected to grow at a CAGR of 12.4% to reach USD 5,641.3 million by 2026. The large share of the 2D barcodes technology segment can be attributed to the increasing use of 2D barcodes in the packaging industry. They have higher data storage capacities than linear barcodes and contain larger amounts of data with fewer variations in image size. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=158898570 According to the new market research report "Track and Trace Solutions Market by Product (Plant Manager, Checkweigher, Barcode Scanner, Monitoring), Technology (2D Barcode, RFID), Application (Serialization, Aggregation, Reporting), End User (Pharma, Food, Medical Devices) - Global Forecast to 2026", published by MarketsandMarkets™, the global market is projected to reach USD 7.3 billion by 2026 from USD 4.1 billion in 2021, at a CAGR of 12.1% during the forecast period. The implementation of track and trace solutions and technologies is an important strategy adopted by many manufacturing companies and regulatory bodies in recent years. Browse in-depth TOC on "Track and Trace Solutions Market" 298 – Tables 50 – Figures 318 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=158898570 The Growth in track and trace solutions market is largely driven by stringent regulations & standards for the implementation of serialization, increasing focus of manufacturers on brand protection, growth in the number of packaging-related product recalls, high growth in the generic and OTC markets, and growth in the medical device industry. On the other hand, the high costs and long implementation timeframe associated with serialization and aggregation and the huge setup costs are expected to limit market growth to a certain extent. "The Software segment accounted for the largest market share in 2020." Based on products, the market is segmented into software, hardware components, and standalone platforms based on product. The software segment accounted for the largest share—60.1%—of the track and trace solutions market in 2020. Market growth is largely driven by the increasing awareness about secure packaging, the rising number of counterfeit drugs and related products, and growing awareness of brand protection. In addition, regulatory compliance is further supporting the growth of this market. The standalone platforms segment is expected to register the highest CAGR of 15.9% during the forecast period. The growth in this market is mainly attributed to the stringent government regulations for implementing serialization and UDI codes in the pharma and medical device industry, increasing pressure on pharmaceutical companies to adopt serialization, and increasing demand for standalone platforms to reduce the serialization implementation timeframe. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=158898570 "The Serialization solutions segment accounted for the largest market share in 2020." Based on application, the track and trace solutions market is segmented into serialization solutions; aggregation solutions; and tracking, tracing, and reporting. The serialization solutions segment accounted for the largest share—62.3%—of the applications market. This segment is projected to grow at a CAGR of 12.0% during the forecast period to reach USD 2,560.9 million by 2026. Stringent regulations for the implementation of serialization solutions in packaging and supply chain applications drive this segments growth. The tracking, tracing and reporting segment is expected to register the highest CAGR of 16.1% during the forecast period owing to the increasing number of regulations such as DSCSA, UDI, and Medical Device Reporting (MDR) for medical devices and pharmaceutical products. "The 2D Barcode segment accounted for the largest market share in 2020." Based on technology, the track and trace solutions market is segmented into linear barcodes, 2D barcodes, and radiofrequency identification (RFID). The 2D barcodes segment accounted for the largest share of 76.2% of the technology market in 2020. This segment is projected to grow at a CAGR of 12.4% to reach USD 5,641.3 million by 2026. The large share of the 2D barcodes technology segment can be attributed to the increasing use of 2D barcodes in the packaging industry. They have higher data storage capacities than linear barcodes and contain larger amounts of data with fewer variations in image size. The RFID segment is expected to register the highest CAGR of 13.7% during the forecast period due to the growing demand for these systems in automated pharmaceutical distribution and medical devices due to low labor costs and improved visibility & planning. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=158898570 "The Pharmaceutical and Biopharmaceutical Company segment accounted for the largest market share in 2020." Based on technology, the track and trace solutions market is segmented into linear barcodes, 2D barcodes, and radiofrequency identification (RFID). The 2D barcodes segment accounted for the largest share of 76.2% of the technology market in 2020. This segment is projected to grow at a CAGR of 12.4% to reach USD 5,641.3 million by 2026. The large share of the 2D barcodes technology segment can be attributed to the increasing use of 2D barcodes in the packaging industry. They have higher data storage capacities than linear barcodes and contain larger amounts of data with fewer variations in image size. The RFID segment is expected to register the highest CAGR of 13.7% during the forecast period due to the growing demand for these systems in automated pharmaceutical distribution and medical devices due to low labor costs and improved visibility & planning. "North America was the largest regional market for track and trace solutions market in 2020" The market studied in this report is divided into five major regions, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2020, North America accounted for the largest share of 42.9% of the global market, followed by Europe (33.5%). The presence of developed healthcare systems in the US & Canada; the presence of many pharmaceutical & biotechnology companies and medical device manufacturers; stringent regulations regarding serialization; and the growing medical devices market are major factors driving market growth in North America. Asia Pacific (APAC) is the fastest-growing market and is projected to grow at the highest CAGR of 13.8% for track and trace solutions. Growing regulatory requirements in the healthcare industry to comply with manufacturing and distribution practices, the rising number of pharmaceutical and biotechnology companies, and the significant economic development in emerging Asia Pacific countries such as China and India are the major factors driving the demand for track and trace solutions in the APAC region. Some of the prominent players in the track and trace solutions market are OPTEL GROUP (Canada), Mettler-Toledo International Inc. (US), Systech International Inc. (US), TraceLink Inc. (US), Antares Vision (Italy), SAP (US), Xyntek Inc. (US), SEA Vision Srl (Italy), Syntegon (Germany), Körber Medipak Systems AG (Switzerland), Siemens AG (Germany), Uhlmann Group (Germany), JEKSON VISION (India), Videojet Technologies, Inc. (US), Zebra Technologies Corporation (US), Axway Inc. (US), ACG Worldwide (India), Laetus GmbH (Germany), and WIPOTEC-OCS (Germany).  The Growth in the eTMF systems market can be attributed primarily to the rising adoption of eTMF systems, rising number of clinical trials, partnerships between biopharma companies & CROs, increasing funding to support clinical trials, and the growth in the R&D spending by pharma & biotech companies. Emerging countries are expected to provide significant opportunities for players in the Electronic Trial Master File (eTMF) Systems Market. However, budget constraints, data privacy issues, and a dearth of skilled professionals will challenge market growth in the coming years According to the new market research report “Electronic Trial Master File Systems Market by Component (Services, Software), End-User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations), Delivery Mode (On-Premise, Cloud-Based), and Region – Global Forecast to 2024″ published by MarketsandMarkets™, the eTMF systems market is projected to reach USD 1.8 billion by 2024 from USD 1.0 billion in 2019, at a CAGR of 12.7%. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=94357456 Geographically; divided into North America, Europe, Asia Pacific, and the Rest of the World (RoW). The North American market accounted for the largest share of the eTMF systems market in 2018, primarily due to the increasing government funding for clinical research and a large number of clinical trials. Several major global players are also based in the US, owing to which the country has become a center of innovation in the Electronic Trial Master File Systems Market Veeva Systems (US), Oracle Corporation (US), Phlexglobal Limited (UK), TransPerfect Global Inc. (US), Aurea Software (US), LabCorp (US), ePharmaSolutions (US), Wingspan Technology, Inc. (US), MasterControl (US), SureClinical, Inc. (US), Dell EMC (US), Paragon Solutions (US), PharmaVigilant (US), Mayo Clinic (US), Database Integrations, Inc. (US), CareLex (US), Ennov (France), Forte Research (US), Freyr (US), Montrium (US), NCGS Inc. (US), SAFE-BioPharma (US), SterlingBio Inc. (US), BIOVIA Corp. (US), and arivis AG (Germany) are the key players in the eTMF systems market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=94357456 Market Segmentation in Detailed: the cloud-based eTMF segment accounted for the largest share of the eTMF systems market in 2018. Based on delivery mode, the market is segmented into on-premise and cloud-based eTMF. In 2018, the cloud-based eTMF segment accounted for the largest share of the market. The large share of this segment is primarily due to the flexible, scalable, and affordable nature of this delivery mode. The heavy dependence of end-users on service providers will drive the services segment in the eTMF systems market Based on the component, the market is segmented into services and software. The services segment accounted for the largest market share in 2018. The large share of this segment can be attributed to their indispensable nature and repetitive requirement. End-users of eTMF systems rely heavily on service providers for consulting, data storage, implementing services, training, maintenance, and regular upgrades of solutions. The implementation of track and trace solutions and technologies is an important strategy adopted by many manufacturing companies and regulatory bodies in recent years. Growth in Track and Trace Solutions Market is largely driven by stringent regulations & standards for the implementation of serialization, increasing focus of manufacturers on brand protection, growth in the number of packaging-related product recalls, high growth in the generic and OTC markets, and growth in the medical device industry. On the other hand, the high costs and long implementation timeframe associated with serialization and aggregation and the huge setup costs are expected to limit market growth to a certain extent. According to the new market research report “Track and Trace Solutions Market by Product (Plant Manager, Checkweigher, Barcode Scanner, Monitoring), Technology (2D Barcode, RFID), Application (Serialization, Aggregation, Reporting), End User (Pharma, Food, Medical Devices) – Global Forecast to 2026″ published by MarketsandMarkets™, is projected to reach USD 7.3 billion by 2026 from USD 4.1 billion in 2021, at a CAGR of 12.1% during the forecast period. Opportunities: Remote authentication of products; Traditional brand protection technologies such as anti-theft and authentication are intended to protect individual items rather than safeguard the entire supply chain. There is a high possibility of fake products being introduced at any stage in the supply chain. To combat counterfeiting and identify massive product items, a solution with automatic and non-line-of-sight capabilities is required. The demand for technologies with modular designs, which fit enterprise needs, has increased in the last few years. For instance, track and trace technologies based on RFID maintain an electronic pedigree that records the transaction information of products within the supply chain. This approach proved to be a standout for protecting the supply chain against infiltration, theft, and fraud and supporting remote authentication in the brand protection supply chain. Technologies that are scalable from a single production line to a multi-facility/multi-line infrastructure while minimizing the initial investment are projected to gain attention in the coming future. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=158898570 Geographically; The track and trace solutions market studied in this report is divided into five major regions, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2020, North America accounted for the largest share of 42.9% of the global track and trace solutions market, followed by Europe (33.5%). The presence of developed healthcare systems in the US & Canada; the presence of many pharmaceutical & biotechnology companies and medical device manufacturers; stringent regulations regarding serialization; and the growing medical devices market are major factors driving market growth in North America. Asia Pacific (APAC) is the fastest-growing market and is projected to grow at the highest CAGR of 13.8% for track and trace solutions. Some of the prominent players in the track and trace solutions market are OPTEL GROUP (Canada), Mettler-Toledo International Inc. (US), Systech International Inc. (US), TraceLink Inc. (US), Antares Vision (Italy), SAP (US), Xyntek Inc. (US), SEA Vision Srl (Italy), Syntegon (Germany), Körber Medipak Systems AG (Switzerland), Siemens AG (Germany), Uhlmann Group (Germany), JEKSON VISION (India), Videojet Technologies, Inc. (US), Zebra Technologies Corporation (US), Axway Inc. (US), ACG Worldwide (India), Laetus GmbH (Germany), and WIPOTEC-OCS (Germany). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=158898570 Market Segmentation in Detailed: “The Software segment accounted for the largest market share in 2020.” Based on products, the track and trace solutions market is segmented into software, hardware components, and standalone platforms based on product. The software segment accounted for the largest share—60.1%—of the track and trace market in 2020. Market growth is largely driven by the increasing awareness about secure packaging, the rising number of counterfeit drugs and related products, and growing awareness of brand protection. In addition, regulatory compliance is further supporting the growth of this market. The standalone platforms segment is expected to register the highest CAGR of 15.9% during the forecast period.  The report “Anatomic Pathology Track and Trace Solutions Market by Product (Software, Hardware (Printer & Labeling Systems), Consumables), Technology (Barcode, RFID), Application (Tissue Cassette, Slide Tracking), End User (Hospital Labs) – Global Forecast to 2023″, the Track and Trace Solutions Market Projected to Reach USD 695.7 Million by 2023. The increasing volume of diagnostic tests performed in anatomic pathology laboratories, rising number of legal cases around cancer misdiagnosis, benefits of automated labeling solutions, increasing consolidation among anatomic pathology laboratories, and the growing adoption of automated systems to enhance the efficiency of laboratories are the major factors driving the growth of this market. However, the high cost associated with the implementation of track and trace solutions in anatomic pathology laboratories is expected to restrain the growth of this market during the forecast period. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=124099392 Software segment is expected to account for the largest share of the anatomic pathology track and trace solutions market. On the basis of product, the track and trace solutions market is broadly segmented into software, hardware, and consumables. In 2018, the software segment is expected to account for the largest share of this market. This can majorly be attributed to the growing need to automate the sample labeling process for reducing manual errors, increasing focus on improving the efficiency of anatomic laboratories, growing adoption of cloud-based LIMS, and the increasing workload in anatomic pathology laboratories. Slide tracking segment is expected to register the highest CAGR in the anatomic pathology track and trace solutions market. Based on application, the track and trace solutions market is segmented into slide tracking, tissue cassettes and blocks tracking, and specimen tracking. The slide tracking segment is estimated to register the highest CAGR during the forecast period primarily due to the implementation of tracking systems for reducing specimen identification errors and increasing workflow efficiency in anatomic pathology laboratories. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=124099392 Geographical View in-detailed: North America is expected to account for the largest share of the anatomic pathology track and trace solutions market in 2018, followed by Europe. The increasing volume of diagnostic tests performed in anatomic pathology laboratories, easy accessibility to advanced technologies, growing demand for advanced cancer diagnostic testing and screening, favorable reimbursement scenario for anatomic pathology diagnostic tests, increasing healthcare expenditure, and the strong presence of leading market players in the region are the major factors responsible for the large share of North America in the anatomic pathology market. Global Key Leaders: The key players operating in the global anatomic pathology track and trace solutions market are Thermo Fisher Scientific (US), Leica Biosystems (Germany), General Data Healthcare (US), Ventana Medical Systems (US), Agilent Technologies (US), Sunquest Information Systems (US), Zebra Technologies Corporation (US), Primera Technology (US), Cerebrum Corporation (US), AP Easy Software Solutions (US), and LigoLab (US). |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed