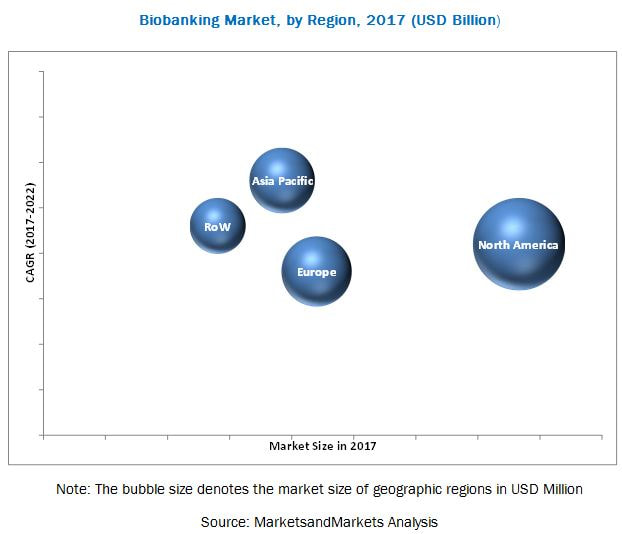

According to the new market research report “Biobanking Market by Product and Service(Equipment, Consumables, Services, Software), Sample Type (Blood Products, Human Tissues, Cell Lines, Nucleic Acids), Application( Regenerative Medicine, Life Science, Clinical Research) – Global Forecast”, published by MarketsandMarkets™, the biobanking devices market is expected to reach USD 2.69 Billion by 2022 from USD 1.85 Billion in 2017, at a CAGR of 7.8%. Regenerative medicine applications for biobanking market will drive the market; The Biobanking Devices Market plays an integral role in advancing biomedical and translational research, through the collection and preservation of biological samples, such as blood, tissues, and nucleic acids, which are then made available for use in research to discover disease-relevant biomarkers; this is further used for diagnosis, prognosis, and predicting drug responses. Growth in the number of research activities in this segment forms a major driver for the market. The availability of government funding for regenerative medicine, stem cell therapeutics, and cell & gene therapy is supporting research activities in this segment. Apart from this, the increasing trend of cord blood banking will also aid growth of this market segment. Future prospects including advancements in orthopedic procedures with the use of stem cells are expected to further support market growth for regenerative medicine. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=594 The Factors driving the growth of this market include the increasing number of genomics research activities for studying diseases; advances in biobanking and the growing trend of conserving cord blood stem cells of newborns; government & private funding to support regenerative medicine research; and the growing need for cost-effective drug discovery and development. The equipment segment is expected to dominate the biobanking devices market. By product and service, the biobanking market is segmented into equipment, consumables, services, and software. The equipment segment is expected to dominate the global market in 2017. Rising number of biobanks and the increasing number of biospecimens are factors increasing the demand for biobanking equipment. Blood products are estimated to command the largest biobanking devices market share. The biobanking market is segmented by sample type into blood products, human tissues, nucleic acids, human waste products, cell lines, and biological fluids. In 2017, the blood products segment is expected to account for the largest share of the market, by sample type. Rising incidence of blood disorders and the increasing demand for various types of blood products across the globe are driving the growth of this segment. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=594 North America is expected to account for the largest share of the biobanking devices market. Based on region, the biobanking market is segmented into North America, Europe, Asia-Pacific, and Rest of the World (RoW). North America is expected to dominate the market in 2017, this is attributed to factors like increasing research activities in regenerative medicine, cell and gene therapy; growing interest in personalized medicine and biomarker discovery; increasing number of biotechnology and pharmaceutical companies; and rising investments in genomics and proteomics research in the region as compared to other regions. Key players in the biobanking market include Thermo Fisher Scientific Inc. (U.S.), Tecan Group Ltd. (Switzerland), Qiagen N.V. (Germany), Hamilton Company (U.S.), Brooks Automation (U.S.), TTP Labtech Ltd (U.K.), VWR Corporation (U.S.), Promega Corporation (U.S.), Worthington Industries [(Taylor Wharton, U.S.)], Chart Industries (U.S.), Becton, Dickinson and Company (U.S.), Merck KGaA (Germany), Micronic (Netherlands), LVL Technologies GmbH & Co. KG (Germany), Panasonic Healthcare Holdings Co. Ltd (Japan), Greiner Bio One [Greiner Holding AG, Austria)], Biokryo GmbH (Germany), Biobank AS (Norway), Biorep Technologies Inc. (U.S.), Cell & Co Bioservices (France), RUCDR infinite biologics (U.S.), Modul-Bio (France), CSols Ltd (U.K.), Ziath (U.K.), and LabVantage Solutions Inc. (U.S.). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=594

0 Comments

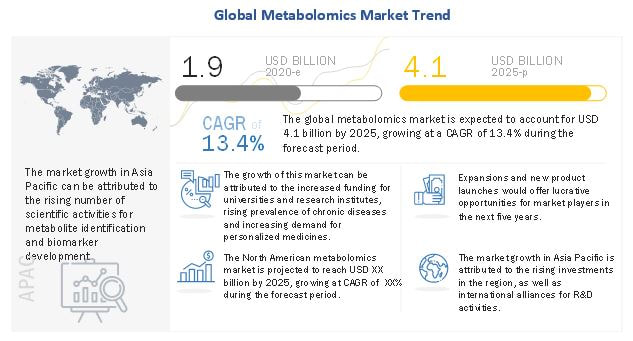

According to the new market research report “Metabolomics Market by Product (GC,UPLC, CE, Surface based Mass Analysis), Application (Biomarker Discovery, Drug Discovery, Functional Genomics), Indication (Cardiology, Oncology, Inborn Errors), End User (Academic Institute, CROs) – Global Forecast to 2025″, published by MarketsandMarkets™, the global Metabolomics Technology Market size is projected to reach USD 4.1 billion by 2025, at a CAGR of 13.4% between 2020 and 2025. Opportunity:Biomarker development; Metabolomics is used to identify new biomarkers through bioinformatics tools, which indicate the changes in the physiological state of a cell or tissue. Biomarkers are important for developing in-vitro diagnostic tools, environmental toxicology screening methods, and drug discovery and development techniques. The omics revolution of the last decade has increased the application of metabolomics in biomedical research. As a result of these technological developments, new biomarkers are being regularly discovered. These biomarkers are required in medical sciences to better define and diagnose diseases, predict adverse drug events, and identify patient groups who would benefit from specific treatments. Moreover, in the near future, identifying biomarkers related to safety, sensitivity, and resistance to commercially available drugs will present significant growth opportunities for the metabolomics market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=900 The major factors driving the growth of this market are the growing R&D expenditure in the pharmaceutical & biopharmaceutical industry, growing demand for personalized medicine and increasing use of metabolomics in toxicology testing are driving the growth of the global metabolomics industry. Separation tools accounted for the largest share in the metabolomics market in 2019. Based on the product & service, the market is categorized into metabolomics instruments and bioinformatics tools and services. The metabolomics instruments segment is further categorized into separation tools and detection tools. Separation tools is sub segmented into gas chromatography, high-performance liquid chromatography, ultra-performance liquid chromatography, and capillary electrophoresis. Similarly, detection tools are categorized into nuclear magnetic resonance (NMR) spectroscopy, mass spectrometry (MS), and surface-based mass analysis. The separation tools segment accounted for the largest share of the market in 2019. The widespread use of separation tools in research activities, increase in funds for research projects, development of innovative technologies in these tools, and their extensive application in the drug discovery process are fueling the growth of this segment. Cancer accounted for the largest share in the market in 2019 Based on indication, the metabolomics market has been segmented into into cancer, cardiovascular disorders, neurological disorders, metabolic disorders, inborn errors of metabolism, and other indications. The cancer segment is expected to account for the largest market share in 2020, with the highest growth rate as well. This can primarily be attributed to the growing use of metabolomics in cancer research and increasing number of cancer patients. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=900 Academic and research institutes accounted for the largest share the metabolomics market in 2019 Based on end user, the market has been segmented into academic and research institutes, pharmaceutical & biotechnology companies, contract research organizations, and other end users. The academic and research institutes segment accounted for the largest share of the market in 2019. The increasing number of research activities in the field of metabolomics and funding to the academic and research institutes to conduct metabolomics research are the factors responsible for the largest share of the segment. Biomarker Discovery accounted for the largest share of the metabolomics market Based on application, the Metabolomics Technology Market has been segmented into biomarker discovery, drug discovery, toxicology testing, nutrigenomics, functional genomics, personalized medicine, and other applications. Biomarker discovery accounted for the largest share of the market in 2019. The growing implications of metabolic biomarkers to access the pathophysiological health status of patients are expected to drive market growth. North America accounted for the largest share of the metabolomics market in 2019. Based on the region, the global Metabolomics Technology Market is segmented into North America, Europe, the Asia Pacific, Latin Ametica and Middle East & Africa. In 2019, North America accounted for the largest share of the metabolomics technologies market. The large share of the North America region can be attributed to the presence of major players operating in the market in the US, growing biomedical research in the US, and rising preclinical activities by CROs and pharmaceutical companies in the region. The metabolomics market is dominated by a few globally established players such as Waters Corporation (US), Agilent Technologies (US), Shimadzu Corporation (Japan), Thermo Fisher Scientific (US), Danaher Corporation (US), Bruker Corporation (US), PerkinElmer (US), Merck KGaA (Germany), GE Healthcare (US), Hitachi High-Technologies Corporation (Japan), Human Metabolome Technologies, Inc. (Japan), LECO Corporation (US), Metabolon, Inc. (US), Bio-Rad Laboratories (US), Scion Instruments (US), DANI Instruments S.p.A. (Italy), GL Sciences (Japan), SRI Instruments (US), Kore Technology Ltd. (UK), and JASCO, Inc. (US) among others. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=900  According to the new market research report "Cell Culture Market by Product (Consumables (Media, Serum, Reagent, Vessels), Equipment (Bioreactor, Centrifuge, Incubator)), Application (Vaccines, mAbs, Diagnostics, Tissue Engineering), End User (Pharma, Biotech, Hospital) - Global Forecast to 2026", published by MarketsandMarkets™, the global market is projected to reach USD 41.3 billion by 2026 from USD 22.8 billion in 2021, at a CAGR of 12.6 % between 2021 and 2026. Browse in-depth TOC on "Cell Culture Market" 690 – Tables 43 – Figures 490 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=559 The growth of this market is majorly driven by the growing awareness about the benefits of cell-based vaccines, increasing demand for monoclonal antibodies (mAbs), funding for cell-based research, growing preference for single-use technologies, the launch of advanced cell culture products, and the growing focus on personalized medicine. On the other hand, the high cost of cell biology research is restraining the growth of this market. The consumables segment accounted for the largest share of the product segment in the cell culture market in 2020. Based on product, the market is segmented into equipment and consumables. The cell culture equipment market is further segmented into supporting equipment, bioreactors, and storage equipment. The cell culture consumables market is segmented into sera, media & reagents, vessels, and bioreactor accessories. In 2020, the consumables segment accounted for the largest share of the market. The large share and high growth of the consumables segment can be attributed to the repeated purchase of consumables and an increase in funding for cell-based research. The biopharmaceutical production segment accounted for the largest share of the application segment in the cell culture market in 2020. Based on application, the market is categorized into biopharmaceutical production, diagnostics, drug discovery & development, tissue engineering & regenerative medicine, and other applications. The biopharmaceutical production segment is further divided into monoclonal antibody production, vaccine production, and other therapeutic protein production. The tissue engineering & regenerative medicine segment is further divided into cell & gene therapy and other tissue engineering & regenerative medicine applications. The biopharmaceutical production segment is estimated to grow at the highest CAGR of 14.1% during the forecast period. The high growth of this segment is attributed to the commercial expansion of major pharmaceutical and biotechnology companies, the increasing demand for mAbs, and the growing regulatory approvals for the production of cell culture-based vaccines. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=559 The Asia Pacific region is the fastest-growing region of the cell culture market in 2020. Based on the region, the global market has been segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa. The Asia Pacific market is estimated to register the highest CAGR during the forecast period. Government initiatives for research on stem cell therapy, growing geriatric population, the rising prominence of regenerative medicine research, increasing number of researchers in Japan, growth of preclinical/clinical research in China, favorable changes in foreign direct investment (FDI) regulations in the pharmaceutical industry in India, and growth of the pharmaceutical & biopharmaceutical sectors in South Korea are the major factors contributing to the growth of the market in the Asia Pacific. Key players in the cell culture market include Thermo Fisher Scientific, Inc. (US), Merck KGaA (Germany), Danaher Corporation (US), and Sartorius AG (Germany). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=559  According to the new market research report “In Vivo Toxicology Market by Product (Animal Models, Reagents & Kits), Test Type (Chronic, Sub-acute), Toxicity Endpoints (Systemic, Immunotoxicity), Testing Facility (Outsourced, In-house), End User (Academic & Research Institute, CROs) – Forecast to 2025″, published by MarketsandMarkets™, the global Toxicity Testing Market size is projected to reach USD 6.6 billion by 2025, at a CAGR of 5.5% between 2020 and 2025. Growth Opportunity: Rising demand for humanized animal models; Humanized animal models are important tools for conducting preclinical research to gain insights into human biology. These models are developed through the engraftment of human cells or tissues, leading to the expression of human proteins in animals. Humanized mice are increasingly being used as models for biomedical research applications, such as cancer, infectious diseases, HIV/AIDS, regenerative medicine, and hepatitis. In March 2019, the National Institute of Allergy and Infectious Diseases (NIAID), an agency of the US Department of Health and Human Services, announced funding for projects to conduct detailed characterization, direct comparisons, and further development of humanized immune system (HIS) mouse models. The need to identify the actual effects of drugs on humans, as well as the growing focus on studying human-specific infections, therapies, and immune responses, is promoting the development and use of humanized animal models Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=105308811 The Market growth is driven largely by the increasing pharmaceutical R&D activities, innovations in animal models, the development of exclusive in vivo toxicology tests, and the increasing demand for personalized medicine. Consumables accounted for the largest share in the in vivo toxicology market in 2019. Based on the product, the market is categorized into instruments and consumables. The consumables segment is further categorized into animal models and reagents & kits. Animal models is sub segmented into mice, rat and other animals. The consumables segment accounted for the largest share of the market in 2019. The widespread use of reagents & kits in research activities, increase in funds for research projects, and their extensive application in the in vivo toxicology studies are fueling the growth of this segment. Chronic test type accounted for the largest share in the toxicity testing market in 2019 Based on test type, segmented into acute, sub-acute, sub-chronic, and chronic test type. The chronic test type segment is expected to dominate the market during the forecast period. In 2019, the chronic test type segment held the largest share of the market, followed by sub-chronic test type. Increasing research on drugs used for longer-duration therapy such as anti-cancer, anti-convulsive, anti-arthritis, and anti-hypertensives drives the growth of the chronic test type market. Outsourced testing facilities accounted for the largest share in the in vivo toxicology market in 2019 Based on the testing facility, the global toxicity testing market is segmented into outsourced testing facilities and in-house testing facilities. The outsourced testing facilities segment is expected to dominate the market, by testing facility, over the forecast period. In 2019, the outsourced testing facilities segment held the largest share of the global market. The large share of this segment is attributed to the increasing R&D investments and cost-saving strategies of pharmaceutical, biopharmaceutical, and medical devices companies, resulting in increased outsourcing of services to CROs. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=105308811 Academic and research institutes accounted for the largest share the market in 2019 Based on the end user, the global market has been broadly segmented into academic & research institutes, pharmaceutical & biotechnology companies, contract research organizations, and other end users (cosmetic companies and food laboratories). The academic and research institutes segment accounted for the largest share of the in vivo toxicology market in 2019. The increasing number of research activities in the field of in vivo toxicology and funding to the academic and research institutes to conduct in vivo toxicology research are the factors responsible for the largest share of the segment. North America accounted for the largest share of the toxicity testing market in 2019. Based on the region, the global in vivo toxicology market is segmented into North America, Europe, the Asia Pacific, Latin America and Middle East & Africa. In 2019, North America accounted for the largest share of the market. The large share of the North America region can be attributed to the presence of major players operating in the market in the US, growing biomedical research in the US, and rising preclinical activities by CROs and pharmaceutical companies in the region. The major players operating in Toxicity Testing Market are by Charles River Laboratories (US), The Jackson Laboratory (US), Envigo (US), Taconic Biosciences, Inc. (US), and JANVIER LABS (France), Thermo Fisher Scientific (US), Danaher Corporation (US), Waters Corporation (US), Agilent Technologies (US), Shimadzu Corporation (Japan), Bruker Corporation (US), PerkinElmer (US). Other prominent players include Merck KGaA (Germany), GE Healthcare (US), and Bio-Rad Laboratories (US), genOway (France), Cyagen Biosciences (US), GVK BIO (India), PolyGene (Switzerland), Crown Biosciences (US), TransCure bioServices (France), Ozgene Pty Ltd. (Australia), Harbour BioMed (US) among others. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=105308811

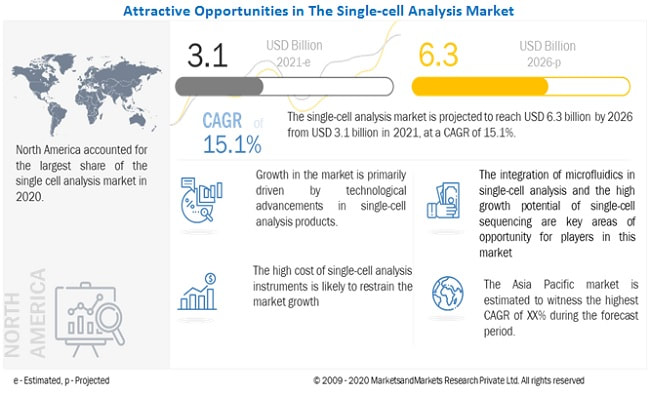

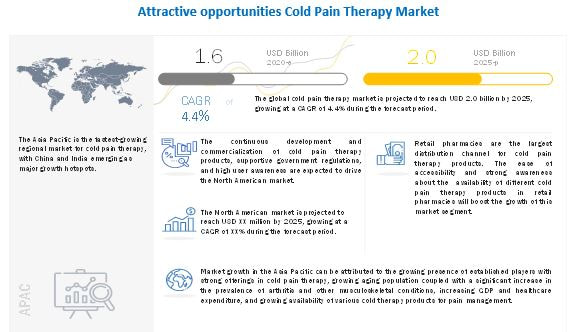

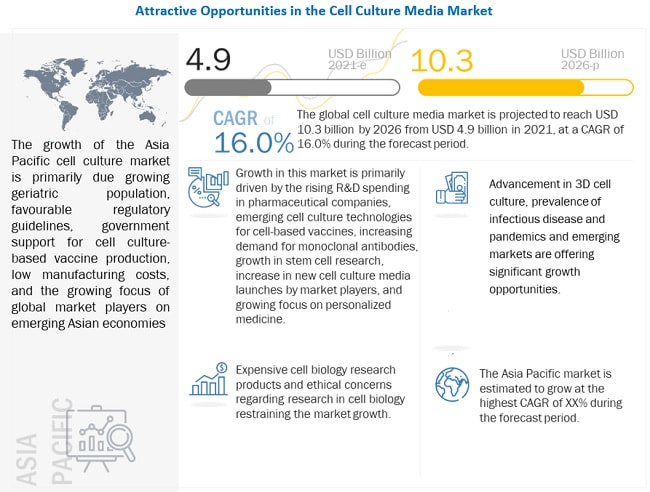

According to the new market research report “Single-cell Analysis Market by Cell Type (Human, Animal, Microbial), Product (Consumables, Instrument), Technique (Flow Cytometry, NGS, PCR, Microscopy, MS), Application (Research, Medical), End User (Pharma, Biotech, Hospitals) – Global Forecast to 2026″, published by MarketsandMarkets™, is projected to reach USD 6.3 billion by 2026 from USD 3.1 billion in 2021, at a CAGR of 15.1% during the forecast period. Growth Driver: Growing prevalence of cancer; One of the most important application areas of single-cell analysis is cancer genomics. According to GLOBOCAN, the number of cancer cases will rise to approximately 30 million by 2040 from 19.3 million cases and 10 million cancer deaths in 2020. The growth in the prevalence of this disease has resulted in a need to conduct extensive research for diagnosis and treatment; single-cell analysis forms an important part of this research. The analysis of individual cells enables the correct diagnosis of diseases and monitoring of treatment efficacy. Single-cell analysis aids in the enumeration of helper T-cells, determination of DNA content, and monitoring the proliferation of tumor cells in breast cancer and other malignancies. Recent Developments: - In March 2021, Beckman Coulter (a subsidiary of Danaher Corporation) launched the CytoFLEX SRT Benchtop Sorter that features expanded laser and color options for use in labs of all sizes. - In March 2020, Fluidigm Corporation (US) opened a new Center of Excellence (CoE) for Imaging Mass Cytometry (IMC) in Singapore, together with the Singapore Immunology Network (SIgN), part of the Agency for Science, Technology and Research.. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=171955254 The Growth in the single-cell analysis market is driven by factors such as technological advancements in single-cell analysis products coupled with increasing R&D in the pharmaceutical and biotechnology industries, growing focus on personalized medicine, growth in stem cell research, and the rising prevalence of cancer. The consumables segment accounted for the largest share of the product segment in the single-cell analysis market in 2020. Consumables accounted for the largest share of the market in 2020. The large share of this segment can primarily be attributed to the frequent purchase of these products compared to instruments, which are considered a one-time investment. The wide applications of consumables in research and genetic exploration, exosome analysis, and isolation of RNA and DNA are also expected to drive market growth. The research applications segment accounted for the largest share of the application segment in the market in 2020 Based on applications, the single-cell analysis market is segmented into research and medical applications. The research applications segment accounted for the largest share of the market in 2020. Increasing government initiatives in stem cell research and the wide usage of single-cell analysis in cancer research are the major factors driving the growth of the research applications segment. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=171955254 The Asia Pacific region is the fastest-growing region of the market in 2020. The market in the Asia Pacific is expected to grow at the highest CAGR of 17.4% during the forecast period. This can be attributed to the fast-growing pharmaceutical industry in this region, rising geriatric population, rising prevalence of cancer, and increasing government initiatives. The prominent players in the single-cell analysis market are Becton, Dickinson and Company (US), Danaher Corporation (US), Merck KGAA (Germany), QIAGEN N.V. (Netherlands), Thermo Fisher Scientific, Inc. (US), Promega Corporation (US), Illumina, Inc. (US), Fluidigm Corporation (US), 10X Genomics (US), and Corning Incorporated (US). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=171955254  According to the new market research report “Cold Pain Therapy Market by Product (OTC (Gels, Creams, Patches, Wraps, Pads), Prescription Devices (Motorized, Non-Motorized), Applications (Musculoskeletal, Post Op, Sports Medicine), Distribution Channel(Hospital, Retail) – Global Forecasts to 2025″, published by MarketsandMarkets™, is projected to reach USD 2.0 billion by 2025 from USD 1.6 billion in 2020, at a CAGR of 4.4% during the forecast period. Driver: Increase in the prevalence of incidence of sports injuries; Musculoskeletal injuries are the most common forms of sports-related injuries. Some of the common injuries include ankle sprains, knee injuries, fractures, joint injuries, tennis elbow (epicondylitis), and dislocations. Cold pain therapy products, such as ice packs and sprays, are the most commonly used products for the management of pain associated with sports-related injuries as they provide instant pain relief. Furthermore, with rising disposable income levels, growing health awareness, growing obesity rate, and growing stress levels, the emphasis on gym activities and workouts among adults across the globe has increased augumenting the market growth. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=55543905 The Increasing prevalence of prevalence of arthritis & other musculoskletal disorders and growing awareness about the availability of cold therapy products are the key factors driving the growth of the market. The cold pain therapy market includes major Tier I and II suppliers of cold therapy products are Sanofi (France), Pfizer (US), Hisamitsu Pharmaceutical (Japan), ROHTO Pharmaceutical (Japan), Beiersdorf (Germany), Johnson & Johnson (US), Medline Industries (US), Össur (Iceland), Performance Health (US), Breg (US).These suppliers have their manufacturing facilities spread across regions such as North America and Europe. COVID-19 has impacted their businesses as well. Due to the pandemic, the market experienced short-term negative growth, which can be attributed to a sharp reduction in access to hospital and retail pharmacies and the temporarily shutdown of orthopedic clinics and rehabilitation centers. However, post lockdown the improved access to cold therapy devices through online platforms and the growing number of patients opting for self-medication with over-the-counter cold therapy products including cold gel packs, ointments, and cold sprays, for pain management are some of the key factors likely to drive the long-term growth of the cold pain therapy market. Additionally, many players have been strongly focusing on implementing brand promotional activities to combat the decline in the sales of cold therapy products in the initial stages of the pandemic. Demand for cold packs for musculoskeletal disorder pain management result in the segment occupying the high share of the cold pain therapy market Cold pack owes a good market share in OTC pain therapy market. The large share of this segment is attributed to factors such as the growing commercial availability of cold packs, increase awareness about the benefits of cold packs providing instant relief from pain associated with arthritis and other musculoakletal disorders, and rise in number of cold packs manufacturers are anticipoated to boost the growth of the segment. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=55543905 Asia Pacific likely to emerge as the fastest growing cold pain therapy market. Geographically, the emerging Asian countries, such as China, India, South Korea, Japan and Singapore, are offering high-growth opportunities for market players. The Asia Pacific market is projected to grow at the highest CAGR of 5.6% from 2020 to 2025. Growing preference for topical products, especially cold patches, expansion of healthcare infrastructure, growing awareness of cold therapy products the region. Moreover, emergence of key players with established product portfolio are driving the growth of the APAC market. Prominent players in cold pain therapy market Sanofi (France), Pfizer (US), Hisamitsu Pharmaceutical (Japan), ROHTO Pharmaceutical (Japan), Beiersdorf (Germany), Johnson & Johnson (US), Medline Industries (US), Össur (Iceland), Performance Health (US), Breg (US), Romsons Group of Industries (India), Unexo Life Sciences (India), and Bird & Cronin (US) Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=55543905  According to the new market research report "Cell Culture Media Market by Type(Serum-free (CHO, BHK, Vero Cell), Stem Cell, Chemically Defined, Classical, Specialty), Application(Biopharmaceutical (mAbs, Vaccine), Diagnostics, Tissue Engineering), End User(Pharma, Biotech) - Global Forecast to 2026", published by MarketsandMarkets™, the market is projected to reach USD 10.3 billion by 2026 from USD 4.9 billion in 2021, at a CAGR of 16.0% between 2021 and 2026. Browse in-depth TOC on "Cell Culture Media Market" 314 – Tables 41 – Figures 303 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=97468536 The global cell culture media market is expected to grow at a CAGR of 16.0% during the forecast period. The growth of this market is majorly driven by the rising R&D spending in pharmaceutical companies, emerging cell culture technologies for cell-based vaccines, increasing demand for monoclonal antibodies, growth in stem cell research, the launch of new cell culture media by market players, and the growing focus on personalized medicine. On the other hand, expensive cell biology research products and ethical concerns regarding cell biology research are expected to hinder the growth of this market. The serum-free media segment accounted for the largest share of the type segment in the cell culture media market in 2020. Based on type, the market is segmented into serum-free media, classical media & salts, stem cell culture media, specialty media, chemically defined media, and other cell culture media. In 2020, the serum-free media segment accounted for the largest share of the market. This can be attributed to the advantages of serum-free media over other types of media, including consistent performance, increased growth & productivity, better control over physiological responsiveness, and reduced risk of contamination by serum-borne adventitious agents in cell culture. The biopharmaceutical production segment accounted for the largest share of the application segment in the cell culture media market in 2020. Based on application, the market is categorized into biopharmaceutical production, diagnostics, drug discovery & development, tissue engineering & regenerative medicine, and other applications. The biopharmaceutical production segment is further divided into monoclonal antibody production, vaccine production, and other therapeutic protein production. The tissue engineering & regenerative medicine segment is further divided into cell & gene therapy and other tissue engineering & regenerative medicine applications. The biopharmaceutical production segment is estimated to grow at the highest CAGR of 17.5% during the forecast period. The high growth of this segment is attributed to the commercial expansion of major pharmaceutical and biotechnology companies, the increasing demand for mAbs, and the growing regulatory approvals for the production of cell culture-based vaccines. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=97468536 The Asia Pacific region is the fastest-growing region of the cell culture media market in 2020. Based on the region, the global market has been segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa. The Asia Pacific market is estimated to register the highest CAGR during the forecast period. The growing geriatric population, favorable regulatory guidelines, government support for cell culture-based vaccine production, low manufacturing costs, and the growing focus of global market players on emerging Asian economies are the major factors contributing to the growth of the cell culture media market in the Asia Pacific. Key players in the cell culture media market include Thermo Fisher Scientific, Inc. (US), Merck KGaA (Germany), Danaher Corporation (US), and Sartorius AG (Germany), Corning Incorporated (US). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=97468536

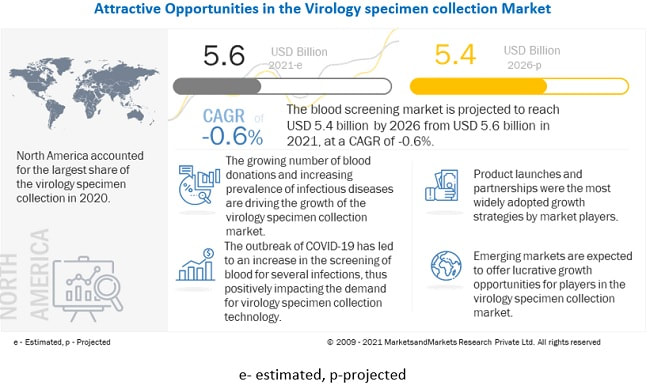

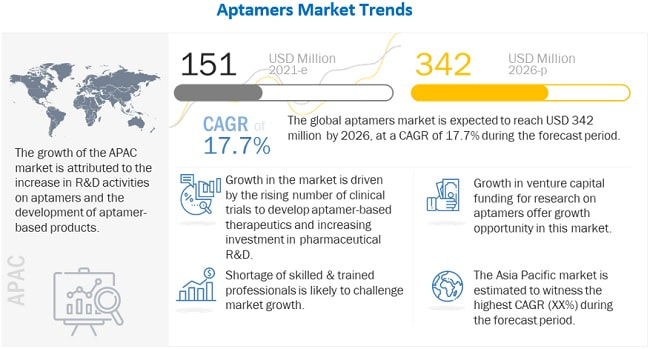

According to the new market research report “Virology Specimen Collection Market by Product (Viral Transport Media, Swabs, Blood Collection Kits, Specimen Collection Tubes), Sample Type (Blood, Cervical, Nasal, Nasopharyngeal, Throat, Oral), Region-Global Forecast to 2026″, published by MarketsandMarkets™, the global market is projected to reach USD 5.4 billion by 2026 from USD 5.6 billion in 2021, at a CAGR of -0.6%. Browse in-depth TOC on “Virology Specimen Collection Market” 26 – Tables 16 – Figures 79 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=150226807 The Rising number of blood donations are among the factors. Emerging economies such as India and Japan are providing lucrative opportunities for the players operating in the market. The viral transport media segment accounted for the largest share of the specimen collection market, by product segment, in 2020 Based on product, the virology specimen collection market is segmented into blood collection kits, specimen collection tubes, viral transport media and swabs. The viral transport media segment accounted for the largest share of the market in 2020. Factors such as rising prevalence of viral diseases and emergence of newer pathogens are contributing for the growth of this market. Blood segment to register the highest growth rate during the forecast period The virology specimen collection market is segmented into blood, nasopharyngeal, nasal, throat, cervical, oral and other samples. In 2020, the blood segment accounted for the highest growth rate. Factors such as the rising number of blood donations and rising prevalence of viral diseases and emergence of newer pathogens. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=150226807 The global Virology Specimen Collection Market is segmented into four major regions, namely, North America, Europe, the Asia Pacific and Rest of the World. In 2020, North America accounted for the largest share of the market. The large share of this region can be attributed to increasing number of blood donations in the region. The major players operating in virology specimen collection market are Becton, Dickinson and Company (US), Quidel Corporation (US), Thermo Fisher Scientific, Inc. (US), Trinity Biotech (Ireland), Titan Biotech, Ltd. (India), Diasorin SA (Italy), Vircell S.L. (Spain), Copan Italia S.p.A. (Italy), Puritan Medical Products, Co. (Guilford, ME) and Hardy Diagnostics (US). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=150226807  According to the new market research report “Aptamers Market by Product Type (DNA, RNA, XNA), Technology (SELEX), Application (Therapeutics, Diagnostics, R&D), End Users (Pharmaceutical & Biotechnology Companies, Academic & Government Research Institutes, CROs) – Global Forecast to 2026″, published by MarketsandMarkets™, is valued at an estimated USD 151 million in 2021 and is projected to reach USD 342 million by 2026, at a CAGR of 17.7% during the forecast period. Browse in-depth TOC on “Aptamers Market” 196 – Tables 38 – Figures 183 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=1167 The Growth of aptamers market is attributed to factors such as increase in number of clinical trials for development of aptamer-based therapeutics, increase in awareness about advantages of aptamers as compared to antibodies, rising investment in pharmaceutical R&D, and rising prevalence of chronic and rare diseases to increase the demand for aptamer-based therapeutics and diagnostics. Growth in the venture capital funding for research on aptamers and growing collaborations with research institutes and pharmaceutical companies are also expected to offer a wide range of growth opportunities to players in the market. On the other hand, low market acceptance as compared to antibodies is likely to restrain the market growth while shortage of skilled & trained professionals may challenge market growth to a certain extent. Lower production cost and higher stability will drive the DNA-based aptamers segment growth Based on type, the aptamers market is segmented into DNA aptamers, XNA aptamers, and RNA aptamers. The DNA-based aptamers segment dominated the market in 2020. The large share of this segment is attributed to their lower production cost and higher stability compared to other nucleic acid-based aptamers and the wide availability of DNA aptamers. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=1167 Others segment is expected to witness the highest CAGR during the forecast period Based on technology, segmented into SELEX and other technologies. The SELEX technology segment dominated the market in 2020. The segment accounts for a large share of the aptamers market as SELEX is one of the most widely used technologies. The other technologies segment is expected to register the highest CAGR during the forecast period due to the increasing focus on developing technologies for aptamer selection. North America was the largest regional market for aptamer market in 2020 The global aptamers market is segmented into five major regions, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2020, North America accounted for the largest share of the market. The largest share of North America is attributed to the availability of funds to develop innovative technologies, the presence of prominent market players, and growing collaborations among companies. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=1167 Some of the prominent players operating in Aptamers Market include Aptamer Group (UK), Raptamer Discovery Group (US), SomaLogic Inc. (US), Aptamer Sciences, Inc. (South Korea) and Aptagen, LLC (US).  The Research Report on "Body Composition Analyzers Market by Product (Bio-impedance analyzer/DEXA/Skinfold calipers/ADP/Hydrostatic weighing), & End-users (Hospitals/Fitness & wellness centers/Academic & Research Center/Home-users) - Analysis & Global Forecast", analyzes and studies the major market drivers, restraints/challenges, and opportunities. The Body Composition Analyzers Market is poised to reach USD 668.16 Million, growing at a CAGR of 12.7%, during the forecast period. The Body composition analysis is the process to evaluate the amount of fat, muscle, and bone in the body. It gives the precise measurement of body fat in relation to lean body mass. Evaluation of body composition is essential in order to determine the risks associated with high or low levels of body fat. The growth of the overall body composition analyzers market can be contributed to rise in obese population across the globe, growing health and fitness consciousness among people, increasing government initiatives to encourage physical activity and technological advancements. In the coming years, the body composition analyzers market is expected to witness the highest growth rate in the Asia-Pacific region. North America is expected to account for the largest share of the global body composition analyzers market. However, inconsistency in the accuracy of different analyzers and high cost of equipment is likely to restrain the growth of the market during the forecast period. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=248209133 Industry Segmentation In Detailed: The global body composition analyzers market is segmented on the basis of product type, end users and region. Based on product, the market is segmented into bio-impedance analyzer, dual energy X-ray absorptiometry (DEXA), skin fold Calipers, air displacement plethysmography (ADP) and hydrostatic weighing. The bio-impedance analyzer is expected to account for the largest share of the body composition analyzers market, by product in 2016 and is expected to grow at highest CAGR. This large share can be attributed to the simplicity, low cost, and better accuracy as compared to other body composition analyzers. Based on end users, the market is segmented into hospitals, fitness clubs and wellness centers, academic and research centers. In 2016, hospitals segment is estimated to account for the largest share of the body composition analyzer market, by end users in 2016 and is expected to grow at highest CAGR. The growth of this segment can be attributed to the rise in osteoporosis cases, increasing adoption of body composition analyzers to assess the nutritional status in patients and increasing health consciousness among masses. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=248209133 Leading Key Players and Analysis: Key players in this Body Composition Analyzers Market includes Tanita Corporation (Japan), Omron Corporation (Japan), InBody Co., Ltd (South Korea), Hologic, Inc. (U.S.) and GE Healthcare (U.S.) among others. These players are increasingly undertaking mergers and acquisitions, and product launches to develop and introduce new technologies and products in the market. Geographical Analysis in Detailed: The Body Composition Analyzers Market is divided into North America, Europe, Asia-Pacific, and the Rest of the World (RoW). In 2016, North America is expected to account for the largest share of the body composition analyzer market. Its large share can be attributed to rising obesity rates and increasing health clubs and fitness centers in the U.S. However, the Asia-Pacific market is slated to grow at the highest CAGR during the forecast period due to rising trend of overweight and obesity in China, and foothold of local players in Japan. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=248209133 |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed