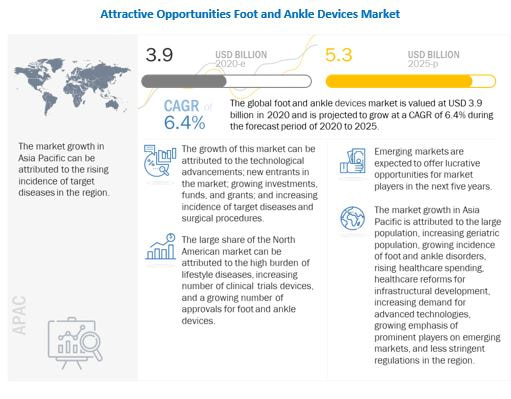

The Key Growth Elements in Detailed? The Growth of Foot and Ankle Devices Market is mainly driven by the growing number of hospitals across major markets, increasing awareness about complication related to foot and ankle related to osteoarthritis and diabetes coupled with the increasing adoption of bracing and support devices devices. Moreover, rising R&D investments by the key players operating in the market to develop advanced foot and ankle devices coupled with growing funding & grants for commercialization and development of foot and ankle devices are other important factors to drive the market growth in the near future. Worldwide Growth Opportunities in Terms of Revenue: The Foot and Ankle Devices Market is projected to reach USD 5.3 billion by 2025 from USD 3.9 billion in 2020, at a CAGR of 6.4% during the forecast period. Growth Driver: Continuous product commercialization; Foot and ankle devices offer several benefits such as better affordability, higher efficacy, greater patient comfort, and are easy-to-use as compared to conventional products. Moreover, key players are increasingly focusing on the development of specialized products for the treatment of various foot and ankle disorders and deformaties as well as to address the unmet market needs. The availability of advanced products and treatment modalities is generating significant interest among end users owing to the better treatment outcomes promised by them. Listed below are regulatory approval and launches in recent years:

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=845 Regional Growth, Development and Demand Analysis: The North America, comprising the US and Canada, accounted for the largest share of the foot and ankle devices market in 2019. Increasing number of clinical trials validating foot and ankle devices and a growing number of approvals forfoot and ankle devices are the major factors driving market growth in North America. Customers in North America are moving towards ambulator surgical centers, which is increasing de,mand for foot and ankle devices. This trend will have a positive impact on the foot and ankle devices market. Major Key Players Mentioned in the research report are: DePuy Synthes Companies (US), Stryker Corporation (US), Zimmer Biomet Holdings, Inc (US), Smith & Nephew plc (UK), Arthrex Inc (US), Integra LifeSciences Holdings Corporation (US), DJO Finance, LLC (US), CONMED Corporation (US), Össur HF (Iceland), Orthofix Medical Inc. (US), Medartis AG (Switzerland), Acumed LLC (US), Extremity Medical (US), aap Implantate AG (Germany), Ottobock SE & Co. KGaA (Germany), Ortho Solutions UK Ltd. (UK), Vilex in Tennessee, Inc. (US), Advanced Orthopaedic Solutions (US), Fillauer LLC (US), and Groupe FH Ortho (France),among others are some of the major players operating in the global foot devices market. DePuy Synthes Companies (US) has a wide range of product offerings in the foot and ankle devices market, including internal fixation devices, external fixation devices, joint implants and musculoskeletal reinforcement d evices products. The company sustains its key position in the global ankle devices market owing to its multiple product launches. DePuy Synthes has a strong product portfolio, supporting around one million orthopedic and neuro procedures worldwide.The company is focused on innovations and improving the quality of its products with increasing investment in its R&D department. DePuy Synthes global footprint allows it to cater to a customer base across 60+ countries such as Germany, the UK, South Korea, France, Australia, and the US. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=845

0 Comments

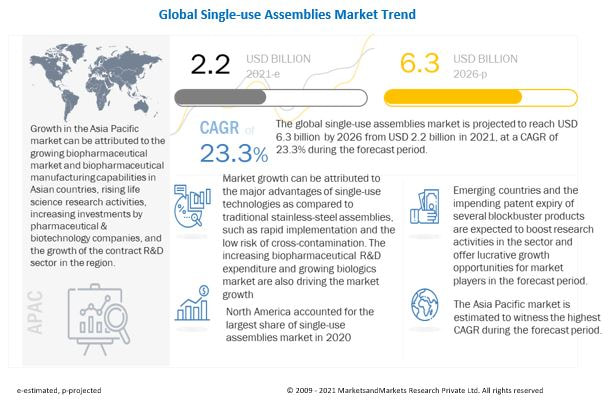

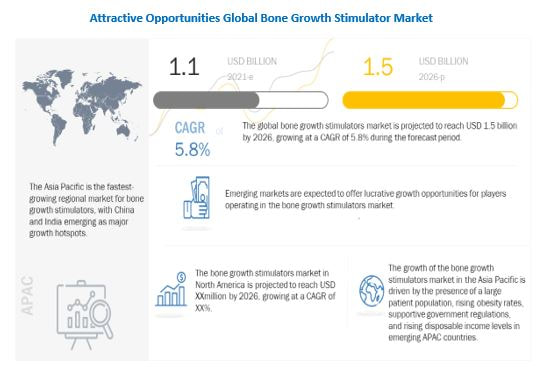

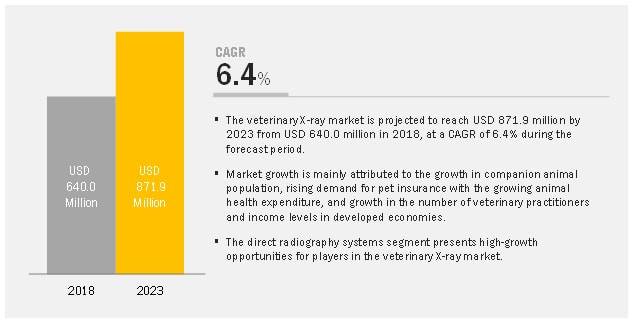

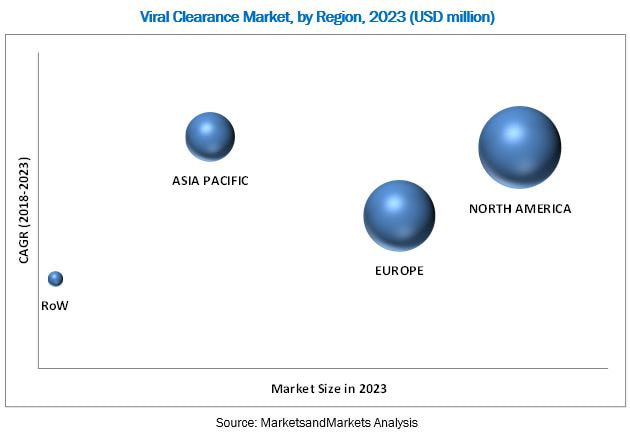

The Key Growth Elements in Detailed? The Growth of single-use assemblies market can primarily be attributed to the major advantages of single-use technologies as compared to traditional stainless-steel assemblies, such as rapid implementation and the low risk of cross-contamination. The increasing biopharmaceutical R&D expenditure and growing biologics market are also driving the growth. Worldwide Growth Opportunities in Terms of Revenue: The Global Single-use Assemblies Market is projected to reach USD 6.3 billion by 2026 from USD 2.2 billion in 2021, at a CAGR of 23.3% during the forecast period. Growth Driver: Rapid implementation and low risk of cross-contamination; A single-use solution has numerous advantages over traditional bioprocessing technologies, due to which the adoption of single-use assemblies is growing continuously. These include the faster implementation of single-use assembly components in the bioprocess cycle and a lower risk of cross-contamination. Single-use assemblies are ergonomically designed to hold integrated single-use flow paths for faster set-up and reduced space requirements. The product design is aimed to reduce the amount of time and cost related to preparation, set-up, testing, validation, and documentation. Product cross-contamination is a major concern in the biomanufacturing industry. The potential for cross-contamination occurs when the same process equipment is used repeatedly in the process cycle. Unwanted protein contamination, for example, may reduce production yields by requiring additional purification steps, or in the worst possible case, proteins that co-purify may result in potentially fatal treatments. Single-use component manufacturers also typically make and assemble products in clean rooms to ensure that their products do not introduce harmful particulates and endotoxins into a bioprocess. Such advantages are driving the adoption of single-use assemblies among end users in the bio-pharmaceutical & pharmaceutical industries. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=46226549 Regional Growth, Development and Demand Analysis: In 2020, the Asia Pacific region accounted for the fasted growing region of the single-use assemblies market. This can be attributed to the growing biopharmaceutical market and biopharmaceutical manufacturing capabilities in Asian countries, rising life science research activities, increasing investments by pharmaceutical & biotechnology companies, and the growth of the contract R&D sector. Major Key Players Mentioned in the research report are: Prominent players operating in the single-use assemblies market are Thermo Fisher Scientific, Inc. (US), Sartorius Stedim Biotech (France), Danaher Corporation (US), Merck KGaA (Germany), Avantor, Inc. (US), and Saint-Gobain (France). Thermo Fisher Scientific is one of the leading players in the single-use assemblies market. The company offers a range of single-use assemblies for downstream, upstream, and fill-finish stages of bioprocessing. The company’s BioProcess containers and transfer assemblies are single-use flexible container systems for critical liquid handling applications in biopharmaceutical & biomanufacturing operations. In the last few years, the company has majorly focused on expanding its bioproduction capabilities and market presence. In 2020, it saw significant growth in its Life Sciences segment, driven by the demand for diagnostic testing for COVID-19; the demand for bioproduction products, including single-use assemblies, saw a significant surge. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=4622654  According to the new market research report “Bone Growth Stimulator Market by Product (Device (Implant, External), Bone Morphogenetic Protein, PRP), Application (Spinal Fusion, Delayed Union, Non-union Bone Fracture, Maxillofacial Surgery), Care Setting (Hospital, Homecare) – Global Forecasts to 2026″, published by MarketsandMarkets™, the global BGS Market is projected to reach USD 1.5 billion by 2026 from USD 1.1 billion in 2021, at a CAGR of 5.8% during the forecast period. Opportunity: Emerging markets; Emerging economies (such as China, India, Brazil, and Mexico) are expected to offer significant growth opportunities in the bone growth stimulators market. Factors such as the presence of a large patient population, rising healthcare expenditure, government initiatives to support the healthcare industry, strengthening export trade, and growing awareness among physicians, surgeons, and patients about the latest treatment options for spinal fusion and bone healing are expected to boost the demand for bone growth stimulation products in these countries. In addition, owing to the significant cost advantages, many patients from developed markets are reported to travel to these emerging markets to undergo medical treatment. Emerging economies (such as China, India, Brazil, and Mexico) are expected to offer significant growth opportunities in the bone growth stimulators market. Factors such as the presence of a large patient population, rising healthcare expenditure, government initiatives to support the healthcare industry, strengthening export trade, and growing awareness among physicians, surgeons, and patients about the latest treatment options for spinal fusion and bone healing are expected to boost the demand for bone growth stimulation products in these countries. In addition, owing to the significant cost advantages, many patients from developed markets are reported to travel to these emerging markets to undergo medical treatment. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=82341383 The Rise in the global incidence of AKI and increase in the demand for effective renal replacement therapy among ICU patients and initiatives undertaken by governments to increase the awareness about BGS therapy along with the increase in the launch of advanced BGS system area anticipated to fuel the BGS market growth during the forecast period. The growing demand for orthopedic injuries to support the market growth during the forecast period. The significant rise in demand for BGS in the treatment of orthopedic patients. Moreover, the development and commercialization of BGS products also support Bone Growth Stimulator Market growth. Furthermore, many companies are expanding their BGS (PRP products) product portfolios. Similarly, the companies are also expanding their presence in the market. For instance, in 2021, Orthofix entered into an exclusive license agreement to commercialize the innovative portfolio of IGEA’s bone, cartilage, and soft tissue stimulation products in the US and Canada. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=82341383 Asia Pacific likely to emerge as the fastest-growing BGS Market. Geographically, the emerging Asian countries, such as China, India, Japan and Singapore, are offering high-growth opportunities for Bone Growth Stimulator Market players. The Asia Pacific point of care market is projected to grow at the highest CAGR of 8.7% from 2021 to 2026. Expansion of healthcare infrastructure and increase in disposable personal income, increase patient population with orthopedic disease, are factors likely to support the growth of market in the region. The prominent players operating in the global Bone Growth Stimulator Market include Orthofix Medical, Inc. (US), DJO Finance, LLC (US), Zimmer Biomet (US), Bioventus LLC (US), Medtronic plc (Ireland), Stryker (US), DePuy Synthes (US), Arthrex, Inc. (US), Isto Biologics (US), Terumo Corporation (Japan), Ember Therapeutics, Inc. (US), Ossatec Benelux Ltd. (Netherlands), Altis Biologics (Pty) Ltd. (South Africa), Regen Lab SA (Switzerland), ITO Co., Ltd. (Japan), Elizur Corporation (US), BTT Health GmbH (Germany), Stimulate Health Inc. (Canada), VQ OrthoCare (US)  The study involved four major activities to estimate the current market size for veterinary X-ray products. Exhaustive secondary research was done to collect information on the market, peer market, and parent market. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. Secondary Research: In the secondary research process, various secondary sources such as annual reports, press releases & investor presentations of companies, white papers, certified publications, articles by recognized authors, trade directories, and databases such as D&B Hoovers and Bloomberg Businessweek were referred to identify and collect information for this study. According to the new market research report “Veterinary X-ray Market by Technology (Direct, Computed, Film), Type (Digital, Analog), Mobility (Fixed, Portable), Animal (Companion, Large Animal), Application (Trauma, Oncology, Dental), End User (Clinic, Hospital) – Forecast” published by MarketsandMarkets™, is projected to reach USD 872 million by 2023 from USD 640 million in 2018, at a CAGR of 6.4%. Recent Developments: – In 2018, Heska Corporation (US) formed a partnership with Pathway Vet Alliance (US). Under the terms of this agreement, Pathway plans to align its internal diagnostic portfolio with Heska, which can provide in-house operational services like point-of-care blood diagnostics, digital imaging, and allergy testing. – In 2018, Carestream Health signed a service partnership agreement with Med Imaging Healthcare, a Diagnostic Imaging equipment maintenance company. The partnership was aimed at providing wider maintenance coverage and support for Carestream customers across Scotland. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=126397675 Geographically; North America accounted for the largest share of the veterinary X-ray market in 2017, followed by Europe and the Asia Pacific. Rising number of veterinary practices, increasing number of companion animals, and rising companion animal healthcare expenditure are some of the key factors driving the growth of the animal x-ray market in North America. The prominent players in the veterinary X-ray market are IDEXX (US), Fujifilm (Japan), Onex Corporation (Canada), Sedecal (Spain), Agfa-Gevaert (Belgium), Sound Technologies (US), Fujifilm Holdings Corporation (Japan), Canon, Inc (Japan), Examion (Germany), Konica Minolta (US), DRE Veterinary (US), and Heska Corporation (US). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=126397675 Market Segmentation in Detailed: “Computed Radiography Systems Accounted for the Largest Market Share” On the basis of technology, the veterinary X-ray market is segmented into direct radiography (DR), computed radiography (CR), and film-based radiography systems. The computed radiography systems segment accounted for the largest share of the animal X-ray market in 2017. Benefits offered by CR systems over traditional X-ray systems, resulting in a large-scale replacement of traditional film X-ray systems, is the major factor responsible for the large share of this segment. “Small Companion Animals Segment Held the Largest Share of the Veterinary X-ray Market” Based on the type of animal, the X-ray market is segmented into small companion animals and large animals. The small companion animals segment accounted for the largest share of the animal X-ray market in 2017. The large share of this segment can be attributed to the growing companion animal population, increasing pet care expenditure, growing demand for pet insurance, and technological advancements in imaging modalities for small companion animals.  The growth of Viral Clearance Market is primarily driven by factors such as the growth in the pharmaceutical and biotechnology industries, increasing number of new drug launches, R&D investments in life science, advancements in nano-filtration technology, and high incidence and large economic burden of chronic diseases. According to the new market research report “Viral Clearance Market by Application (Recombinant Proteins, Blood, Vaccines), End User (Pharmaceutical & Biotechnology Companies, CROs), Method (Viral Removal (Chromatography, Nanofiltration), Viral Inactivation (Low pH)) – Global Forecast” published by MarketsandMarkets™, is expected to reach USD 724.5 million, at a CAGR of 21.7% during the forecast period. Objectives of the Study;

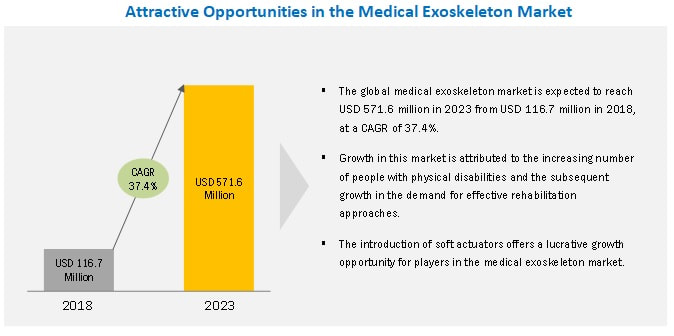

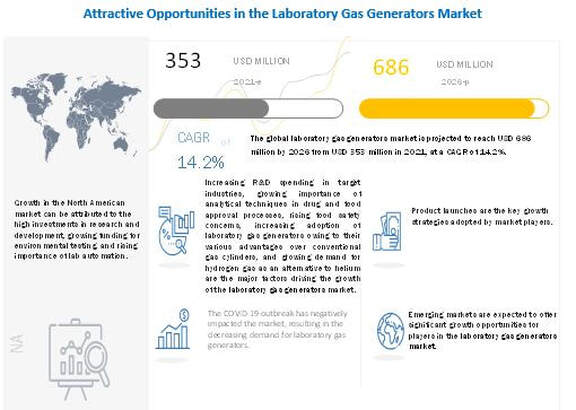

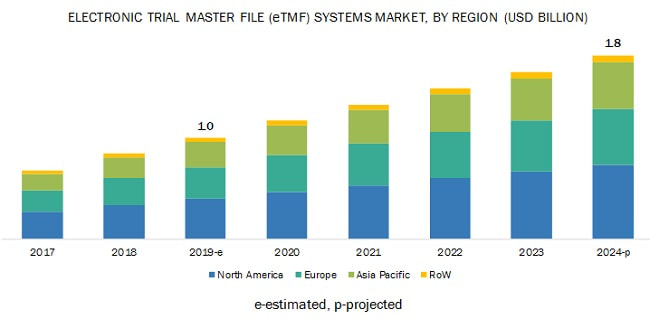

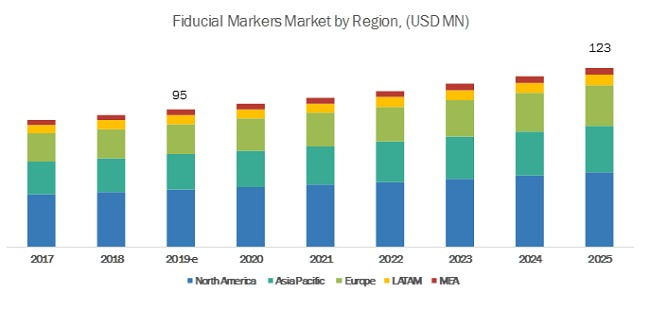

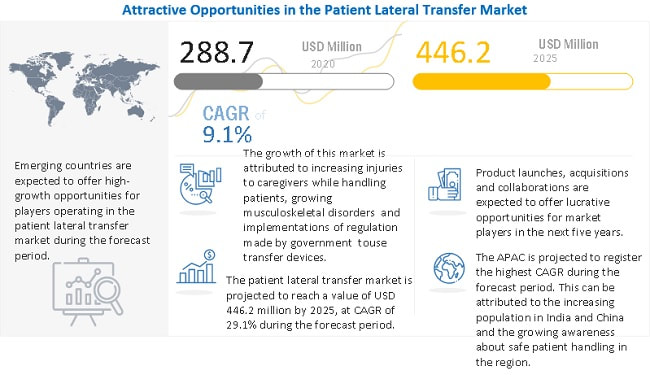

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=62681197 Geographically; The North American region is expected to account for the largest share of the market in 2018. The viral clearance market in the region is driven by the presence of national institutes supporting biotechnology and life science research, growth in the pharmaceuticals industry, and the increasing number of drug approvals. The rising prevalence of diseases, growing production of monoclonal antibodies, and government support for the development of drugs are some of the key factors driving the viral clearance market in the US. In Canada, increasing pharmaceutical production is expected to boost the growth of market. However, Asia Pacific is expected to witness the highest growth during the forecast period, owing to increase in generics development and manufacturing, surge in funding for medical research and the presence of a large number of CROs to provide preclinical and clinical research services in China, government initiatives to boost the use of generic drugs, increasing aging population in Japan, rise in pharmaceutical R&D expenditures in India, and the growing pharmaceutical manufacturing in Singapore and Malaysia. The key players in the global viral clearance market are Wuxi Biologics (Cayman) (China), Merck KGaA (Germany), Charles River Laboratories International Inc. (US), and Texcell Inc. (France), Kedrion (Italy), Vironova Biosafety (Sweden), Clean Cells (France), BSL BIOSERVICE Scientific Laboratories Munich GmbH (Germany), and ViruSure GmbH (Austria). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=62681197 Market Segmentation in Detailed: The recombinant proteins segment is expected to account for the largest share of the market in 2018 On the basis of application, the global market is segmented into four categories recombinant proteins, blood and blood products, vaccines, and other applications. In 2018, the recombinant proteins segment is expected to account for the largest share of the viral clearance market owing to the high potential of recombinant proteins to treat various diseases, fewer side effects, and shorter development time as compared to small molecules. Furthermore, the regulatory requirement to demonstrate the capacity of the purification process to effectively clear infectious viruses during the manufacturing of recombinant proteins is also expected to support the growth of this market segment during the forecast period. The pharmaceutical & biotechnology companies segment is expected to account for the largest share of the market in 2018 By end user, the viral clearance market is segmented into pharmaceutical & biotechnology companies, CROs, academic research institutes, and other end users. In 2018, the pharmaceutical & biotechnology companies segment is expected to account for the largest share of the global market. The large share of this segment can be attributed to the rapid expansion of the biopharmaceutical industry, growth in the number of research activities in life sciences, increasing R&D investments in drug development, and increasing number of drug launches.  A medical exoskeleton, also known as a wearable robot, is a robotic machine suite worn by humans in place of their limbs to complement, substitute, and enhance human functions. It helps in physical movements by offering increased strength and endurance. The Factors such as the increasing number of people with physical disabilities and subsequent growth in the demand for effective rehabilitation approaches; agreements and collaborations among companies and research organizations for the development of the exoskeleton technology; and increasing insurance coverage for medical exoskeletons in several countries driving the growth of the medical exoskeleton market. However, the high cost of medical exoskeletons may restrict market growth to a certain extent. According to the new market research report “Medical Exoskeleton Market by Component (Hardware (Sensor, Actuator, Control System, Power Source), Software), Type (Powered, Passive), Extremities (Lower, Upper) & Mobility (Mobile, Stationary) – Global Forecast” published by MarketsandMarkets™, is projected to reach USD 571.6 million, at a CAGR of 37.4% during the forecast period. Growth Opportunity: Introduction of soft actuators; Currently, the medical exoskeletons industry is focusing on developing soft exoskeletons (without electronic motors and heavy batteries), which augment normal muscle function in healthy individuals for commercial use. Currently, these exoskeletons are available only for research purposes. Such exoskeletons have soft actuators that can be easily driven by an off-board compressor. Soft exoskeletons are attached to the body securely and comfortably and transmit forces over the body through beneficial paths such that biologically appropriate moments are created at the joints. Compared to traditional exoskeletons, these exoskeletons are ultra-light-weight and have low mechanical impedance and inertia. The use of soft actuators has led to the development of inexpensive gait-supportive exoskeletons, creating opportunities for new players in the industry. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=138546702 Geographically; North America is expected to dominate the market followed by Europe. The large share of this geographical segment is attributed to the growing geriatric population, increasing demand for self-assist exoskeletons, growing number of spinal cord injuries (SCI), and the high prevalence of stroke in the region. The medical exoskeleton market includes various players. The major players in the market are Ekso Bionics Holdings, Inc. (US), ReWalk Robotics Ltd (Israel), Parker Hannifin Corp (US), Bionik Laboratories Corp (Canada), CYBERDYNE Inc. (Japan), Rex Bionics Ltd. (UK), B-TEMIA Inc. (Canada), Hocoma AG (A Subsidiary of DIH Technologies) (Switzerland), Wearable Robotics SRL (Italy), Gogoa Mobility Robots SL (Spain), and ExoAtlet, O.O.O. (Russia). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=138546702 Market Segmentation in Detailed: Lower extremity medical exoskeletons are expected to dominate the market in 2018 By extremity, the market is segmented into lower extremity medical exoskeletons and upper extremity medical exoskeletons. In 2018, lower extremity medical exoskeletons segment is expected to account for the largest share of the global medical exoskeleton market. Lower extremity exoskeletons provide stability to paralyzed and geriatric patients and offer weight-bearing and locomotion capabilities. As a result, they are more widely adopted for rehabilitation applications. The mobile segment is projected to grow at the highest CAGR during the forecast period Based on mobility, the medical exoskeleton market is segmented into mobile and stationary exoskeletons. The mobile segment is expected to register the highest CAGR during the forecast period. The growth of this segment can be attributed to the high demand for compact, light-weight mobile medical exoskeletons that can offer mobility assistance to paralyzed patients.  The growth of the Laboratory Gas Generators Market is primarily driven by the growing importance of analytical techniques in drug and food approval processes, rising food safety concerns, increasing adoption of laboratory gas generators owing to their various advantages over conventional gas cylinders, growing demand for hydrogen gas as an alternative to helium, and the increasing R&D spending in target industries. On the other hand, reluctance shown by lab users in terms of replacing conventional gas supply methods with modern laboratory gas generators and the availability of refurbished products are the major factors expected to hamper the growth of this market. According to the new market research report “Laboratory Gas Generators Market by type (Nitrogen, Hydrogen, Zero Air, Purge Gas, ToC), Application (Gas Chromatography, LC-MS), End user (Life Science Industry, Chemical & Petrochemical Industry, Food & Beverage Industry) – Global Forecast to 2026” published by MarketsandMarkets™, the global lab gas generators market is projected to reach USD 686 million by 2026 from USD 353 million in 2021, at a CAGR of 14.2% during the forecast period. GROWTH OPPORTUNITY: Opportunities in the life sciences industry; The demand for the analytical testing of cannabis for ensuring its safety before human consumption has increased in recent years, as medical cannabis is being legalized in a number of countries/states across the globe. Medical cannabis has proven effective in various medical applications, such as reducing nausea caused due to chemotherapy, stimulating appetite in AIDS patients, controlling muscular spasms in multiple sclerosis patients, and reducing intraocular pressure in patients with glaucoma. Owing to their health benefits, governments in various countries are legalizing the use of medical cannabis. Australia (2016), Canada (2015), South Korea (2018), Portugal (2001), the UK (2006), Germany (2017), Italy (2013), the Netherlands (2003), and Brazil (2017) have all legalized the use of medical cannabis in recent years. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=133302129 Geographically; The lab gas generators market is divided into five regions, namely, North America, Europe, Asia Pacific, and Rest of the World. North America dominated the global laboratory gas generators market. The large share of the North American region is mainly attributed to the high investments in R&D in the US and Canada, which has led to a higher demand for efficient and advanced laboratory equipment. The major players in the laboratory gas generators market are Parker Hannifin Corporation (US), PeakGas (UK), Linde plc (Ireland), Nel ASA (Norway), PerkinElmer Inc. (US), VICI DBS (US), Angstrom Advanced Inc. (US), Dürr Group (Germany), ErreDue spa (Italy), F-DGSi (France), LabTech S.r.l. (Italy), CLAIND S.r.l. (Italy). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=133302129 Market Segmentation in Detailed: Nitrogen gas generators accounted for the larger share of the share of global lab gas generators market in 2020 Based on type, segmented into nitrogen gas generators, hydrogen gas generators, zero air generators, purge gas generators, TOC gas generators, and other gas generators. The nitrogen gas generators segment accounted for the largest share of global laboratory gas generators market. This can be attributed to factors such as cost-efficiency, increased safety, reduced downtime and supply issues, environmental benefits, and its wide usage among end users. The liquid chromatography-mass spectrometry (LC-MS) segment accounted for the largest market share in 2020 Based on application, segmented into gas chromatography (GC), liquid chromatography-mass spectrometry (LC-MS), gas analyzers, and other applications. The liquid chromatography-mass spectrometry (LC-MS) accounted for the largest share of the global laboratory gas generators market. The large share of this segment can be attributed to the high efficiency and the expandable and scalable nitrogen generation capacity of generators in LC-MS applications.  The Growth in the eTMF systems market can be attributed primarily to the rising adoption of eTMF systems, rising number of clinical trials, partnerships between biopharma companies & CROs, increasing funding to support clinical trials, and the growth in the R&D spending by pharma & biotech companies. Emerging countries are expected to provide significant opportunities for players in the Electronic Trial Master File (eTMF) Systems Market. However, budget constraints, data privacy issues, and a dearth of skilled professionals will challenge market growth in the coming years According to the new market research report “Electronic Trial Master File Systems Market by Component (Services, Software), End-User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations), Delivery Mode (On-Premise, Cloud-Based), and Region – Global Forecast to 2024″ published by MarketsandMarkets™, the eTMF systems market is projected to reach USD 1.8 billion by 2024 from USD 1.0 billion in 2019, at a CAGR of 12.7%. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=94357456 Geographically; divided into North America, Europe, Asia Pacific, and the Rest of the World (RoW). The North American market accounted for the largest share of the eTMF systems market in 2018, primarily due to the increasing government funding for clinical research and a large number of clinical trials. Several major global players are also based in the US, owing to which the country has become a center of innovation in the Electronic Trial Master File Systems Market Veeva Systems (US), Oracle Corporation (US), Phlexglobal Limited (UK), TransPerfect Global Inc. (US), Aurea Software (US), LabCorp (US), ePharmaSolutions (US), Wingspan Technology, Inc. (US), MasterControl (US), SureClinical, Inc. (US), Dell EMC (US), Paragon Solutions (US), PharmaVigilant (US), Mayo Clinic (US), Database Integrations, Inc. (US), CareLex (US), Ennov (France), Forte Research (US), Freyr (US), Montrium (US), NCGS Inc. (US), SAFE-BioPharma (US), SterlingBio Inc. (US), BIOVIA Corp. (US), and arivis AG (Germany) are the key players in the eTMF systems market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=94357456 Market Segmentation in Detailed: the cloud-based eTMF segment accounted for the largest share of the eTMF systems market in 2018. Based on delivery mode, the market is segmented into on-premise and cloud-based eTMF. In 2018, the cloud-based eTMF segment accounted for the largest share of the market. The large share of this segment is primarily due to the flexible, scalable, and affordable nature of this delivery mode. The heavy dependence of end-users on service providers will drive the services segment in the eTMF systems market Based on the component, the market is segmented into services and software. The services segment accounted for the largest market share in 2018. The large share of this segment can be attributed to their indispensable nature and repetitive requirement. End-users of eTMF systems rely heavily on service providers for consulting, data storage, implementing services, training, maintenance, and regular upgrades of solutions.  The growth of Fiducial Markers Market is mainly attributed to factors such as the growing incidence of cancer, rising awareness on radiotherapy, and funding for cancer as well as fiducial marker research. In addition, the modernization of healthcare infrastructure and rising penetration of healthcare insurance in developing countries is expected to further fuel the growth of the market in the near future. According to the new market research report “Fiducial Markers Market by Product (Metal Based Markers (Gold, Gold Combination) Polymer Markers), Cancer Type (Prostate, Lung, Breast), Modality (CT, CBCT, MRI, Ultrasound), End user (Hospitals, Outpatient Facilities) – Global Forecast to 2025” published by MarketsandMarkets™, is projected to USD 123 million by 2025 from USD 95 million in 2019, at a CAGR of 4.5% during the forecast period of 2019 to 2025. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=180673710 Geographically; the fiducial markers market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa. North America is projected to hold the largest share of the regional market for fiducial markers in 2019. This is attributed to the expansion of the target patient population, favorable reimbursement scenario, greater accessibility to radiotherapy procedures, and the presence of major players in this region. The major players in Fiducial Markers Market include CIVCO Radiotherapy (US), IZI Medical Products (US), Boston Scientific Corporation (US), Naslund Medical AB (Sweden), and IBA (Belgium). Other players are Best Medical International, Inc. (US), Nanovi A/S (Denmark), Carbon Medical Technologies (US), Eckert & Ziegler (Germany), Innovative Oncology Solutions (US), Medtronic (Ireland), and QFIX (US). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=180673710 Market Segmentation in Detailed: The metal-based FMs product segment to register significant growth over the forecast period Based on product, the fiducial markers market is classified into metal-based markers, polymer-based markers, and others. The metal-based markers segment is expected to register significant growth over the forecast period of 2019 to 2025. The adoption of radiotherapy has increased in recent years due to its advantages, such as high precision & radiation control, reduced risk of side-effects, and minimal exposure of healthy tissues to radiation. As metal-based FMs are widely preferred for tumor localization, the rising adoption of radiotherapy procedures is expected to support market growth. Prostate cancer segment to grow at the highest CAGR over the forecast period Based on cancer type, the fiducial markers market is broadly segmented into prostate cancer, lung cancer, breast cancer, gastric cancer, and others. Among these, the prostate cancer segment is anticipated to register significant growth over the forecast period due to the rising incidences of prostate cancer globally and the high cure rate associated with radiotherapy. For instance, according to a study published in the Journal of Medical Imaging and Radiation Oncology, the use of EBRT in men suffering from prostate cancer showed a cure rate of ~95.5% for intermediate-risk prostate cancer.  The outbreak of corona virus globally, there is a sudden rise in the demand for patient lateral transfer services. The Growth in this market will majorly be driven by the high risk of musculoskeletal injuries to caregivers during manual handling of patients and the implementation of regulations to minimize manual patient handling. However, the lack of training to caregivers for the efficient operation of patient handling equipment is a key challenge in this market. According to the new market research report “Patient Lateral Transfer Market by Product (Air Assisted Transfer Device (Type (Regular Mattress, Split Legs Mattress, Half Mattress), Usage (Single Patient Use, Reusable)), Sliding Sheets, Accessories) End User (Hospitals) – Global Forecast to 2025” published by MarketsandMarkets™, is expected to reach USD 446.2 million by 2025 from USD 288.7 million in 2020, at a CAGR of 9.1% during the forecast period of 2020 to 2025. Growth Opportunities: Growing demand of home health care services; Globally, an increasing number of government regulations are being implemented for reducing the duration and cost involved in healthcare treatments. For instance, the Centers for Medicare and Medicaid Services (CMS) has implemented steps to provide incentives to healthcare providers for reducing hospitalization costs. Under this initiative, the CMS is promoting healthcare settings such as nursing homes and approaches such as home healthcare as they can provide quality care at reduced costs (as compared to the cost of hospitalization). Homecare settings are expected to account for 28.3% of the patient handling equipment market in the US. Owing to this, private nursing institutions and geriatric care homes have become highly viable end-user segments in the US. market. This will eventually increase opportunity for home healthcare services in lateral transfer market Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=93948116 Geographically; the patient lateral transfer market is segmented into five major regions, namely, North America, Europe, Asia Pacific, Latina America, and the Middle East and Africa. In 2019, North America accounted for the largest share. The large share of North America can primarily be attributed to the growing number of COVID-19 cases, rising prevalence of musculoskeletal disorders among caregivers, growing geriatric population, and the increasing incidence of chronic and lifestyle diseases. Due to its growing geriatric population segment and environmental conditions have favored the spread of COVID-19 which has severely affected the region and ensured enormous growth in the demand for patient lateral transfer devices. Players in this and adjacent, or even non-related, markets have focused on or collaborated for expanding the products of patient lateral transfer. Some of the prominent players in patient lateral transfer market are Stryker Corporation (US), Hill-Rom Holdings, Inc. (US), Sizewise (US), Arjo (Sweden), Haines Medical Australia (Australia), Handicare (Sweden), Medline Industries, Inc. (US), AliMed (US), and Airpal Inc. (US). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=93948116 Market Segmentation in Detailed: Rise in the musculoskeletal injuries to caregivers while man handling patients to drive the demand for patient lateral transfer. Based on product, the patient lateral transfer market is segmented into air-assisted lateral transfer mattresses, sliding sheets, and accessories. The air-assisted lateral transfer mattresses segment accounted for the largest market share in 2019. The large share of this segment can be attributed to the advantages of these mattresses in overcoming persistent difficulties while handling patients with special conditions. The hospitals segment accounted for the largest market share in 2019 Based on end users, the patient lateral transfer market is segmented into hospitals, ambulatory surgery centers, and other end users. Hospitals accounted for the largest share of the lateral transfer market in 2019. This can be attributed to many patient admissions in hospitals, rising prevalence of various chronic conditions, and growing regulatory norms to use safe patient transfer equipment. Ambulatory surgery centres are expected to witness the highest growth during the forecast period, mainly due factors such as the growing number of digitalization in healthcare field such as mhealth and teleradiology. |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed