The Research Report on “In Vivo Toxicology Market by Product (Animal Models, Reagents & Kits), Test Type (Chronic, Sub-acute), Toxicity Endpoints (Systemic, Immunotoxicity), Testing Facility (Outsourced, In-house), End User (Academic & Research Institute, CROs) – Forecast to 2025“, the global in vivo toxicology testing market size is projected to reach USD 6.6 billion by 2025, at a CAGR of 5.5% between 2020 and 2025. Driver: Increasing pharmaceutical R&D activities; Changing dynamics in the healthcare markets across the globe have compelled pharmaceutical and biotechnology companies to develop products that offer real value rather than just incremental benefits. Owing to this, an increasing number of pharma companies and medical device manufacturers focus on innovation and increasing their R&D efficiencies. R&D activities, however, are associated with a high risk of failure. One estimate is that for every 10,000 compounds synthesized in the discovery phase, only 250 reach the preclinical phase, ultimately resulting in one approved drug by the FDA (Source: National Center for Biotechnology Information). Thus, it is very important to bring down the attrition of failing molecules in the early stages of drug development. The primary goal of R&D is to increase the overall likelihood of approval of Phase I candidates by increasing the acceptance of the compounds in the preclinical stages. To achieve this, intensive R&D is conducted in the early stages of drug development. Increased R&D investments in the initial stages of drug development are likely to increase the use of in vivo toxicology methods before the drug reaches the more expensive clinical stage. According to the Biotechnology Industry Organization (BIO) 2019, nearly 82.7% of the venture capital investment in the US by emerging growth companies (EGCs) over the last decade was in R&D for emerging therapeutics and novel drugs. Likewise, ~50% of the venture capital investment for therapeutics was for developing biologic molecules/metabolites. Companies are also investing in research to develop breakthrough molecules/metabolites to cater to growing demands in the healthcare industry Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=105308811 Industry Segmentation In Detailed: The immunotoxicity segment accounted for the largest share of the in vivo toxicology market Based on toxicity endpoint, segmented into immunotoxicity, systemic toxicity, carcinogenicity, genotoxicity, developmental & reproductive toxicity (DART), and other toxicity endpoints (includes organ toxicity, endocrine disruptor toxicity, juvenile toxicity, phototoxicity, ocular toxicity, and skin irritation). In 2019, the immunotoxicity segment accounted for the largest share of the global in vivo toxicology testing market, followed by the systemic toxicity segment.The rising demand for the development of biologics and biosimilars is driving the growth of the immunotoxicity segment The chronic test type segment accounted for the largest share of the in vivo toxicology market Based on test type, segmented into acute, sub-acute, sub-chronic, and chronic test type. The chronic test type segment is expected to dominate the market during the forecast period. In 2019, the chronic test type segment held the largest share of the market, followed by sub-chronic test type.Increasing research on drugs used for longer-duration therapy such as anti-cancer, anti-convulsive, anti-arthritis, and anti-hypertensives drives the growth of the chronic test type market. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=105308811 Leading Key Players and Analysis: The major players operating in In Vivo Toxicology Market are by Charles River Laboratories (US), The Jackson Laboratory (US), Envigo (US), Taconic Biosciences, Inc. (US), and JANVIER LABS (France), Thermo Fisher Scientific (US), Danaher Corporation (US), Waters Corporation (US), Agilent Technologies (US), Shimadzu Corporation (Japan), Bruker Corporation (US), PerkinElmer (US). Other prominent players include Merck KGaA (Germany), GE Healthcare (US), and Bio-Rad Laboratories (US), genOway (France), Cyagen Biosciences (US), GVK BIO (India), PolyGene (Switzerland), Crown Biosciences (US), TransCure bioServices (France), Ozgene Pty Ltd. (Australia), Harbour BioMed (US) among others. Charles River Laboratories (US) has extensive portfolio of animal models, particularly mice models and services. With more than 70 years of experience, the company has built upon its core competency in the field of in vivo biology through its diverse products and services portfolio. It offers products, services, and solutions that focus specifically on early-stage drug discovery and preclinical development. Its strong portfolio enables it to increase collaboration with clients, from early lead generation to candidate selection. Charles River Laboratories has nearly 90 facilities spread across 20 countries. The company has its presence in the US, Canada, the UK, France, Italy, Spain, the Netherlands, Belgium, Germany, Poland, Ireland, Finland, Luxembourg, Japan, China, India, South Korea, Hong Kong, and Australia. Geographical Analysis in Detailed: The global in vivo toxicology market is segmented into North America, Europe, the Asia Pacific, Latin Ametica and Middle East & Africa. In 2019, North America accounted for the largest share of the in vivo toxicology testing market. The large share of the North America region can be attributed to the presence of major players operating in the toxicology market in the US, growing biomedical research in the US, and rising preclinical activities by CROs and pharmaceutical companies in the region. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=105308811

0 Comments

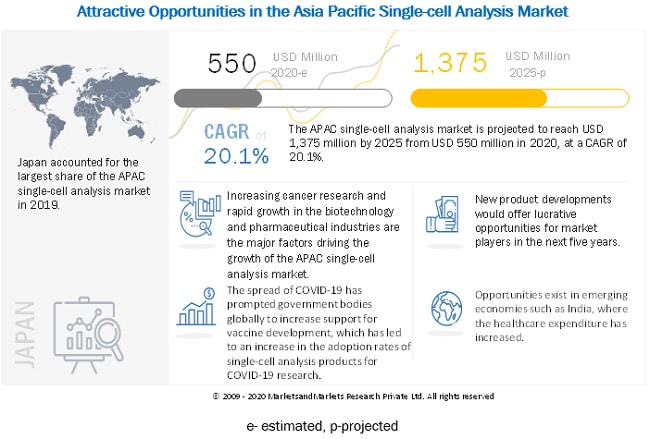

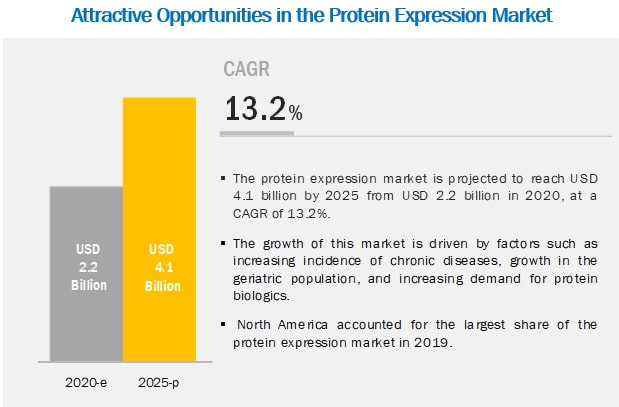

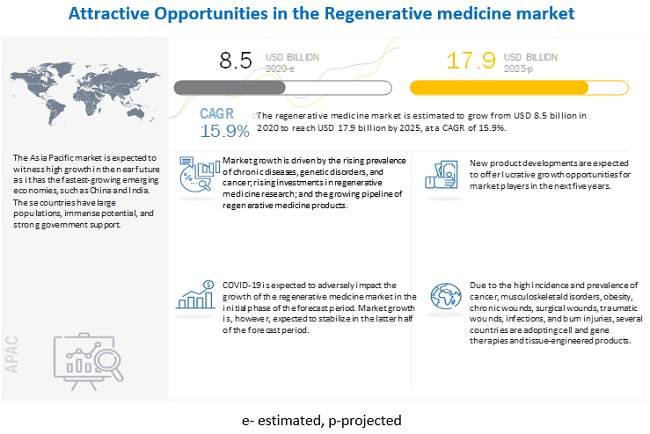

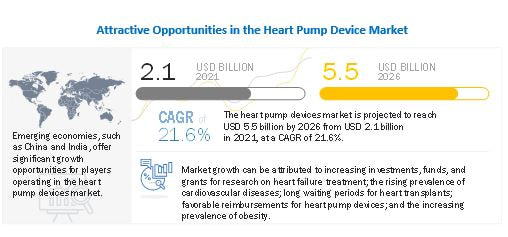

The Research Report on “Asia Pacific Single-cell Analysis Market by Cell Type (Human, Animal, Microbial), Product (Reagent, Assays, Instruments), Technique (Flow Cytometry, NGS, PCR), Application (Cancer, Stemcell, IVF), End User (Academic, Research Labs) – Forecast to 2025″, is projected to reach USD 1,375 million by 2025 from USD 550 million in 2020, at a 20.1% CAGR. Growth Opportunity: High growth potential of single-cell sequencing; Single-cell sequencing (SCS) helps understand the transcriptional stochasticity and cellular heterogeneity in more detail. It assists in the investigation of small groups of differentiating cells and circulating tumor cells. It also demonstrates the heterogeneity of gene expressions, interaction and regulations of gene regulatory networks, characteristics of putative cancer stem cells, gene expression profiles of intracellular compartments, mRNA locations, and allele-specific gene expression. Advancements in single-cell sequencing have improved the detection and analysis of infectious disease outbreaks, antibiotic drug-resistant strains, food-borne pathogens, and microbial diversities in the environment. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=257201069 Industry Segmentation In Detailed: The consumables segment accounted for the largest share of the Asia Pacific single-cell analysis market. Based on product, the APAC single-cell analysis market is segmented into consumables and instruments. The consumables segment accounted for the largest shareof the APAC single-cell analysis market in 2019. The frequent purchase of these products as compared to instruments, which are considered as a one-time investment, and their wide applications in research and genetic exploration, exosome analysis, and isolation of RNA and DNA are the major factors driving this segments growth. Animal cells segment to register the highest growth rate during the forecast period The Asia Pacific single-cell analysis market is segmented into human cells, animal cells, and microbial cells based on cell type. In 2019, the animal cells segment accounted for the highest growth rate. This can be attributed to the growth in the pharmaceutical industry and rising investments in animal cell research. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=257201069 Leading Key Players and Analysis: The major players operating in this market are Becton, Dickinson and Company (US), Danaher Corporation (US), Merck Millipore (US), QIAGEN N.V. (Netherlands), Thermo Fisher Scientific, Inc. (US), General Electric Company (US), Promega Corporation (US), Illumina, Inc. (US), Bio-Rad Laboratories (US), Fluidigm Corporation (US), Agilent Technologies, Inc. (US), Tecan Group Ltd. (Switzerland), Sartorius AG (Germany), Luminex Corporation (US), Takara Bio (Japan), 10x Genomics (US), Fluxion Biosciences (US), Menarini Silicon Biosystems, Inc. (Italy), bioMérieux SA (France), Oxford Nanopore Technologies (UK), Cytek Biosciences (US), Corning Incorporated (US), Apogee Flow Systems Ltd. (UK), NanoCellect Biomedical (US), and On-chip Biotechnologies Co., Ltd. (Japan). Danaher Corporation accounted for the second-largest share of the Asia Pacific single-cell analysis market in 2019. The company offers a broad range of products in the single-cell analysis market, including flow cytometers, cell counters, mass spectrometers, reagents, and kits. The company adopts the strategies of product launches and acquisitions. Over the years, Danaher has acquired several players operating in the single-cell analysis market, such as Beckmann Coulter and Molecular Devices. Geographical Analysis in Detailed: The APAC single-cell analysis market is segmented into Japan, China, India, South Korea, Singapore, Australia, Southeast Asia, and the Rest of Asia Pacific. In 2019, Japan accounted for the largest share of the Asia Pacific single-cell analysis market. This can be attributed to the rising geriatric population, increasing government initiatives to promote life science research, increasing investments in biotech R&D, and the growing focus on personalized medicine. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=257201069  MarketsandMarkets Research Report’s View on Revenue Impact? The Global Protein Expression Market size is projected to reach USD 4.1 billion by 2025 from USD 2.2 billion in 2020, at a CAGR of 13.2% between 2020 and 2025. Factors Responsible for Growth and Recent Developments? The increasing incidence of chronic diseases, growth in the geriatric population, and increasing demand for protein biologics are the significant factors driving the growth of the protein expression industry. Emerging economies are likely to create substantial growth opportunities for players in the market. – In 2020, Thermo Fisher Scientific Inc. acquired the biotechnology company, Qiagen (Germany). This acquisition will help Thermo Fisher Scientific to enhance its precision medicine portfolio through molecular diagnostics and improved life sciences solutions. – In 2020, Merck announced plans for the construction of a new biotech development facility in Switzerland. The company will be investing USD 282.5 million for this purpose. This facility is going to strengthen the company’s presence in the protein expression market. – In 2019, Agilent Technologies acquired BioTek Instruments (US). This acquisition expanded Agilent’s presence and expertise in cell analysis and strengthened its position in the growing immune-oncology and immunotherapy areas. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=180323924 Leading Key Players and Analysis: The prominent players in protein expression market include Thermo Fisher Scientific Inc. (US), Merck KGaA (Germany), Agilent Technologies, Inc. (US), Genscript Biotech Corporation (US), Takara Bio, Inc. (Japan), Bio-Rad Laboratories (US), Lonza (US), Promega Corporation (US), New England Biolabs (US), Oxford Expression Technologies Ltd. (US), and Synthetic Genomics Inc. (US). Thermo Fisher Scientific Inc. is the largest player in the protein expression market. The large share of this company can be attributed to its robust suite of expression vectors, reagents, competent cells, and instruments. Owing to its strong sales and distribution network, the company has a significant global footprint. Additionally, the large number of production sites give it a competitive advantage over other players in the protein expression market. The company focuses on product launches to create a strong foothold in the market. In 2018, Thermo Fisher Scientific Inc. launched the Gibco ExpiSf System, the first-ever chemically defined protein expression system. The company further intends to strengthen its presence in this market by investing in R&D. Its extensive R&D activities enable it to increase its depth of capabilities in protein expression solutions and services and to provide innovative products and services in the market space. Geographical Analysis in Detailed? In 2019, North America dominated the protein expression sector, followed by Europe. The major factors driving the growth of this market include the increasing incidence of chronic diseases, growth in the geriatric population, and increasing demand for protein biologics. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=180323924 Industry Segmentation: The prokaryotic expression systems segment accounted for the largest share of the protein expression market. Based on system type, segmented into prokaryotic expression systems, mammalian cell expression systems, insect cell expression systems, yeast expression systems, cell-free expression systems, and algal-based expression systems. The prokaryotic expression systems segment accounted for the largest share of the global protein expression market in 2019. The large share of this segment is attributed to the low cost and ease of use of prokaryotic expression systems. The reagents segment accounted for the largest share of the protein expression industry in 2019. Based on product and service, the protein expression industry is segmented into reagents, expression vectors, competent cells, instruments, and services. The reagents segment accounted for the largest share of the market in 2019. The large share of this segment is mainly due to the increasing research activities in the field of protein expression and the large-scale production of antibodies and vaccines. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=180323924  MarketsandMarkets Research Report’s View on Revenue Impact? The Global Regenerative Medicine Market is expected to reach USD 17.9 billion by 2025 from USD 8.5 billion in 2020, at a CAGR of 15.9%. Factors Responsible for Growth and In-Depth Analysis? The Regenerative Medicine Market growth is driven by the rising prevalence of chronic diseases, genetic disorders, and cancer; rising investments in regenerative medicine research; and the growing pipeline of regenerative medicine products. However, the high cost of cell and gene therapies and ethical concerns related to the use of embryonic stem cells in research and development are expected to restrain the growth of this market during the forecast period. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=65442579 Leading Key Players and Analysis: The major players operating in this market are 3M (US), Allergan plc (Ireland), Amgen, Inc. (US), Aspect Biosystems (Canada), bluebird bio (US), Kite Pharma (US), Integra LifeSciences Holdings Corporation (US), MEDIPOST Co., Ltd. (South Korea), Medtronic plc (Ireland), Anterogen Co., Ltd. (South Korea), MiMedx Group (US), Misonix (US), Novartis AG (Switzerland), Organogenesis Inc. (US), Orthocell Limited (Australia), Corestem, Inc. (South Korea). Novartis AG (Switzerland) is one of the the largest player in the regeneartive medicine market in 2019. In order to maintain its position in the market, the company has been focusing on the innovations, and breakthrough product approvals for the treatment of cancer. For instance, in August 2017, Novartis received the FDA approval for CAR-T cell therapy, Kymriah (CTL019), which is used for the treatment of cancer. Kymriah got the EU approval in August 2018. Novartis also focused on the inorganic strategies in order to enhance their dominance in the regenerative medicine market. For instance, Novartis received EU approval for one-time gene therapy, Luxturna, developed by Spark Therapeutics, to restore vision in people with rare and genetically-associated retinal disease. Geographical Analysis in Detailed? The regenerative medicine market is segmented into four major regions, namely, North America, Europe, Asia Pacific, and the Rest of the World (RoW). In 2019, North America accounted for the largest share in the market. The growth in the North American market can be attributed to rising stem cell banking, tissue engineering, and drug discovery in the region; expansion of the healthcare sector; and the high adoption of stem cell therapy and cell immunotherapies for the treatment of cancer and chronic diseases. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=65442579 Industry Segmentation: Tissue-engineered products segment accounted for the largest share of the regenerative medicine market. Based on products, segmented into tissue-engineered products, cell therapies, gene therapies, and progenitor and stem cell therapies. The tissue-engineered products segment accounted for the largest share in the regenerative medicine market in 2019. The increasing adoption of tissue-engineered products for the treatment of chronic wounds and musculoskeletal disorders and the rising funding for the R&D of regenerative medicine products and therapies are the major factors driving the growth of this segment. Musculoskeletal segment accounted for largest share in the market. Based on applications, the regenerative medicine market is segmented into musculoskeletal disorders, wound care, oncology, ocular disorders, dental, and other applications. In 2019, the musculoskeletal disorders segment accounted for the largest market share. This can be attributed to the rising prevalence of orthopedic diseases, growing geriatric population, increasing number of stem cell research projects, growing number of clinical researches/trials, and the rich pipeline of stem cell products for the treatment of musculoskeletal disorders. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=65442579  MarketsandMarkets Research Report’s View on Revenue Impact? The Heart Pump Device Market is projected to reach USD 5.5 billion by 2026 from USD 2.1 billion in 2021, at a CAGR of 21.6% from 2021 to 2026. Factors Responsible for Growth and In-Depth Analysis? The Heart pump devices are used by patients suffering from cardiac diseases and patients waiting for a heart transplant. These devices are also used to provide the necessary support to patients recovering from a major surgical procedure. Factors such as increasing investments, funds, and grants for research on heart failure treatment; rising prevalence of cardiovascular diseases; long waiting periods for heart transplants; favorable reimbursements for heart pump devices; and increasing obesity are expected to drive the growth of the market. The Asia Pacific market is estimated to be the fastest-growing regional market, mainly due to the growing target population, active product launches & approvals by players in the region, and healthcare infrastructure improvements in several APAC countries such as China, Japan, and India. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=237125725 Leading Key Players and Analysis: The major players operating in Heart Pump Device Market are Abbott Laboratories (US), Abiomed (US), Medtronic (Ireland), Teleflex Incorporated (US), SynCardia Systems (US), Fresenius Medical Care AG & Co. KGaA (Germany), Getinge (Sweden), CardiacAssist, Inc. (US), Berlin Heart (Germany), Jarvik Heart, Inc. (US), CARMAT (France), SENKO MEDICAL INSTRUMENT Mfg. CO., LTD. (Japan), Angiodroid (Italy), CardioDyme (US), and World Heart Corporation (US). Abbott Laboratories occupied the leading position in the heart pump devices market, with a share of 30.6% in 2020. In the heart pump devices market, the company offers VADs to treat heart failure in patients. The company has consistently adopted strategic initiatives over the years, helping it gain a competitive edge in the market. In 2020, the FDA approved the updated labeling for the HeartMate 3 Heart Pump to be used in pediatric patients with advanced refractory left ventricular heart failure. The company is also extremely innovation-centric and invests heavily in R&D to maintain its market share. It has a strong presence in the US; in 2020, it registered ~37.6% of its total revenue from the US. Geographical Analysis in Detailed? The heart pump device market is segmented into North America, Europe, Asia Pacific, and the Rest of the World. In 2020, Europe commanded the largest share of the market. The large share of this market segment can be attributed to the rising adoption of heart pump devices, the high prevalence of CVDs, the growing number of research activities to improve current technologies, and the limited availability of donor hearts for transplants. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=237125725 Industry Segmentation: Ventricular assist devices are expected to hold the largest share of the heart pump device market. Based on products, segmented into ventricular assist devices, intra- aortic balloon pumps, and total artificial hearts. Ventricular assist devices are the largest and fastest-growing segment in this market. Growth in this segment can primarily be attributed to technological advancements, the shortage of organ donors, and the increasing prevalence of heart failure globally. Implantable heart pump devices are expected to hold the largest share of the heart pump device market. Based on type, segmented into implantable heart pump devices and extracorporeal heart pump devices. In 2020, implantable heart pump devices accounted for the largest share of this market, due to the introduction of innovative products by leading players and the rising need for an efficient solution to manage heart failure. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=237125725 MarketsandMarkets analysis says that a Potential Opportunity Worth $50 Bn is opening up in Genomics1/12/2022 As Genome Sequencing heads to $100 Direct-to-Consumer, a potential opportunity worth $50 Bn is expected to open up, leading to a million terabytes of genome data by 2025.

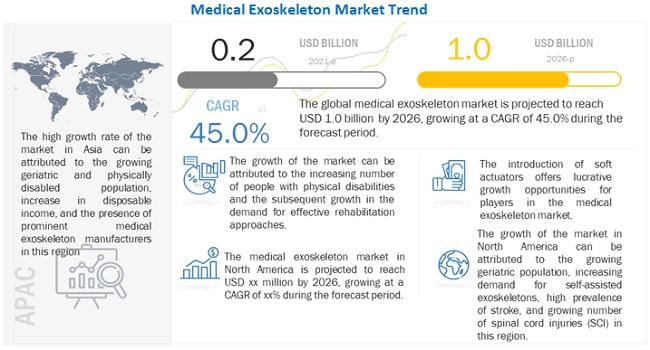

The genome sequencing market will reach $25 Bn by 2026, further intensified by COVID-19, and oncology and rare disease diagnostics coupled with pan genome studies. Adjacent markets of data storage, high performance computing (HPC), lab automation, and AI are anticipated to see unlocking of a further $20 Bn. According to MarketsandMarkets analysis,

MarketsandMarkets is focused on high-growth, niche markets, such as AI in genomics, spatial genomics & transcriptomics, liquid biopsy, single-cell analysis, and related markets, providing a comprehensive understanding of the entire genomics ecosystem through the World’s First Market Intelligence Cloud, 'KnowledgeStore'. It helps find blind spots in clients’ revenue decisions because of interconnections and unknowns that impacting clients and their client’s clients. For more details, please visit: https://www.marketsandmarkets.com/practices/genomics-new.asp Press Release: https://www.marketsandmarkets.com/PressReleases/genomics.asp MarketsandMarkets™ Research Report’s View on Revenue Impact? The Global In Vivo Toxicology Market size is projected to reach USD 6.6 billion by 2025 from USD 5.0 billion in 2020, at a CAGR of 5.5% during the forecast period. Factors Responsible for Growth and In-Depth Analysis? The Changing dynamics in the healthcare markets across the globe have compelled pharmaceutical and biotechnology companies to develop products that offer real value rather than just incremental benefits. Owing to this, an increasing number of pharma companies and medical device manufacturers focus on innovation and increasing their R&D efficiencies. R&D activities, however, are associated with a high risk of failure. One estimate is that for every 10,000 compounds synthesized in the discovery phase, only 250 reach the preclinical phase, ultimately resulting in one approved drug by the FDA (Source: National Center for Biotechnology Information). Thus, it is very important to bring down the attrition of failing molecules in the early stages of drug development. The primary goal of R&D is to increase the overall likelihood of approval of Phase I candidates by increasing the acceptance of the compounds in the preclinical stages. To achieve this, intensive R&D is conducted in the early stages of drug development. Increased R&D investments in the initial stages of drug development are likely to increase the use of in vivo toxicology methods before the drug reaches the more expensive clinical stage. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=105308811 Leading Key Players and Analysis: The major players operating in In Vivo Toxicology Market are by Charles River Laboratories (US), The Jackson Laboratory (US), Envigo (US), Taconic Biosciences, Inc. (US), and JANVIER LABS (France), Thermo Fisher Scientific (US), Danaher Corporation (US), Waters Corporation (US), Agilent Technologies (US), Shimadzu Corporation (Japan), Bruker Corporation (US), PerkinElmer (US). Other prominent players include Merck KGaA (Germany), GE Healthcare (US), and Bio-Rad Laboratories (US), genOway (France), Cyagen Biosciences (US), GVK BIO (India), PolyGene (Switzerland), Crown Biosciences (US), TransCure bioServices (France), Ozgene Pty Ltd. (Australia), Harbour BioMed (US) among others. Charles River Laboratories International, Inc. (US) has extensive portfolio of animal models, particularly mice models and services. With more than 70 years of experience, the company has built upon its core competency in the field of in vivo biology through its diverse products and services portfolio. It offers products, services, and solutions that focus specifically on early-stage drug discovery and preclinical development. Its strong portfolio enables it to increase collaboration with clients, from early lead generation to candidate selection. Charles River Laboratories has nearly 90 facilities spread across 20 countries. The company has its presence in the US, Canada, the UK, France, Italy, Spain, the Netherlands, Belgium, Germany, Poland, Ireland, Finland, Luxembourg, Japan, China, India, South Korea, Hong Kong, and Australia. Geographical Analysis in Detailed? The global in vivo toxicology market is segmented into North America, Europe, the Asia Pacific, Latin Ametica and Middle East & Africa. In 2019, North America accounted for the largest share of the market. The large share of the North America region can be attributed to the presence of major players operating in the market in the US, growing biomedical research in the US, and rising preclinical activities by CROs and pharmaceutical companies in the region. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=105308811 Industry Segmentation: Chronic test type accounted for the largest share in the in vivo toxicology market in 2019 Based on test type, segmented into acute, sub-acute, sub-chronic, and chronic test type. The chronic test type segment is expected to dominate the market during the forecast period. In 2019, the chronic test type segment held the largest share of the market, followed by sub-chronic test type.Increasing research on drugs used for longer-duration therapy such as anti-cancer, anti-convulsive, anti-arthritis, and anti-hypertensives drives the growth of the chronic test type market. Academic and research institutes accounted for the largest share the in vivo toxicology market. Based on the end user, segmented into academic & research institutes, pharmaceutical & biotechnology companies, contract research organizations, and other end users (cosmetic companies and food laboratories). The academic and research institutes segment accounted for the largest share of the in vivo toxicology market in 2019. The increasing number of research activities in the field of in vivo toxicology and funding to the academic and research institutes to conduct in vivo toxicology research are the factors responsible for the largest share of the segment Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=105308811 MarketsandMarkets Research Report’s View on Revenue Impact? The Asia Pacific Single-cell Analysis Market is projected to reach USD 1,375 million by 2025 from USD 550 million in 2020, at a CAGR of 20.1%. Factors Responsible for Growth and In-Depth Analysis? The rising incidence of infectious diseases, increasing pandemics frequency, increasing R&D in the pharmaceutical and biotechnology industries for complex diseases, growth in stem cell research, and the rising prevalence of cancer are the major factors driving the growth of Asia Pacific single-cell analysis market. However, the high cost of single-cell analysis products is a major factor hampering the growth of the single-cell analysis market. Emerging economies such as Japan and China are providing lucrative opportunities for the players operating in the APAC single-cell analysis market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=257201069 Leading Key Players and Analysis: The major players operating in Asia Pacific Single-cell Analysis Market are Becton, Dickinson and Company (US), Danaher Corporation (US), Merck Millipore (US), QIAGEN N.V. (Netherlands), Thermo Fisher Scientific, Inc. (US), General Electric Company (US), Promega Corporation (US), Illumina, Inc. (US), Bio-Rad Laboratories (US), Fluidigm Corporation (US), Agilent Technologies, Inc. (US), Tecan Group Ltd. (Switzerland), Sartorius AG (Germany), Luminex Corporation (US), Takara Bio (Japan), 10x Genomics (US), Fluxion Biosciences (US). Danaher Corporation accounted for the second-largest share of the Asia Pacific single-cell analysis market in 2019. The company offers a broad range of products in the single-cell analysis market, including flow cytometers, cell counters, mass spectrometers, reagents, and kits. The company adopts the strategies of product launches and acquisitions. Over the years, Danaher has acquired several players operating in the single-cell analysis market, such as Beckmann Coulter and Molecular Devices. Geographical Analysis in Detailed? Japan dominated the single-cell analysis market in Asia Pacific region The Asia Pacific single-cell analysis market is segmented into Japan, China, India, South Korea, Singapore, Australia, Southeast Asia, and the Rest of Asia Pacific. In 2019, Japan accounted for the largest share of the single-cell analysis market. This can be attributed to the rising geriatric population, increasing government initiatives to promote life science research, increasing investments in biotech R&D, and the growing focus on personalized medicine. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=257201069 Industry Segmentation: The consumables segment accounted for the largest share of the Asia Pacific single-cell analysis market. Based on product, segmented into consumables and instruments. The consumables segment accounted for the largest shareof the APAC single-cell analysis market in 2019. The frequent purchase of these products as compared to instruments, which are considered as a one-time investment, and their wide applications in research and genetic exploration, exosome analysis, and isolation of RNA and DNA are the major factors driving this segments growth. Animal cells segment to register the highest growth rate during the forecast period The Asia Pacific single-cell analysis market is segmented into human cells, animal cells, and microbial cells based on cell type. In 2019, the animal cells segment accounted for the highest growth rate. This can be attributed to the growth in the pharmaceutical industry and rising investments in animal cell research. The academic & research laboratories segment accounted for the largest share of the Asia Pacific single-cell analysis market. Based on end-user, the APAC single-cell analysis market is segmented into academic & research laboratories, biotechnology & pharmaceutical companies, hospitals & diagnostic laboratories, and cell banks & IVF centers. In 2019, the academic & research laboratories segment accounted for the largest share of the single-cell analysis market. The increasing funding for life science research, increasing number of medical colleges and universities, and the increasing number of collaborations among research institutes and life science research companies are the major factors driving the growth of this end-user segment. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=257201069  According to the new market research report “Medical Exoskeleton Market by Component (Hardware (Sensor, Actuator, Control System, Power Source), Software), Type (Powered, Passive), Extremities (Lower, Upper and Full Body) & Mobility (Mobile, Stationary) – Global Forecasts to 2026″, published by MarketsandMarkets™, is projected to reach USD 1.0 billion by 2026, from USD 0.2 billion in 2021, at a CAGR of 45.0%. Browse in-depth TOC on “Medical Exoskeleton Market” 96 – Tables 38 – Figures 178 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=138546702 The growth of this market is mainly driven by factors such as the increasing number of people with physical disabilities and subsequent growth in the demand for effective rehabilitation approaches; agreements and collaborations among companies and research organizations for the development of the exoskeleton technology, and increasing insurance coverage for medical exoskeletons in several countries driving the growth of the medical exoskeleton market. However, the high cost of medical exoskeletons may restrict market growth to a certain extent. The companies have a large market spread across various countries in North America, Europe, Asia, and the Rest of the World. Impact of Covid-19 on The Medical Exoskeleton Market As of September 2021, more than 220 million confirmed cases of COVID-19 were reported globally, with more than 4.5 million deaths (Source: WHO). This situation has compelled governments across the world to take proactive measures to contain the outbreak. The COVID-19 pandemic had a negative impact on the market in 2020, with small and medium-sized companies struggling to sustain their businesses. The medical exoskeleton market is witnessing a variable growth trend, with some countries offering some growth potential while others are facing closures and low profit margins. Major exoskeleton providers, such as Ekso Bionics, ReWalk Robotics, and Hocoma AG, have incurred a reduction in overall revenue for the fiscal year 2020 due to a decline in the demand for exoskeleton systems. Manufacturers are likely to adjust production to prevent bottlenecks and plan production according to the demand from OEMs. Tier 1 players experienced a decline in revenue in the remaining quarters of 2020. Moreover, medical exoskeleton manufacturers are facing disruptions in supply chains as countries are under lockdown to prevent the spread of the disease. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=138546702 The hardware segment accounted for the largest share 78.6% of the medical exoskeleton market by component, segmented into hardware and software. The hardware segment is expected to account for the largest share 78.6% of the medical exoskeleton market in 2020. The dominant share of this segment is attributed to the fact that a large number of parts such as sensors, actuators, power sources, and control systems are required to manufacture exoskeletons. The lower extremity segment accounted for the largest share 63.0% of the medical exoskeleton market By extremity, segmented into lower extremity medical exoskeletons and upper extremity medical exoskeletons and Full Body extremity medical exoskeletons. In 2020, the lower extremity medical exoskeletons segment is expected to account for a larger share of 63.0% of the market. Lower extremity exoskeletons provide stability to paralyzed and geriatric patients and offer weight-bearing and locomotion capabilities. As a result, their adoption is higher in the rehabilitation of patients. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=138546702 North America accounted for the largest share 44.4%. of the global medical exoskeleton market Based on the region, segmented into North America, Europe, Asia, and the Rest of the World (RoW). In 2020, North America is expected to dominate the market with a share of 44.4%. The growing geriatric population, increasing demand for self-assist exoskeletons, high prevalence of stroke, and growing number of spinal cord injuries (SCI) are the key factors driving the growth of the exoskeleton market in this region. Some of the leading players in the Medical exoskeleton market include Key players in this market are Ekso Bionics Holdings, Inc. (US), ReWalk Robotics Ltd. (Israel), Parker Hannifin Corp (US), CYBERDYNE Inc. (Japan), Bionik Laboratories Corp (Canada), Rex Bionics Ltd. (UK), B-TEMIA Inc. (Canada), Hocoma AG (a subsidiary of DIH Technologies) (Switzerland), Wearable Robotics SRL (Italy), Gogoa Mobility Robots SL (Spain), and ExoAtlet (Luxembourg)  MarketsandMarkets Research Report’s View on Revenue Impact? The Global Industrial Centrifuge Market is projected to reach USD 9.0 billion by 2025 from USD 7.2 billion in 2020, at a CAGR of 4.4% between 2020 and 2025. Factors Responsible for Growth and In-Depth Analysis? The increasing demand for centrifuges in process industries and the rising need for wastewater management solutions are the major factors driving the growth of industrial centrifuge market. Industrial centrifuges are used for the separation of two- or three-phase systems and have a range of industrial applications. Many process industries are increasingly using various types of centrifuge equipment for the separation of two or three immiscible phases. Some of these industries include chemical processing, food processing (including dairy and beverage industry), metal processing, mining and mineral processing, pharmaceutical and biotechnology industries, fuel and biofuel industries, wastewater processing, and pulp and paper industries. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=59612221 Leading Key Players and Analysis: Prominent players in Industrial Centrifuge Market are ANDRITZ AG (Austria), Alfa Laval Corporate AB (Sweden), GEA Group AG (Germany), Mitsubishi Kakoki Kaisha, Ltd. (Japan), Thomas Broadbent & Sons (UK), FLSmidth & Co. A/S (Denmark), Schlumberger Limited (US), Ferrum AG (Switzerland), Flottweg SE (Germany), SIEBTECHNIK TEMA (Germany), HEINKEL Drying & Separation Group (Germany), Gruppo Pieralisi – MAIP S.p.A. (Italy), SPX Flow Inc. (US), HAUS Centrifuge Technologies (Turkey), Elgin Separation Solutions (US), Comi Polaris Systems, Inc. (US), Dedert Corporation (US), US Centrifuge Systems (US), B&P Littleford (US), and Pneumatic Scale Angelus (US). Alfa Laval AB (Sweden) is the leading player in the decanter and separator centrifuge market. The company’s expertise, experience, and comprehensive capabilities in various industries and business functions, enables it to maintain its leading position in the market. The company has a wide global presence with operations in North America and Europe. The company focuses on achieving sustainable growth by enhancing its operating base and launching competitive technologies. In July 2019, Alfa Laval launched the ALDEC G3 VecFlow decanter for the industrial centrifuge market. Geographical Analysis in Detailed? North America accounted for the largest share of the industrial centrifuges market, followed by Europe. The high demand for crude oil, a large number of shale oil and gas drilling activities, government initiatives to manage wastewater, flourishing food processing industry, technological advancements, and government support for the development of innovative centrifugation systems are the key factors driving the growth of the industrial centrifuge market in North America. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=59612221 Industry Segmentation: Power industry accounted for the largest market share in 2019 On the basis of end users, the industrial centrifuge market is segmented into the chemicals industry, food and beverage industry, metal industry, mining industry, pharmaceutical and biotechnology industries, power plants, pulp and paper industry, wastewater treatment plants, and water purification plants. In 2019, the power industry segment accounted for the largest share of the market. Growing oil and gas exploration activities, the establishment of new power plants to cater to the rising energy needs in developing countries, and upgradation of existing power plants to make them more efficient and reliable are some of the factors that are expected to drive the growth of this segment. Vertical Centrifuge dominated the industrial centrifuge market in 2019 On the basis of design, segmented into vertical and horizontal centrifuges. In 2019, the vertical centrifuge segment accounted for the largest share of the market. Growth in this segment can be attributed to factors such as the ability of these centrifuges to attain high speeds and the high efficiency of separation. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=59612221 |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed