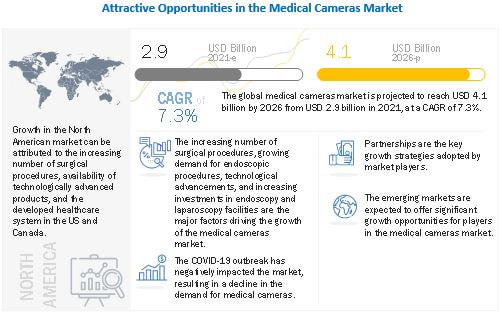

The Medical Camera Market growth is largely driven by the increasing number of surgical procedures, growing demand for endoscopic procedures, technological advancements, and increasing investments in endoscopy and laparoscopy facilities. However, the high cost of medical cameras is a major restraint for market growth. Product discontinuations, a shortage of trained medical professionals, and the availability of refurbished products are also major challenges limiting market growth to a certain extent. According to the new market research report “Medical Cameras Market by Camera Type (Endoscopy Cameras, Ophthalmology Cameras, Dermatology Cameras), Resolution (HD Cameras, SD Cameras), Sensor (CMOS, CCD), End-Users (Hospitals & Ambulatory Surgery Centers, Specialty Clinics) – Global Forecast to 2026” published by MarketsandMarkets™, is projected to reach USD 4.1 billion by 2026 from USD 2.9 billion in 2021, at a CAGR of 7.3% during the forecast period. GROWTH DRIVER: The increasing number of surgical procedures; An increasing number of surgical procedures require medical cameras, which has considerably grown in recent years. The growing number of surgeries can be attributed to the rapidly growing geriatric population worldwide and the increasing prevalence of chronic diseases, leading to the increasing demand for medical equipment. Many countries across the world are facing the challenge of increasing senior populations. According to the United Nations (UN), in 2019, there were 703 million persons aged 65 years or over in the world. The senior population is estimated to double to 1.5 billion in 2050. Non-invasive surgeries (mainly using endoscopy and microscopy surgery cameras) are preferred for older people due to lesser complications than conventional surgeries. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=201071746 Geographically; the medical cameras market is divided into five regions, namely, North America, Europe, Asia Pacific, and Rest of the World. North America dominated the global market. The large share of the North American region is mainly attributed to the technological advancements in medical cameras, implementation of favorable government initiatives, and rise in the number of surgical procedures. The major players in the medical camera market are Olympus Corporation (Japan), Richard WOLF GmbH (Germany), TOPCON CORPORATION (Japan), Sony Corporation (Japan), Stryker Corporation (US), Danaher Corporation (US), Canon Inc. (Japan), Carl Zeiss AG (Germany), Smith & Nephew (UK), Carestream Dental LLC (US), and Basler AG (Germany) Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=201071746 Market Segmentation in Detailed: Endoscopy Cameras accounted for the larger share of the share of global medical cameras market in 2020. Based on type, segmented into surgical microscopy cameras, endoscopy cameras, dermatology cameras, ophthalmology cameras, dental cameras, and other medical cameras. The Endoscopy cameras segment accounted for the largest share of global medical camera market. This can be attributed to the increasing number of endoscopy procedures across the globe. The CMOS Sensor segment accounted for the largest market share in 2020. Based on sensor, segmented into CMOS Sensor and CCD Sensor. CMOS Sensors accounted for the largest share of the global medical cameras market in 2020. This can be attributed various advantages of CMOS sensors over CCD sensors, such as low power consumption, ease of integration, and faster frame rate. Moreover, the cost of manufacturing these sensors is lower than that of CCD sensors.

0 Comments

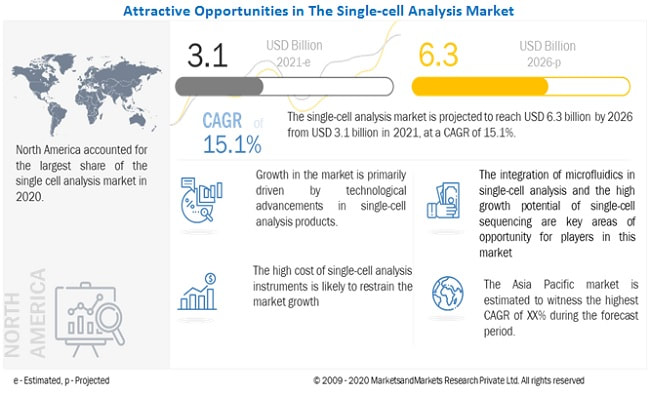

The growth in Single-cell Analysis Market is driven by technological advancements in single-cell analysis products, increasing government funding for cell-based research, growing biotechnology and biopharmaceutical industries, wide applications of single-cell analysis in cancer research, growing focus on personalized medicine, and the increasing incidence and prevalence of chronic and infectious diseases. However, the high cost of single-cell analysis products is expected to restrain the growth of this market to a certain extent during the forecast period. According to the new market research report “Single-cell Analysis Market by Cell Type (Human, Animal, Microbial), Product (Consumables, Instruments), Technique (Flow Cytometry, NGS, PCR, Mass Spectrometry, Microscopy), Application (Research, Medical Application), End User – Global Forecasts to 2025” published by MarketsandMarkets™, is projected to reach USD 5.6 billion by 2025 from USD 2.1 billion in 2019, at a CAGR of 17.8% during the forecast period. Recent Developments:

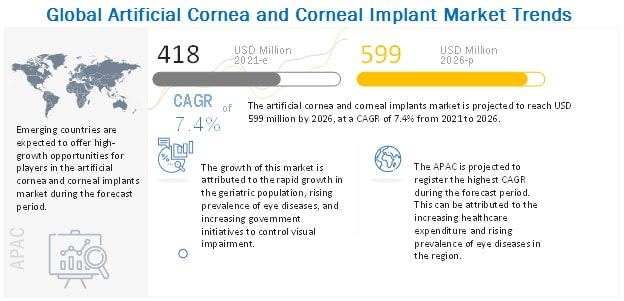

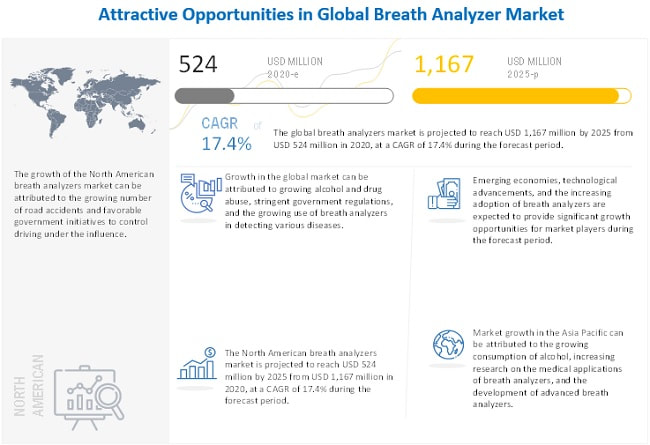

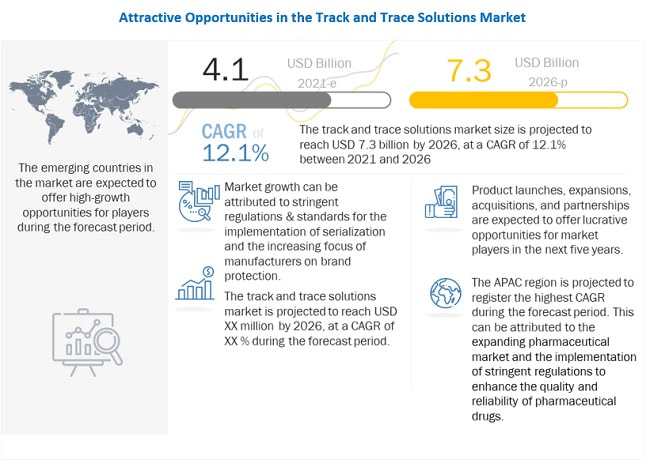

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=171955254 Geographically; the global single-cell analysis market is segmented into five major regions, namely, North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2018, North America accounted for the largest share of the market. The growth in this market can be attributed to the increasing drug development activities in the pharmaceutical and biotechnology industries, rising prevalence of chronic and infectious diseases, and an increase in stem cell research activities. Prominent players in the single-cell analysis market include Becton, Dickinson and Company (US), Danaher Corporation (US), Merck Millipore (US), QIAGEN (Netherlands), Thermo Fisher Scientific (US), General Electric Company (US), 10x Genomics (US), Promega Corporation (US), Illumina (US), Bio-Rad Laboratories (US), Fluidigm Corporation (US), Agilent Technologies (US), NanoString Technologies (US), Tecan Group (Switzerland), Sartorius AG (Germany), Luminex Corporation (US), Takara Bio (Japan), Fluxion Biosciences (US), Menarini Silicon Biosystems (Italy), and LumaCyte (US). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=171955254 Market Segmentation in Detailed: The consumables segment accounted for the largest share of the single-cell analysis market. Based on product, segmented into consumables (beads, microplates, reagents, assay kits, and other consumables) and instruments (flow cytometers, NGS systems, PCR instruments, spectrophotometers, microscopes, cell counters, HCS systems, microarrays, and other instruments). The consumables segment accounted for the largest market share in 2018. The large share of this segment can be attributed to the frequent purchase of these products as compared to instruments, which are considered as a one-time investment, and their wide applications in research and genetic exploration, exosome analysis, and isolation of RNA and DNA. The human cells segment dominates the single-cell analysis market Based on cell type, the market is segmented into human, animal, and microbial cells. The human cells segment accounted for the largest market share in 2018. The large share of this segment can be attributed to the high utilization of human cells in research laboratories and academic institutes.  The Artificial Cornea and Corneal Implant Market Growth is largely driven by the The growing geriatric population and the rising prevalence of eye diseases are the major drivers for the artificial cornea and corneal implants market. The increasing prevalence of eye disorders and government initiatives to control visual impairment are further boosting the market growth. According to the new market research report “Artificial Cornea and Corneal Implant Market by Type (Human Cornea, Artificial Cornea), Transplant Type (Penetrating Keratoplasty, Endothelial Keratoplasty), Disease Indication, End Users (Hospitals, Specialty Clinics & ASCs) – Global Forecast to 2026” published by MarketsandMarkets™, the global artificial cornea implant market is projected to reach USD 599 million by 2026 from USD 418 million in 2021, at a CAGR of 7.4% from 2021 to 2026. Growth Opportunity: Shortage of corneal donors; There is a significant requirement of corneal donors across the globe, as approximately 10 million people are in need of corneal transplants. Densely populated counties such as India suffer from a significant shortage of donor corneas, and there is a waiting period of more than six months for corneal transplants among patients suffering from corneal blindness. Approximately 6.8 million people in the country have poor vision in one eye, and nearly one million people have poor vision in both eyes due to corneal disorders. It was estimated that by the end of 2020, India would suffer from 10.6 million cases of unilateral corneal blindness. In 2019, around 120,000 people were affected by corneal blindness. Around 250,000 corneas are needed annually in the country; however, the total number of corneas donated each year is around 25,000. The high burden of corneal blindness, coupled with a shortage of corneal donors, is expected to offer high-growth opportunities to manufacturers of corneal implants. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=182165973 Geographically, the artificial cornea and corneal implant market is segmented into North America, Europe, the Asia Pacific, Latin America, and Middle East & Africa. Asia Pacific is projected to witness highest CAGR during the forecast period of 2021–2026. The Asia Pacific forms the most lucrative region in the artificial cornea and corneal implants market, owing to the large population in countries such as China and India, rapid growth in the geriatric population, improving healthcare infrastructure, growing per capita income, and the rising focus of key market players on this region. The prominent players in this market are AJL Ophthalmic (Spain), CorneaGen Inc. (US), Addition Technology, Inc. (US), LinkoCare Life Sciences AB (Sweden), Presbia plc (Ireland), Mediphacos (Brazil), Aurolab (India), Cornea Biosciences (US), DIOPTEX GmbH (Austria), EyeYon Medical (Israel), Massachusetts Eye and Ear (US), Florida Lions Eye Bank (US), SightLife (US), Advancing Sight Network (US), San Diego Eye Bank (US) and L V Prasad Eye Institute (LVPEI, India). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=182165973 Market Segmentation in Detailed: The artificial cornea segment is projected to witness fastest growth during the forecast period On the basis of type, segmented into human cornea and artificial cornea. The artificial cornea segment is projected to witness fastet growth during the forecast period. An artificial corneal transplant, also known as keratoprosthesis (KPro), enables the restoration of vision in conditions wherein the cornea and the eye surface is affected or damaged. The scarcity of human eye donors has resulted in the development of innovative solutions such as artificial corneas. Additionally, individuals with a history of multiple previous graft failures, Stevens-Johnson syndrome, chemical burns, severe dry eyes, congenital aniridia, or limbal stem cell deficiency are indications for KPro. One of the commonly used keratoprosthesis is Boston Keratoprosthesis (Boston KPro). To date, over 15,000 Boston KPro have been implanted across the globe. Penetrating keratoplasty segment accounted for the largest share of artificial cornea and corneal implant market in 2020. On the basis of transplant type, segmented into penetrating keratoplasty, endothelial keratoplasty, and other transplants (including anterior lamellar keratoplasty (ALK) and keratoprosthesis). In 2020, the penetrating keratoplasty segment accounted for the largest share of the global artificial cornea and corneal implants market. The large share of this segment can be attributed to the rising number of people suffering from eye disorders such as infectious keratitis and injury of the eyeball. Breath Analyzer Market worth $1,167 million by 2025 – Growing Use in Detecting Various Diseases8/12/2021  The Growth in Breath Analyzer Market can primarily be attributed to factors such as alcohol and drug abuse, stringent government regulations and increasing use of breathalyzers in detecting various diseases. According to the new market research report “Breath Analyzer Market by Technology (Fuel Cell, Semicoductor Oxide Sensor, Others), End User (Law Enforcement Agencies, Enterprises, Individuals ), Application, Region (North America, Europe, APAC, RoW) – Global Forecast to 2025” published by MarketsandMarkets™, the breathalyzers analyzer market is expected to reach USD 1,167 million by 2025 from USD 524 million in 2020, at a CAGR of 17.4% during the forecast period. Growth Drivers: Growing alcohol and drug abuse; In 2018, about 10,511 people in the US died because of drunk driving. Excessive alcohol consumption leads to an increased risk of developing more than 200 diseases, including liver cirrhosis and some cancers. In US almost 30 people die every day due to driving under the influence (DUI) Also, high blood alcohol content was observed in~20% of fatally injured drivers in accidents in developed countries. The growing number of road accidents caused by drunk driving and drug abuse has increased the demand for breath analyzers, as these devices assist in monitoring the presence of different compounds and measuring the blood alcohol content in a breath sample. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=57484012 Geographically; the breath analyzer market is segmented into North America, Asia-Pacific, Europe and Rest of the world(RoW). Asia Pacific is expected to register the highest CAGR during the forecast period. The major factors driving the growth of the Asia Pacific market include as growing consumption of alcohol, increasing research on the medical applications of breath analyzers, and the development of advanced breath analyzers. The prominent players in the global breath analyzer market include Drägerwerk AG & Co. KGaA (Germany), MPD, Inc (US), Lifeloc Technologies (US), BACtrack, Inc. (US), Quest Products, Inc. (US), Akers Biosciences, Inc. (US), Intoximeter, Inc. (US), AK GlobalTech Corporation (US), Alcohol Countermeasure Systems Corporation (Canada), EnviteC-Wismar GmbH (Germany), Lion Laboratories Ltd. (UK) Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=57484012 Market Segmentation in Detailed: The fuel cell segment is expected to account for the largest share of the breath analzyer market in 2020 Based on technology, segmented into fuel cells, semiconductor oxidesensors, and other technologies (infrared spectroscopy and chemical crystals). In 2020, the fuel cellssegment accounted for the largest share of the global breath analyzers market. Fuel cells are the mostwidely used technology in breath analyzers. Fuel cell-based breath analyzers offer an extremely high levelof accuracy, sensitivity, and reliability. They are specifically tuned to detect alcohol and do not requiremultiple sensors. These analyzers are considered the gold standard of handheld alcohol testers for bothpersonal and professional use. The alcohol detection segment is expected to account for the largest share of the breath analyzer market in 2020 On the basis of application, segmented into alcohol detection, drug abuse detection, and medical applications. The alcohol detection segment accounted for the largest market share in 2020. This segment is also projected to register the highest CAGR during the forecast period. The growth of this segment is primarily driven by stringent government regulations for driving under the influence (DUI).  The implementation of track and trace solutions and technologies is an important strategy adopted by many manufacturing companies and regulatory bodies in recent years. Growth in Track and Trace Solutions Market is largely driven by stringent regulations & standards for the implementation of serialization, increasing focus of manufacturers on brand protection, growth in the number of packaging-related product recalls, high growth in the generic and OTC markets, and growth in the medical device industry. On the other hand, the high costs and long implementation timeframe associated with serialization and aggregation and the huge setup costs are expected to limit market growth to a certain extent. According to the new market research report “Track and Trace Solutions Market by Product (Plant Manager, Checkweigher, Barcode Scanner, Monitoring), Technology (2D Barcode, RFID), Application (Serialization, Aggregation, Reporting), End User (Pharma, Food, Medical Devices) – Global Forecast to 2026″ published by MarketsandMarkets™, is projected to reach USD 7.3 billion by 2026 from USD 4.1 billion in 2021, at a CAGR of 12.1% during the forecast period. Opportunities: Remote authentication of products; Traditional brand protection technologies such as anti-theft and authentication are intended to protect individual items rather than safeguard the entire supply chain. There is a high possibility of fake products being introduced at any stage in the supply chain. To combat counterfeiting and identify massive product items, a solution with automatic and non-line-of-sight capabilities is required. The demand for technologies with modular designs, which fit enterprise needs, has increased in the last few years. For instance, track and trace technologies based on RFID maintain an electronic pedigree that records the transaction information of products within the supply chain. This approach proved to be a standout for protecting the supply chain against infiltration, theft, and fraud and supporting remote authentication in the brand protection supply chain. Technologies that are scalable from a single production line to a multi-facility/multi-line infrastructure while minimizing the initial investment are projected to gain attention in the coming future. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=158898570 Geographically; The track and trace solutions market studied in this report is divided into five major regions, namely, North America, Europe, the Asia Pacific, Latin America, and the Middle East & Africa. In 2020, North America accounted for the largest share of 42.9% of the global track and trace solutions market, followed by Europe (33.5%). The presence of developed healthcare systems in the US & Canada; the presence of many pharmaceutical & biotechnology companies and medical device manufacturers; stringent regulations regarding serialization; and the growing medical devices market are major factors driving market growth in North America. Asia Pacific (APAC) is the fastest-growing market and is projected to grow at the highest CAGR of 13.8% for track and trace solutions. Some of the prominent players in the track and trace solutions market are OPTEL GROUP (Canada), Mettler-Toledo International Inc. (US), Systech International Inc. (US), TraceLink Inc. (US), Antares Vision (Italy), SAP (US), Xyntek Inc. (US), SEA Vision Srl (Italy), Syntegon (Germany), Körber Medipak Systems AG (Switzerland), Siemens AG (Germany), Uhlmann Group (Germany), JEKSON VISION (India), Videojet Technologies, Inc. (US), Zebra Technologies Corporation (US), Axway Inc. (US), ACG Worldwide (India), Laetus GmbH (Germany), and WIPOTEC-OCS (Germany). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=158898570 Market Segmentation in Detailed: “The Software segment accounted for the largest market share in 2020.” Based on products, the track and trace solutions market is segmented into software, hardware components, and standalone platforms based on product. The software segment accounted for the largest share—60.1%—of the track and trace market in 2020. Market growth is largely driven by the increasing awareness about secure packaging, the rising number of counterfeit drugs and related products, and growing awareness of brand protection. In addition, regulatory compliance is further supporting the growth of this market. The standalone platforms segment is expected to register the highest CAGR of 15.9% during the forecast period. Orthopedic Braces and Supports Market - Segmentation, Major Players & Geographical Analysis8/9/2021  The Growth in Orthopedic Braces and Supports Market is driven primarily by the increasing prevalence of orthopedic diseases & disorders, continuous product commercialization, greater product affordability and market availability, rising number of sports and accident-related injuries, and growing public awareness related to preventive care. According to the new market research report “Orthopedic Braces and Supports Market by Product (Knee, Ankle, Hip, Spine, Shoulder, Neck, Elbow, Hand, Wrist), Category (Soft, Hard, Hinged), Application (Ligament (ACL, LCL), Preventive, OA), Distribution (Hospital) & Region – Global Forecast to 2025” published by MarketsandMarkets™, the global orthopedic braces market size is projected to reach USD 4.1 billion by 2025 from USD 3.1 billion in 2020, at a CAGR of 5.8% during the forecast period Growth Driver: Increasing prevalence of orthopedic diseases and disorders; Orthopedic braces and supports are increasingly being used during clinical management of various orthopedic diseases and disorders such as osteoarthritis, rheumatoid arthritis, osteoporotic fractures, and carpal tunnel syndrome. These products offer higher clinical efficacy and fast patient recovery compared to alternative therapies such as pain medications.

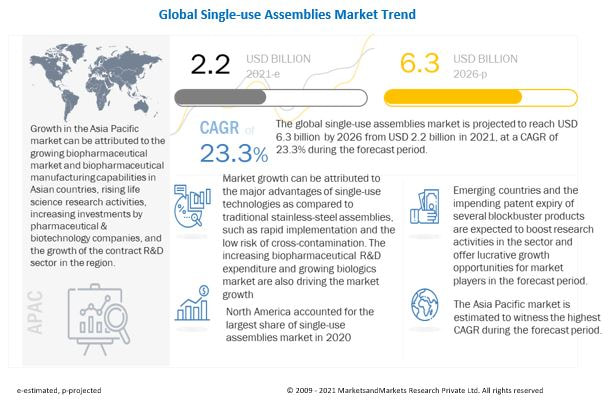

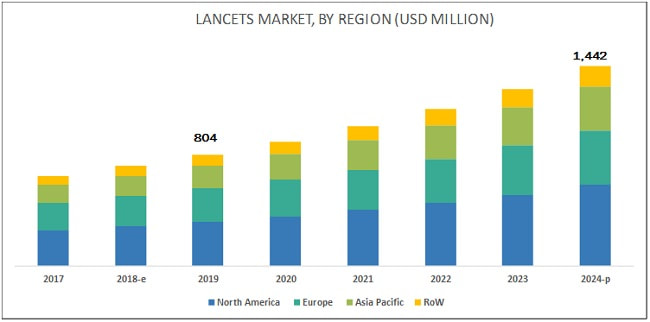

The incidence of orthopedic diseases and disorders is expected to increase further in the coming years with the increasing prevalence of obesity and related lifestyle disorders, as obese individuals are at a higher risk of orthopedic & musculoskeletal injuries as well as diabetes. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=24806829 Geographically; Asia Pacific is estimated to be the fastest-growing market for orthopedic braces and supports during the forecast period. The Asia Pacific market is driven principally by the rising geriatric and obese population (coupled with the significant prevalence of orthopedic & diabetes-related diseases in this population segment), increasing GDP and healthcare expenditure in APAC countries, and growing public awareness. Furthermore, increasingly localized product manufacturing, favorable government regulations, and the focus of global product manufacturers on expanding their presence in APAC countries are aiding the market growth. Key Market Players; Breg, Inc. (US), DJO Finance LLC (US), Bauerfeind AG (Germany), DeRoyal Industries, Inc. (US), and Össur Hf (Iceland) are the top five players in the global orthopedic braces and supports market. Other prominent players operating in this market include Oppo Medical, Inc. (US), Zimmer Biomet Holdings, Inc. (US), Ottobock Holding GmbH & Co. KG (Germany), Bird & Cronin, Inc. (US), Remington Products Company (US), 3M Company (US), medi GmbH & Co. KG (Germany), BSN medical (Germany), Thuasne Group (France), Becker Orthopedic (US), and Trulife (Ireland). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=24806829 Market Segmentation in Detailed: By type, Soft and elastic braces are the most common bracing & support products in orthopedics. These are easy to use, flexible, provide unrestricted patient mobility, and are highly customizable, as compared to other surgical alternatives. Growth in this market can primarily be attributed to the growing availability of advanced products, increasing adoption & patient preference for orthopedic braces in post-operative & preventive care, and the supportive reimbursement scenario for target products across mature markets. Ligament injury is the largest application segment of the orthopedic braces and supports market Orthopedic bracing and support products are used for the clinical management of ligament injuries such as anterior cruciate ligament, posterior cruciate ligament, medial collateral ligament, lateral collateral ligament, and coronary ligament injuries. The large share of the ligament injury segment can be attributed to increasing public participation in sports & athletic activities (coupled with the rising incidence of sports-related injuries), rising number of accidents worldwide, and the growing availability of medical reimbursement for ligament injuries.  The growth of the single-use assemblies market can primarily be attributed to the major advantages of single-use technologies as compared to traditional stainless-steel assemblies, such as rapid implementation and the low risk of cross-contamination. The increasing biopharmaceutical R&D expenditure and growing biologics market are also driving the market growth. According to the new market research report “Single-use Assemblies Market by Product (Bag Assembly, Filtration Assembly, Bottle Assembly, Mixing Assembly), Application (Filtration, Storage), Solution (Standard, Customized), End User (Pharmaceutical, Biopharma, CMOs, CROs) – Global Forecast” published by MarketsandMarkets™, is projected to reach USD 6.3 billion by 2026 from USD 2.2 billion in 2021, at a CAGR of 23.3% during the forecast period. Opportunity: Emerging countries; Emerging economies such as China, India, and Indonesia are expected to offer significant growth opportunities for players operating in the single-use assemblies market. This can be attributed to high growth in their respective pharmaceutical & biopharmaceutical sectors owing to the presence of less-stringent regulatory policies as well as low-cost and skilled labor. In addition, the high and growing incidence of chronic and infectious diseases, rising disposable income levels, improving access to healthcare services, and the implementation of favorable government policies are also attracting companies to these countries. The growing presence of global as well as local pharmaceutical & biopharmaceutical companies in these countries is a major factor driving the demand for single-use assemblies. India, China, Korea, and Brazil are a hub for bioprocess outsourcing owing to their cost advantages and the talent pool offered by these countries. For instance, India has more than 175 US FDA-approved pharmaceutical manufacturing units that offer ~40% lower operational costs in comparison to its western counterparts. Also, according to the India Brand Equity Foundation, Indian companies received 304 Abbreviated New Drug Application (ANDA) approvals from the US FDA in 2017. Similarly, China is the second-largest pharmaceutical market globally, with total spending of USD 137 billion in 2018. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=46226549 Geographically; the Asia Pacific region accounted for the fasted growing region of the single-use assemblies market. This can be attributed to the growing biopharmaceutical market and biopharmaceutical manufacturing capabilities in Asian countries, rising life science research activities, increasing investments by pharmaceutical & biotechnology companies, and the growth of the contract R&D sector. Prominent players operating in the single-use assemblies market are Thermo Fisher Scientific, Inc. (US), Sartorius Stedim Biotech (France), Danaher Corporation (US), Merck KGaA (Germany), Avantor, Inc. (US), and Saint-Gobain (France). Thermo Fisher Scientific is one of the leading players in the market. The company offers a range of single-use assemblies for downstream, upstream, and fill-finish stages of bioprocessing. The company’s BioProcess containers and transfer assemblies are single-use flexible container systems for critical liquid handling applications in biopharmaceutical & biomanufacturing operations. In the last few years, the company has majorly focused on expanding its bioproduction capabilities and market presence. In 2020, it saw significant growth in its Life Sciences segment, driven by the demand for diagnostic testing for COVID-19; the demand for bioproduction products, including single-use assemblies, saw a significant surge. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=46226549 Market Segmentation in Detailed: On the basis of applications, segmented into filtration, cell culture & mixing, storage, sampling, fill-finish applications, and other applications. In 2020, the filtration segment accounted for the largest share of the single-use assemblies market. The adoption of single-use assemblies for filtration is increasing rapidly due to their benefits in this application, such as ease of column cleaning, sterilization, packing, and simplified validation and cleaning, which allows more batches to be run. Based on solution, segmented into standard solutions and customized solutions. The standard solutions segment accounted for a larger share of the single-use assemblies market in 2020. The adoption of standard solutions is high in the pharmaceutical & biopharmaceutical industries due to the advantages these solutions offer, such as manufacturing process efficiency with reduced capital costs, improved flexibility with the use of pre-qualified components for building assemblies, reduced implementation time, and more flexibility with production planning.  The report “Lancets Market by Type (Safety Lancets (Push button, Pressure Activated, Side Button), Personal Lancets), Application (Glucose Testing, Hemoglobin Testing), End User (Hospital, Clinic, Homecare), Region – Global Forecast to 2024″, the lancing devices market is projected to grow at a CAGR of 12.4% during the forecast period to reach USD 1,442 million by 2024 from USD 804 million in 2019. The Growth in the lancets market is mainly driven by the growing prevalence of diabetes and the high prevalence of infectious diseases across the globe. In addition, emerging markets such as India and China are expected to offer growth opportunities for players operating in the market during the forecast period. However, the risk of needlestick injuries, the reuse of lancets, and the poor reimbursement scenario in developing countries are restricting the growth of this market. Recent Developments

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=86063487 The Safety Lancet is expected to be the most widely used type of the lancets market The safety lancets accounted for the largest market share in 2018. This is primarily be attributed to the advantages associated with safety lancets such as their ease of use, the capability to prevent needlestick injuries and cross-contamination, and painlessness of vein puncture. In line with this, According to PharmaJet, in the US, around 600,000 to 800,000 needlestick injuries are reported every year. This is expected to increase the demand of safety lancets. The Glucose testing segment is expected to account for the largest share of the lancets market application The glucose testing segment accounted for the largest share of the lancing devices market, by application, in 2018. This is primarily due to the increasing prevalence of diabetes, and the need for its prevention and management. For instance, according to the International Diabetes Federation (IDF), in 2017, there were almost 425 million people suffering from diabetes worldwide, and this figure is expected to increase to 629 million by 2045. The growing prevalence of diabetes has resulted in the increased adoption of lancets to effectively handle the growing patient pool. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=86063487 Asia Pacific to dominate the lancets market during the forecast period In 2018, North America dominated the market, followed by Europe. Increasing prevalence of diabetes and favorable reimbursement scenario in the region are the factors propelling the growth of the market in the region. The Asia Pacific region is projected to register the highest growth rate in the global lancing devices and lancets market during the forecast period. This is primarily attributed to the rapid economic growth, rising awareness about diabetes treatment, rising geriatric population in China and India, and Japan’s growing healthcare industry. Global Key Leaders: Prominent players in the lancets market are Becton, Dickinson and Company (US), Roche Diagnostics (Switzerland), Ypsomed (Switzerland), B. Braun Melsungen (Germany), Terumo Corporation (Japan), Own Mumford (UK), HTL-STREFA S.A (Poland), ARKRAY (Japan), Sarstedt (Germany), and SteriLance Medical (Suzhou) (China).  The report “Synthetic Stem Cells Market by Application (Cardiovascular Disease, Neurological Disorders, Other Applications (Cancer, Diabetes, Gastrointestinal, Musculoskeletal Disorders)), Region (North America (US, Canada}, Europe, APAC, RoW) – Global Forecast to 2028″, the artificial stem cells market size is expected to grow from USD 14 million in 2023 to USD 37 million by 2028, at a CAGR of 22.5% during the forecast period. The study involved four major activities in estimating the current market size for synthetic stem cells. Exhaustive secondary research was conducted to collect information on the market as well as its peer and parent markets. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. The top-down approach was employed to estimate the complete market size. Market Size Estimation; The top-down approach was used to estimate and validate the total size of the synthetic stem cells market. The approach was also used extensively to estimate the size of various sub-segments in the market. The research methodology used to estimate the market size includes the following:

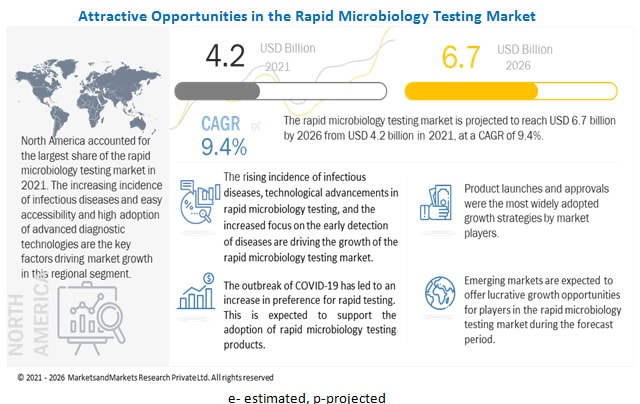

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=4959435 The cardiovascular diseases segment is expected to command the largest share of the overall synthetic stem cells market during the forecast period. The Artificial stem cells market, by application, is estimated to be dominated by the cardiovascular diseases segment in 2023. This is attributed to the fact that the synthetic stem cells have been firstly developed for cardiac tissue and are tested in mice models. After the successful pre-clinical testing of cardiac synthetic stem cells, these cells will enter the clinical phase of development and are expected to hit the market by 2023. North America to lead the synthetic stem cells market with accelerated R&D activities in stem cell therapy research. North America is estimated to account for the largest share of the market in 2023. North America is the pioneer of synthetic stem cell technology. Also, North America leads in the R&D of stem cell therapies globally, with the registration of the highest number of clinical trials (more than 1400) on stem cells till 2018. This is further backed by the high rate of adoption of advanced therapies in the US (more than 600 stem cell therapy clinics in the US in 2016). The key developers of synthetic stem cell technology are North Carolina State University (NCSU) (US) and Zhengzhou University (China). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=495943  The report “Rapid Microbiology Testing Market by Method (Growth, Viability), Product (Automated Microbial Identification & AST System, PCR, Reagent), Application (Clinical Diagnosis, Environmental), End User (Labs, Hospitals, Industry) – Global Forecast to 2023″, is expected to reach USD 5.09 billion, at a CAGR of 8.1%. The Growth in the rapid microbiology testing market can be attributed to factors such as the rising prevalence of infectious diseases; ongoing technological advancements; increasing food safety concerns; increased funding, research grants, and public-private investments; and increasing awareness about rapid microbiology testing. Growth Driver- Technological advancements; Over the years, there has been a gradual shift from conventional microbiology testing toward rapid testing methods. This shift has been driven by the introduction of newer and faster technologies to avert the need for the biological amplification of bacteria for detection. Rapid advancements in the field of microbial testing help to overcome limitations such as long procedural times and long exposure to pathogenic strains with conventional testing methods. Continuous technological advancements in microbiology testing, in terms of efficacy, efficiency, accuracy, faster results, and improved functionality, are generating increased interest among clinical laboratories, hospitals, academic institutes, research laboratories, and pharmaceutical and biotechnology companies. These tests provide a cost-effective alternative for microbial identification by reducing the per procedure consumable cost. Clinical diagnostics, food and beverage testing, and environmental applications use rapid technologies in microbial identification to identify microbes from different samples. With recent advances in genomics and proteomics, microbial identification and quantification methodologies have evolved rapidly. Several emerging molecular diagnostic techniques are increasingly being used for early detection as they eliminate the complex needs of detecting the whole organism by amplifying cellular components, like nucleic acid, or using signal amplification to enhance detection capability. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=31548521 The instruments segment is expected to account for the largest share of the products market; On the basis of product, segmented into instruments, reagents & kits, and consumables. The instruments segment is further categorized into automated ID/AST systems, mass spectrometers, PCR systems, bioluminescence- and fluorescence-based detection systems, cytometers, active air samplers, and other instruments. The automated microbial ID/AST systems segment is expected to command the largest share of the global rapid microbiology testing market in 2018. This is primarily due to the ability of these systems to produce rapid, accurate, reliable, and cost-effective results. Growth-based rapid microbiology testing is expected to account for the largest share of the market; Based on method, classified into segments growth-based, viability-based, cellular component-based, nucleic acid-based, and other rapid microbiology testing methods. The growth-based segment is expected to account for the largest share of the rapid microbiology testing market in 2018. The large share of this segment can be attributed to factors such as the ease of processing (this method uses conventional liquid or agar media), the limited requirement of skilled professionals, and supportive government regulations. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=31548521 Geographical View in-detailed: The rapid microbiology testing market is segmented into North America, Europe, Asia Pacific, and the Rest of the World. North America is expected to account for the largest share of the global microbiology testing market during the forecast period (2018–2023). The large share of this market can be attributed to the growing technological advancements in the field of rapid microbial testing, rising incidence of infectious diseases, and growing food safety concerns. In addition, the region has supportive government initiatives that help create awareness and promote the adoption of advanced microbial testing devices among key end users, thereby propelling the growth of the market in North America. Global Key Leaders: The major players operating in the rapid microbiology testing market include bioMérieux SA (France), Danaher Corporation (US), and Becton, Dickinson and Company (US), among others. |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed