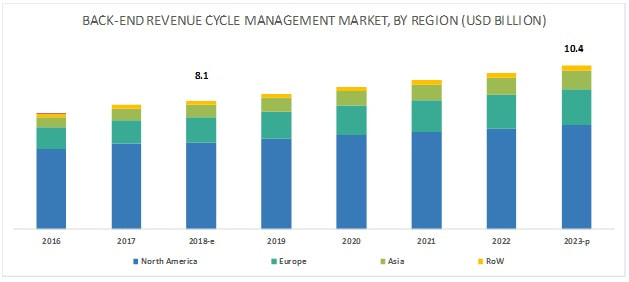

Back-end Revenue Cycle Management Market - Analysis of Worldwide Industry Trends and Opportunities6/30/2021  The report “Back-End Revenue Cycle Management Market by Product and Services (Claim Processing, Denial Management, Payment Integrity), Delivery Mode (On-Premise, Cloud Based), End-User (Payer, Provider (Inpatient, Outpatient)), and Region – Global Forecast to 2023″, is projected to reach USD 10.4 billion by 2023 from USD 8.1 billion in 2018, at a CAGR of 5.0%. The Growing importance of denials management; To reduce costs and maximize profits, insurance companies are increasingly denying claims as well as coverage to patients being treated for chronic or persistent illnesses. This is putting an extra burden on healthcare providers to manage operating costs, and in turn is supporting the adoption of back-end revenue cycle management solutions (with a growing number of healthcare providers focusing on properly analyzing denied claims and appealing them). Many healthcare providers across the globe still use manual and paper-oriented approaches to manage denials. This results in errors, delayed follow-ups, and miscommunication between healthcare providers and insurance companies. The use of back-end revenue cycle management solutions over manual and paper-oriented approaches can not only help healthcare providers overcome these issues but also help them save significant costs. As a result, the demand for back-end revenue cycle management solutions is expected to increase among end users during the forecast period. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=204439794 The Services segment to dominate the back-end revenue cycle management market. By product & service, segmented into software and services. The services segment is expected to account for the largest share of the revenue cycle management market in 2018. The large share of this segment can be attributed to the recurring nature of services such as training and development, installation, software upgrades, consulting, and maintenance. However, due to the need for periodic software upgrades, the software segment is expected to witness the highest growth during the forecast period. The cloud-based systems to register the highest CAGR during the forecast period On the basis of delivery mode, revenue cycle management market is segmented into on-premise and cloud-based systems. The cloud-based segment is expected to register the highest CAGR of the back-end revenue cycle management market during the forecast period. Growth in this segment can be attributed to the comparatively lower capital expenses and operational costs incurred in this model, alongside its scalability, flexibility, and affordability. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=204439794 Geographical View in-detailed: The back-end revenue cycle management market is divided into North America, Europe, Asia, and the Rest of the World (RoW). North America is expected to account for the largest share in 2018 owing to factors such as growing HCIT investments in the region and the presence of regulatory mandates. North America is followed by Europe and Asia. The market in Asia is relatively nascent; however, it is projected to be the fastest-growing market during the forecast period. Global Key Leaders: Athenahealth (US), Cerner Corporation (US), Allscripts Healthcare Solutions, Inc. (US), eClinicalWorks (US), Optum, Inc. (US), McKesson Corporation (US), Conifer Health Solutions (US), GeBBs Healthcare Solutions (US), The SSI Group (US), GE Healthcare (US), nThrive (US), DST Systems (US), Cognizant Technology Solutions (US), and Quest Diagnostics (US) are the key players in the back-end revenue cycle management market.

0 Comments

The report “Superdisintegrants Market by Product (Modified Starch, Modified Cellulose, Crospovidone, Ion Exchange Resin), Formulation (Tablet, Capsules), Therapeutic Area (Gastrointestinal, Cardiovascular, Neurology, Oncology, Hematology) – Global Forecast”, is expected to reach USD 536.5 million, at a CAGR of 7.9%.

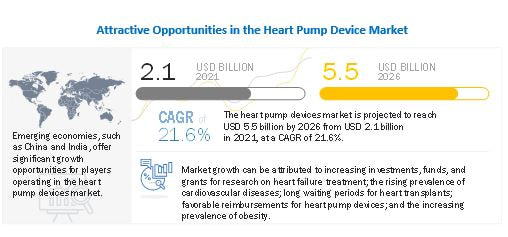

The increasing adoption of orally disintegrating tablets, the growing generics market, and the emergence of new superdisintegrants for the pharmaceutical industry are factors driving the market for superdisintegrants. The shifting focus of pharmaceutical manufacturing to emerging markets and the growth of the overall pharmaceutical market in these markets present significant opportunities for market growth. However, safety and quality concerns are expected to challenge the growth of the superdisintegrants market to a certain extent during the forecast period. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=198068672 The tablets segment is expected to hold the largest share in 2018 Based on formulation, is segmented into tablets and capsules. In 2018, the tablets segment is estimated to account for the largest share of the superdisintegrants market. Benefits such as stability, low manufacturing cost (as compared to other dosage forms), easy product identification, and compactness are driving the production of tablet formulations. The increasing focus on fast and orally disintegrating tablets is also contributing to the large share of this segment. Geographical View in-detailed: Europe is expected to account for the largest share of the superdisintegrants market in 2018, followed by North America and Asia Pacific. The large share of this region can be attributed to the presence of a number of pharmaceutical giants with large production capacities leading to high consumption of excipients. The growing emphasis on superior pharmaceutical products and generics is also expected to aid the market growth in the region. Moreover, a number of major global players are based in Germany. Global Key Leaders: The prominent players in the global superdisintegrants market are Ashland Inc. (US), BASF SE (Germany), DowDuPont (US), JRS Pharma (Germany), DFE Pharma (Germany), Roquette Freres (France), Asahi Kasei Corporation (Japan), Merck KGaA (Germany), Corel Pharma Chem (India), and Avantor Performance Materials, LLC (US). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=198068672 BASF was the leading player in the superdisintegrants market and accounted for the largest share in 2017. The company offers a well-balanced portfolio for the market. Its stronghold in the global pharmaceutical excipients market is primarily attributed to its innovative product portfolio and strong relationships with its customers. Additionally, having a large number of production sites gives it a competitive advantage over other players in the excipients market. The company also provides customized products to make customers’ production processes more efficient. To remain competitive in the market, the company focuses on expanding its presence across the globe. It opened Innovation Campus Asia Pacific in India with an initial investment of USD 2.76 million. By 2020, the company plans to conduct around 25% of its global R&D in Asia Pacific. Ashland was the second-largest market player in the superdisintegrants market in 2017. The company offers crospovidone for the largest market. Ashland’s prominent position in the market is attributed to its research and development activities, robust manufacturing capabilities, and an extensive distribution network across the world, which enables it to serve customers in over 100 countries. The company’s growth strategy for the pharmaceutical excipients business mainly concentrates on expanding its production capacity and meet the rising customer demand. The company majorly focuses on expansions to grow and maintain its position in the market.  The report “Heart Pump Device Market by Product (Ventricular Assist Devices (LVAD, RVAD, BiVAD, and pVAD), Intra-aortic Balloon Pumps, TAH), Type (Extracorporeal and Implantable Pumps), Therapy (Bridge-to-transplant, Destination Therapy) – Global Forecast to 2026” is projected to reach USD 5.5 billion by 2026 from USD 2.1 billion in 2021, at a CAGR of 21.6% from 2021 to 2026. Covid -19 Impact On The Heart Pump Device Market: There have been significant changes in the healthcare sector post the global outbreak of COVID-19. In the cardiac care sector, various countries have decided to postpone elective surgeries to lower the risk of exposure to the virus. In response to the burden of COVID‐19 on healthcare systems in the UK, elective cardiac surgeries have been delayed due to the redistribution of intensive care resources and the unquantifiable risk of acquiring COVID‐19. A study conducted across eight hospitals in Italy from 21st February to 31st March 2020 revealed that admissions for HF were significantly reduced during the lockdown. In fact, in some cases, HF patients may have died at home without seeking medical attention during the COVID‐19 lockdown. With reduced hospitalizations regarding HF, the market for heart pump devices witnessed a considerable decline in 2020. Similarly, players operating in the Heart Pump Device Market have also witnessed declines in their revenues owing to the outbreak of COVID-19. For instance, As per Abiomed’s 10-k form, revenues generated from the sales of Impella pumps were affected due to low patient utilization because of fewer patient visits in the fourth quarter of FY 2020. COVID-19 negatively impacted the revenue of Impella products by approximately USD 17 million, primarily in the US and Europe. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=237125725 Ventricular assist devices are expected to hold the largest share of the heart pump device market, by product in 2021. Based on products, the heart pump devices market is segmented into ventricular assist devices, intra- aortic balloon pumps, and total artificial hearts. Ventricular assist devices are the largest and fastest-growing segment in this market. Growth in this segment can primarily be attributed to technological advancements, the shortage of organ donors, and the increasing prevalence of heart failure globally. Europe commanded the largest share of the heart pump device market in 2021. On the basis of region, segmented into North America, Europe, Asia Pacific, and the Rest of the World. In 2020, Europe commanded the largest share of the market. The large share of this market segment can be attributed to the rising adoption of heart pump devices, the high prevalence of CVDs, the growing number of research activities to improve current technologies, and the limited availability of donor hearts for transplants. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=237125725 The major players operating in this market are Abbott Laboratories (US), Abiomed (US), Medtronic (Ireland), Teleflex Incorporated (US), SynCardia Systems (US), Fresenius Medical Care AG & Co. KGaA (Germany), Getinge (Sweden), CardiacAssist, Inc. (US), Berlin Heart (Germany), Jarvik Heart, Inc. (US), CARMAT (France), SENKO MEDICAL INSTRUMENT Mfg. CO., LTD. (Japan), Angiodroid (Italy), CardioDyme (US), and World Heart Corporation (US). Recent Developments in Heart Pump Device Market:

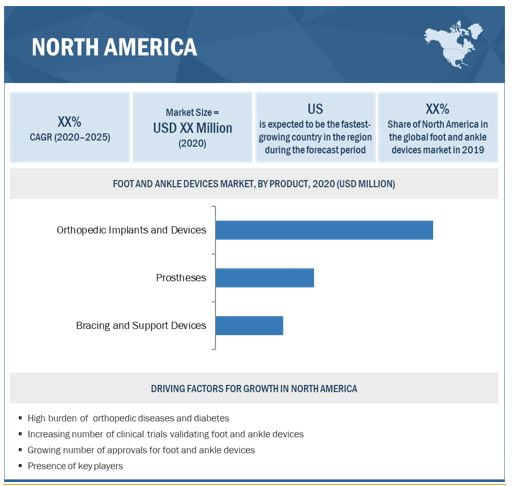

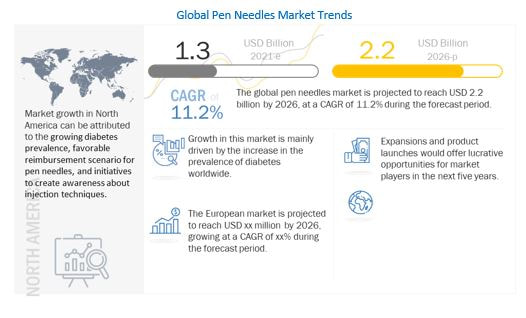

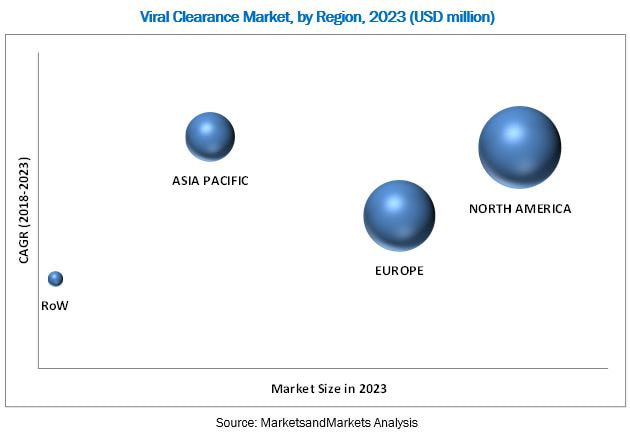

The report “Foot and Ankle Devices Market by Product (Implants, Plates, Screw, Wires, Internal Fixators, Braces, Prosthesis (SACH, Single/Multi-Axial)), Application (Rheumatoid Arthritis, Osteoporosis, Hammertoe), Enduser (Hospital, ASCs) – Global Forecasts to 2025″, is projected to reach USD 5.3 billion by 2025 from USD 3.9 billion in 2020, at a CAGR of 6.4% during the forecast period. The growth of this market is mainly driven by the growing number of hospitals across major markets, increasing awareness about complication related to foot and ankle related to osteoarthritis and diabetes coupled with the increasing adoption of bracing and support devices devices. Moreover, rising R&D investments by the key players operating in the market to develop advanced foot and ankle devices coupled with growing funding & grants for commercialization and development of foot and ankle devices are other important factors to drive the market growth in the near future. Growth Opportunity: Marketing, promotion and branding initiatives undertaken by major product manufacturers; Major product manufacturers are undertaking strategic initiatives to increase their brand visibility and product awareness among key end users (such as medical professionals, patients, and physiotherapists) across major healthcare markets worldwide. Company operating in foot and ankle devices market are opting for hybrid distribution strategy as per which distribution takes place both by distribution channel and through partnership with global orthopedic companies. Foot and ankle devices company has also adopted consignment model, accoding to which company first places the systems with its customers and sales are made according to the implementation of implants. Such initiatives undertaken by major product manufacturers are expected to increase their brand awareness among target end-users as well as sensitize them about their role in preventive care. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=845 The orthopedic implants and devices products segment dominated the global foot and ankle devices market Based on the product, segmented into orthopedic implants and devices, bracing and support devices, and prostheses. Orthopedic implants and devices products include joint implants, fixation devices, and soft tissue orthopedic devices. The orthopedic implants and devices segment dominated the market. Rising incidences of diabetes, new product launches, coupled with the rising adoption of branded orthopedic devices and implants because of better quality and lower risk associated with surgical site infection in emerging countries, is expected to drive the segment growth. The trauma & hair line fractures products segment dominated the global foot and ankle devices market Based on the application, segmented into trauma & hair line fractures, rheumatoid arthritis & osteoarthritis, diabetic foot diseases, ligament injuries, neurological disorders, hammertoe and others. The trauma and hair line fracture segment accounted for a larger share of in the market in 2019. The increasing prevalence of sport injuries and road accidents, growing number of foot and ankle reconstruction procedures related to fractures, rapid growth in the aging population across the globe, and the development of advanced foot and ankle products are factors expected to drive the growth of this market segment in the coming years. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=845 Geographical View in-detailed: North America, comprising the US and Canada, accounted for the largest share of the foot and ankle devices market in 2019. Increasing number of clinical trials validating foot and ankle devices and a growing number of approvals forfoot and ankle devices are the major factors driving market growth in North America. Customers in North America are moving towards ambulator surgical centers, which is increasing de,mand for foot and ankle devices. This trend will have a positive impact on the ankle devices market. DePuy Synthes Companies (US), Stryker Corporation (US), Zimmer Biomet Holdings, Inc (US), Smith & Nephew plc (UK), Arthrex Inc (US), Integra LifeSciences Holdings Corporation (US), DJO Finance, LLC (US), CONMED Corporation (US), Össur HF (Iceland), Orthofix Medical Inc. (US), Medartis AG (Switzerland), Acumed LLC (US), Extremity Medical (US), aap Implantate AG (Germany), Ottobock SE & Co. KGaA (Germany), Ortho Solutions UK Ltd. (UK), Vilex in Tennessee, Inc. (US), Advanced Orthopaedic Solutions (US), Fillauer LLC (US), and Groupe FH Ortho (France),among others are some of the major players operating in the global foot and ankle devices market.  The Research Report on “Pen Needles Market by Type (Standard Pen Needles, Safety Pen Needles), Length (4mm, 5mm, 6mm, 8mm, 10mm, 12mm), Therapy (Insulin, GLP 1, Growth Hormone), and Mode of Purchase (Retail, Non-Retail) – Global Forecast to 2026″ published by MarketsandMarkets™, the market witnessed healthy growth during the last decade and is expected to reach USD 2.2 Billion by 2026 from an estimated USD 1.3 billion in 2021, at a CAGR of 11.2%. The Growth in the market is largely driven by the growing prevalence of chronic diseases and the favorable reimbursement scenario in selected countries. On the other hand, the preference for alternative modes of drug delivery, poor reimbursement in developing countries, and needle anxiety are expected to restrain the overall market growth. Misuse of insulin pens and reuse of pen needles are the challenges faced by the market. The growing preference for biosimilar drugs and emerging markets are areas of opportunity in the market. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=75948613 The Type 2 diabetes, hypertension, and CVD significantly increase the risk for hospitalization and death in COVID-19 patients. Hence, managing these comorbidities has gained more focus for patients with existing conditions and those at the highest risk of contracting these conditions. This awareness has increased among healthcare professionals and patients and supported the growth of the management devices market. Hypoglycemia and hyperglycemia are both predictors for adverse outcomes in hospitalized patients. Hence the adoption of insulin delivery devices has increased. Pen needles are used in great quantities in diabetes management. So these would naturally be impacted by any change in overall product and service demand. The safety pen needles segment holds the highest CAGR during the forecast period. Based on type, the pen needles market is segmented into standard and safety pen needles. Safety pen needles are seen to be growing at the highest CAGR. Due to the rising awareness regarding the risks associated with blood-borne pathogen transmission, needle safety has become an issue of concern for hospitals, doctors, and patients, thus spurring the demand for safe needles. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=75948613 Geographically, the pen needles market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific accounted for the highest growth of the pen needles market in 2020. The medical industry in the region has grown significantly over the years, and manufacturers are beginning to focus on providing well-established technologies to ensure sustainable and strong future revenue growth. Being a high-growth market, many manufacturers are also extending their global manufacturing bases to the APAC. With the low-cost manufacturing advantage, China and India are regarded as the most profitable manufacturing and R&D locations by most manufacturers. Prominent players in the pen needles market include Becton, Dickinson and Company (US), Novo Nordisk A/S (Denmark), Ypsomed Holding AG (Switzerland), B. Braun Melsungen AG (Germany), Owen Mumford (UK), Terumo Corporation (Japan), Nipro Corporation (Japan) Allison Medical (US), AdvaCare Pharma (US), Berpu Medical Technology (China), ARKRAY (Japan), GlucoRx (UK), HTL-STREFA (Poland), UltiMed, (US), Hindustan Syringes and Medical Devices (India), Artsana Group (Italy), PromiseMed Diabetes Care (Canada), Montmed (Canada), Trividia Health (US), VOGT Medical Vertrieb (Germany), Van Heek Medical (Netherlands), Simple Diagnostics (US), Iyon (Turkey), Links Medical Products (US), and MHC Medical Products (US).  The report “Viral Clearance Market by Application (Recombinant Proteins, Blood, Vaccines), End User (Pharmaceutical & Biotechnology Companies, CROs), Method (Viral Removal (Chromatography, Nanofiltration), Viral Inactivation (Low pH)) – Global Forecast”, the global viral removal market is expected to reach USD 724.5 million, at a CAGR of 21.7% during the forecast period. The key factors driving the growth of this market include growth in the pharmaceutical and biotechnology industries, increasing number of new drug launches, R&D investments in life science, advancements in nanofiltration technology, and the high incidence and large economic burden of chronic diseases. Research Methodology Adopted; Top-down and bottom-up approaches were used to validate the size of the global viral clearance market and estimate the size of other dependent submarkets. Various secondary sources such as the International Society for Pharmaceutical Engineering, International Federation of Pharmaceutical Manufacturers and Associations (IFPMA), International Pharmaceutical Federation (FIP), International Diabetes Federation (IDF), European Federation of Biotechnology, International Rare Diseases Research Consortium (IRDiRC), Canadian Institutes of Health Research, Association of the British Pharmaceutical Industry (ABPI), Indian Drug Manufacturers Association, Chinese Medical Association, Korean Research- based Pharma Industry Association (KRPIA), directories, industry journals, databases, press releases, and annual reports of the companies have been used to identify and collect information useful for the study of this market. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=62681197 The recombinant proteins segment is expected to account for the largest share of the market On the basis of application, the global market is segmented into four categories recombinant proteins, blood and blood products, vaccines, and other applications. In 2018, the recombinant proteins segment is expected to account for the largest share of the viral clearance market owing to the high potential of recombinant proteins to treat various diseases, fewer side effects, and shorter development time as compared to small molecules. Furthermore, the regulatory requirement to demonstrate the capacity of the purification process to effectively clear infectious viruses during the manufacturing of recombinant proteins is also expected to support the growth of this market segment during the forecast period. The viral removal segment is expected to account for the largest share of the market On the basis of method, the viral clearance market is segmented into viral removal and viral inactivation. In 2018, the viral removal segment is expected to account for the largest share of the global market due to the growth in biopharmaceutical R&D activities; the high acceptance of this method; and the accuracy, speed, and flexibility provided by the method in life sciences research. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=62681197 Geographical View in-detailed: The North American region is expected to account for the largest share of the market. The viral clearance market in the region is driven by the presence of national institutes supporting biotechnology and life science research, growth in the pharmaceuticals industry, and the increasing number of drug approvals. However, Asia Pacific is expected to witness the highest growth during the forecast period, owing to increase in generics development and manufacturing, surge in funding for medical research and the presence of a large number of CROs to provide preclinical and clinical research services in China, government initiatives to boost the use of generic drugs, increasing aging population in Japan, rise in pharmaceutical R&D expenditures in India, and the growing pharmaceutical manufacturing in Singapore and Malaysia. Global Key Leaders: The key players in the global viral clearance market are Wuxi Biologics (Cayman) (China), Merck KGaA (Germany), Charles River Laboratories International Inc. (US), and Texcell Inc. (France), Kedrion (Italy), Vironova Biosafety (Sweden), Clean Cells (France), BSL BIOSERVICE Scientific Laboratories Munich GmbH (Germany), and ViruSure GmbH (Austria).  The report “Cell Harvesting Market by Type (Manual, Automated), Application (Biopharmaceutical, Stem Cell Research), End User (Biotechnology, Biopharmaceutical Companies, Research Institute), and Region (North America, Europe, APAC, Row) – Global Forecast”, the cell harvesters market is expected to reach USD 324.5 Million, at a CAGR of 8.7%

The Cell harvesting is the process of harvesting cells from the culture media during upstream and downstream bio-processing. Cell harvesters are used extensively for the cell harvesting process and are compatible with a wide range of assays. Rising investments in regenerative medicine and cell-based research, growth of the bio-pharmaceutical and biotechnology industry, and increasing incidence of chronic and infectious diseases are the major driving factors for this market. The objectives of this study are as follows:

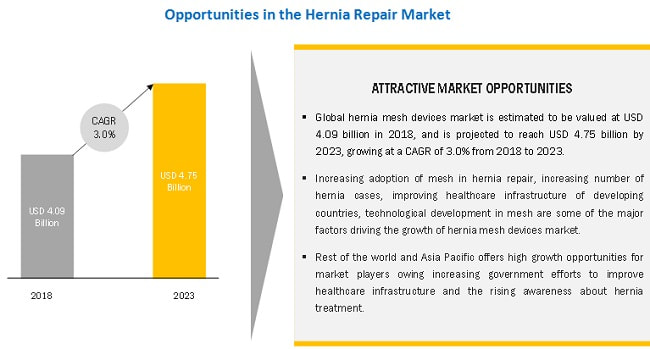

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=209513544 The biotechnology & biopharmaceutical companies segment dominated the market. In the end user, the cell harvesting market is segmented into research institutes, biotechnology & biopharmaceutical companies, and other end users. In 2017, the biotechnology & biopharmaceutical companies segment accounted for the largest share of the cell harvesters market. The high share of this segment can be attributed to the high prevalence of chronic diseases. Biotechnology & biopharmaceutical companies conduct R&D activities to develop new products for the treatment of these diseases. The manual cell harvesters segment dominated the cell harvesting market. On the basis of type, the market is segmented into manual and automated cell harvesters. In 2017, the manual cell harvesters segment accounted for the largest share of this market. The high share of the manual harvesters segment can be attributed to their ease of use and low price as compared to automated harvesters. Asia Pacific offers lucrative growth opportunities By region, the global cell harvesting market is segmented into North America, Europe, Asia Pacific, and the Rest of the World (RoW). While North America held the largest share of the market in 2017, Asia Pacific is expected to register the highest CAGR during the forecast period. As increasing R&D expenditure helps in the development of new treatment solutions, supportive government policies for stem cell research and increasing public-private initiatives to encourage public adoption of stem cell-based treatment in the Asia Pacific countries are driving the growth of the market in this region. Cell harvesting products are widely used in upstream and downstream bioprocesses. They are also used to for the research and development of stem cell therapy products. As increasing R&D expenditure helps in the development of new treatment solutions, supportive government policies for stem cell research and increasing public-private initiatives to encourage public adoption of stem cell-based treatment in the Asia Pacific countries are driving the growth of the market in this region. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=209513544 Some of the major players operating in the cell harvesting market are PerkinElmer (US), Brandel (US), TOMTEC (US), Cox Scientific (UK), Connectorate (Switzerland), Scinomix (US), ADSTEC (Japan), and Terumo BCT (a part of Terumo Corporation) (Japan).  The increasing number of hernia repair procedures, advantages of mesh in hernia repair, and technological advancements are the major factors driving the hernia repair market. In addition, emerging markets are expected to emerge as potential areas of opportunity for players in this market. However, the high cost of meshes, long waiting times, and the development of non-mesh repair approaches are restraining the growth of this market. In addition, increasing pricing pressure on market players and the need for skilled personnel to conduct laparoscopic surgery are the key challenges faced in this industry. Expected Revenue Surge: The Hernia Repair Market is projected to reach USD 4.75 billion by 2023 from USD 4.09 billion in 2018, at a CAGR of 3.0% during the forecast period Growth Driver: Increasing hernia prevalence; The growing prevalence of hernia is the main driving force for the growth of the hernia mesh repair market. This is mainly attributed to the overall increase in population, specifically geriatric and obese population, and improvements in healthcare systems that have enabled the early detection and treatment of hernia. Age contributes significantly to the risk of hernia by retarding the body’s capabilities and natural healing abilities over time. According to a registered study in the UK, the prevalence of hernia was found to increase with age, from 5% in the 25¡V34 age group to:

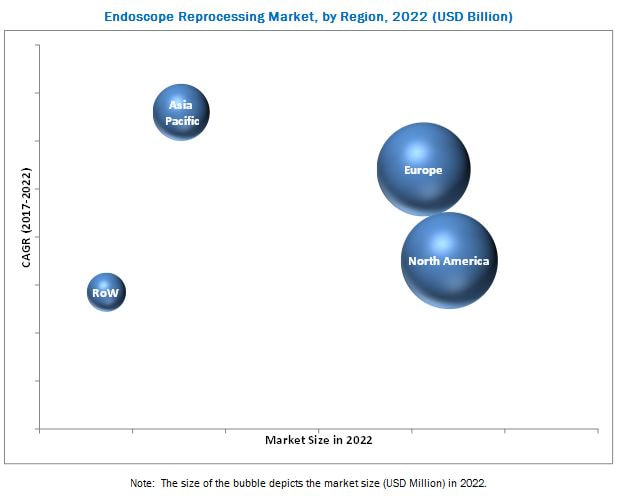

In addition, the incidence of hernia among men aged 75 years and above was found to be 45%. Consequently, the growth in aging population can be expected to boost overall hernia incidence in the coming years. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=203245450 Market Segmentation in Detailed: By Product; The hernia repair market is segmented into mesh and mesh fixators. A mesh is used for reinforcing weak spots in the muscle while repairing the hernia. Mesh fixators are used to fix the mesh in its place to avoid displacement. In 2018, the hernia mesh fixators segment is expected to grow at the highest CAGR during the forecast period. This significant growth of the segment is attributed to the rising adoption of surgical glue as mesh fixators. The hernia mesh segment is further categorized on the basis of type and surgery. On the basis of type, this market is segmented into synthetic and biologic mesh. In 2018, the biologic mesh segment is expected to register the highest growth rate in the hernia mesh market. The increasing number of clinical trials to establish safety and the benefits of biologic meshes coupled with technological advancements to reduce ‘could be’ issues with these mesh are some of the factors triggering the growth of this segment. Based on Surgery; The hernia mesh market is segmented into inguinal hernia, incisional/ventral hernia, femoral hernia, and umbilical hernia. Of these, the inguinal hernia segment is expected to account for the largest market share in 2018. The large share of this segment is attributed to the high number of inguinal hernia repair surgeries performed worldwide every year. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=203245450 Geographically; Segmented into four major regions, namely, North America, Europe, the Asia Pacific, and the Rest of the World (RoW). In 2018, North America is estimated to account for the largest market for hernia mesh devices. The large share of North America in this market can be attributed to the strong demand for and adoption of hernia repair in the US, presence of a large pool of hernia patients, and an efficient and favorable healthcare system are supporting the growth of the hernia mesh market in North America. The major players in the hernia repair market profiled in this report are Covidien ( Part of Medtronic) (Ireland), Ethicon (Part of Johnson & Johnson) (US), B. Braun (Germany), C.R. Bard (Part of Becton Dickinson) (US), W. L. Gore (US), LifeCell (Part of Allergan) (Ireland), Maquet (Part of Getinge) (Sweden), Cook Medical (US), Integra (US), DIPROMED (Italy), FEG (Germany), Cousin Biotech (France), Herniamesh (Italy), Aspide Medical (France), TransEasy Medical (China), and Via Surgical (Israel).  The Factors such as high risk of infections associated with improper sterilization of endoscopes, increasing investments, funds, and grants by government bodies across the globe, rising number of hospitals and growing hospital investments in endoscopy instruments, and rising prevalence of diseases that require endoscopy procedures are driving the growth of the global market for endoscope reprocessing during the forecast period. Expected Revenue Surge: The Global Endoscope Reprocessing Market is expected to reach $2.15 Billion, at a CAGR of 8.6% Objectives of the Study:

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=219094994 Market Segmentation in Detailed: Basis on Products; The market is segmented into high-level disinfectants and test strips; detergents and wipes; endoscope tracking systems; endoscope drying, storage, and transport systems; automated endoscope reprocessors (AERs); and other products (brushes and flushing aids, leak testers, hookups, and sponges). The high-level disinfectants and test strips segment is expected to account for the largest share of the global endoscope reprocessing market in 2017. The large share of this segment is attributed to the increasing outbreaks linked to inadequate cleaning or disinfecting during HLD, the effectiveness of high-level disinfectants for quality assurance in decontaminating endoscopes, and rising adherence to endoscope reprocessing guidelines by healthcare centers. Basis of End-User; Segmented into hospitals, ambulatory surgery centers, and other end users (diagnostic centers, mobile endoscopy facilities, and office endoscopy centers). In 2017, the hospitals segment is expected to account for the largest share of the global endoscope reprocessing market. The ambulatory surgery centers (ASCs) segment, on the other hand, is expected to be the fastest-growing segment during the forecast period. The high growth in this segment can be attributed to the increase in the number of endoscopic procedures performed in ASCs, and rising preference of ASCs over hospitals. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=219094994 Geographically; North America accounted for the largest share of the endoscope reprocessing market, followed by Europe. In the US, Driven by the favorable reimbursement scenario, rising incidence of cancer, increasing investments by hospitals to purchase new endoscopic equipment, and increasing incidence of endoscope-related infections. In Canada, the growth of the market is driven by the availability of physician bonuses, and implementation of a new funding model for Canadian hospitals. The various players in the endoscope reprocessing market include Advanced Sterilization Products (ASP) (US), Cantel Medical (US), Laboratories Anios (France), Olympus (Japan), Wassenburg Medical (The Netherlands), Custom Ultrasonics (US), STERIS (US), Steelco (Italy), Getinge (Sweden), ENDO-TECHNIK (Germany), BES Decon (UK), ARC Healthcare Solutions (Canada), and Metrex Research (US) among others. |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed