|

The report “Cold Pain Therapy Market by Product (OTC (Gels, Creams, Patches, Wraps, Pads), Prescription Devices (Motorized, Non-Motorized), Applications (Musculoskeletal, Post Op, Sports Medicine), Distribution Channel(Hospital, Retail) – Global Forecasts to 2025“, is projected to reach USD 2.0 billion by 2025 from USD 1.6 billion in 2020, at a CAGR of 4.4% during the forecast period.

The Factors such as increasing prevalence of arthritis and the rising number of sports injuries are the key factors boosting the demand for cold pain therapy products for the management of pain. Moreover, growing awareness about the availability of cost-effective cooling pain relief products and the ease of application of cold pain therapy products are anticipated to accelerate the adoption of these products in the coming years Growth Driver: Increase in the prevalence of incidence of sports injuries; Musculoskeletal injuries are the most common forms of sports-related injuries. Some of the common injuries include ankle sprains, knee injuries, fractures, joint injuries, tennis elbow (epicondylitis), and dislocations. Cold pain therapy products, such as ice packs and sprays, are the most commonly used products for the management of pain associated with sports-related injuries as they provide instant pain relief. Furthermore, with rising disposable income levels, growing health awareness, growing obesity rate, and growing stress levels, the emphasis on gym activities and workouts among adults across the globe has increased augumenting the market growth. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=55543905 Musculoskeletal Disorders accounted for the largest share of the cold pain therapy market; The growing prevalence of musculoskeletal disorders gloablly and the demand for thecost effective pain relief ptroducts and the growing awareness about the avaolibility of effective cold therapy products for the musculoskeletal disorders pain management and rise in the geriatric patient population are likely to fuel the growth of this segment during the forecast period. Retail Pharamcies accounted for the largest share of the cold pain therapy market; The segment accounted for the highest share owing to the increasing growing awareness about the availability of effective cold pain therapy products in retail pharmacies, increase in the expansion of retail pharmacies through collaboration with e-pharacies and the major focus on strengthening the brand connection among customnesr by widening their personal consulatnat services are some of the factors anticipated to preopel the growth of this segment. Geographical View in-detailed: The emerging Asian countries, such as China, India, South Korea, Japan and Singapore, are offering high-growth opportunities for market players. The Asia Pacific cold pain therapy market is projected to grow at the highest CAGR of 5.6% from 2020 to 2025. Growing preference for topical products, especially cold patches, expansion of helathacre infrastructure, growing awareness of cold therapy products the region. Moreover, emergence of key players with established product portfolio are driving the growth of the APAC market. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=55543905 Global Key Leaders: The Prominent players in Cold Pain Therapy Market are Sanofi (France), Pfizer (US), Hisamitsu Pharmaceutical (Japan), ROHTO Pharmaceutical (Japan), Beiersdorf (Germany), Johnson & Johnson (US), Medline Industries (US), Össur (Iceland), Performance Health (US), Breg (US), Romsons Group of Industries (India), Unexo Life Sciences (India), and Bird & Cronin (US)

0 Comments

The report “Breast Reconstruction Market by Product (Breast implant (Silicone, Saline), Tissue Expander, Acellular Dermal Matrix), Procedure (Immediate, Delayed, Revision), Type (Unilateral, Bilateral), End User (Hospital, Cosmetology Clinics) – Global Forecast to 2025″, is projected to reach USD 603 million by 2025 from USD 430 million in 2020, at a CAGR of 7.0% from 2020 to 2025. The rising incidence of breast cancer and the availability of reimbursement for breast reconstruction are major driving factors for the market. Moreover, the development of 3D-printed breast implants is expected to offer significant growth opportunities to market players in the coming years. Recent Developments:

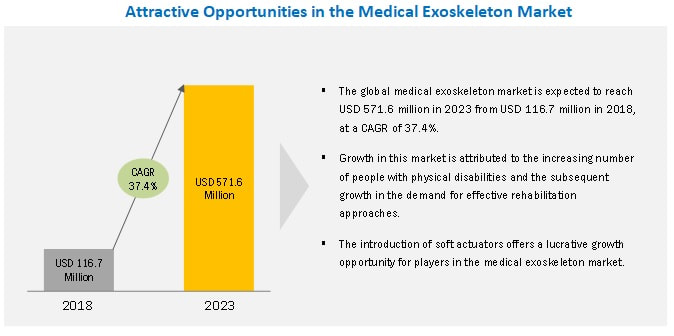

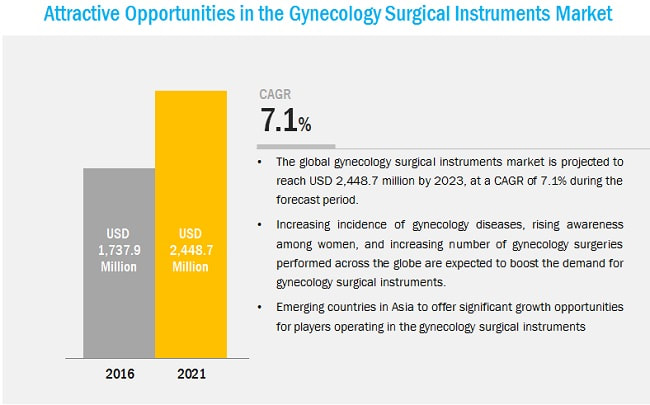

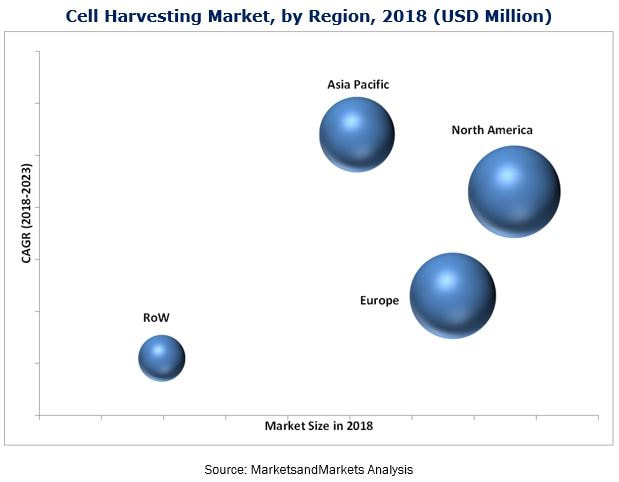

https://www.marketsandmarkets.com/requestsampleNew.asp?id=186501593 Market Segmentation in Detailed: Based on the product, segmented into breast implants, tissue expanders, and acellular dermal matrix. The breast implants segment accounted for the largest market share in 2019. Based on the procedure, the breast reconstruction market is segmented into immediate, delayed, and revision procedures. The immediate procedures segment accounted for the largest market share in 2019. This is primarily attributed to the increasing number of surgeries post-mastectomy and rising awareness. Based on type, segmented into unilateral and bilateral. The unilateral segment accounted for the largest market share in 2019. The increasing incidence of breast cancer and rising awareness are major factors responsible for the dominant share of this segment. Geographical View in-detailed: The breast reconstruction market is segmented into North America, Europe, the Asia Pacific, and the Rest of the World. In 2019, North America held the largest share of the market, followed by Europe. The rising incidences of breast cancer, increasing awareness of breast reconstruction, and FDA approvals for breast reconstruction products in this region are the major factors driving the growth of the breast reconstruction in North America. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=186501593 Global Key Leaders: The prominent players operating in the global breast reconstruction market are Johnson & Johnson (US), Allergan (Ireland), Ideal Implant Incorporated (US), Sebbin (France), GC Aesthetics (Ireland), Polytech Health & Aesthetics (Germany), Sientra (US), Integra Lifesciences (US), RTI Surgical Holdings (US), Establishment Labs S.A. (Costa Rica), and Silimed (Brazil). Johnson and Johnson (US) is the dominant player in the breast reconstruction market. The company has a strong portfolio of breast reconstruction products. It has established a significant footprint in Europe, Asia, and Latin, South, & North America. It focuses on organic and inorganic strategies such as product launches. The company operates in this market through Mentor, which it acquired in January 2009. J&J has a strong presence in over 60 countries and a wide network of subsidiaries across the globe. It recently launched a new warranty program for all MENTOR breast implants sold in the US.  The report “Medical Exoskeleton Market by Component (Hardware (Sensor, Actuator, Control System, Power Source), Software), Type (Powered, Passive), Extremities (Lower, Upper) & Mobility (Mobile, Stationary) – Global Forecast”, is projected to reach USD 571.6 million, at a CAGR of 37.4%. A medical exoskeleton, also known as a wearable robot, is a robotic machine suite worn by humans in place of their limbs to complement, substitute, and enhance human functions. It helps in physical movements by offering increased strength and endurance. The Factors such as the increasing number of people with physical disabilities and subsequent growth in the demand for effective rehabilitation approaches; agreements and collaborations among companies and research organizations for the development of the exoskeleton technology; and increasing insurance coverage for medical exoskeletons in several countries driving the growth of the medical exoskeleton market. However, the high cost of medical exoskeletons may restrict market growth to a certain extent. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=138546702 Growth Driver: Increasing number of people with physical disabilities and subsequent growth in the demand for effective rehabilitation approaches; Globally, the number of people with physical disabilities is increasing majorly due to the rising geriatric population, increasing number of road accidents and severe trauma injuries, and increasing prevalence of stroke, among other factors. All major regions across the globe are witnessing significant growth in their geriatric populations, and this trend is expected to continue in the coming years. Lower extremity medical exoskeletons are expected to dominate the market in 2018 By extremity, the market is segmented into lower extremity medical exoskeletons and upper extremity medical exoskeletons. In 2018, lower extremity medical exoskeletons segment is expected to account for the largest share of the global medical exoskeleton market. Lower extremity exoskeletons provide stability to paralyzed and geriatric patients and offer weight-bearing and locomotion capabilities. As a result, they are more widely adopted for rehabilitation applications. The mobile segment is projected to grow at the highest CAGR during the forecast period Based on mobility, the medical exoskeleton market is segmented into mobile and stationary exoskeletons. The mobile segment is expected to register the highest CAGR during the forecast period. The growth of this segment can be attributed to the high demand for compact, light-weight mobile medical exoskeletons that can offer mobility assistance to paralyzed patients. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=138546702 Geographical View in-detailed: North America is expected to dominate the market followed by Europe. The large share of this geographical segment is attributed to the growing geriatric population, increasing demand for self-assist exoskeletons, growing number of spinal cord injuries (SCI), and the high prevalence of stroke in the region. Global Key Leaders: The medical exoskeleton market includes various players. The major players in the market are Ekso Bionics Holdings, Inc. (US), ReWalk Robotics Ltd (Israel), Parker Hannifin Corp (US), Bionik Laboratories Corp (Canada), CYBERDYNE Inc. (Japan), Rex Bionics Ltd. (UK), B-TEMIA Inc. (Canada), Hocoma AG (A Subsidiary of DIH Technologies) (Switzerland), Wearable Robotics SRL (Italy), Gogoa Mobility Robots SL (Spain), and ExoAtlet, O.O.O. (Russia)  The report “Depth Filtration Market by Media Type (Cellulose, Activated Carbon), Product (Capsule, Sheet, Module), Application(Final Product Processing (Biologics), cell Clarification, Viral Clearance, Operation Scale (Manufacturing, Lab) – Global Forecast to 2025″, is estimated to grow from USD 1.7 billion in 2019 to USD 2.9 billion by 2025, at a CAGR of 9.0% during the forecast period. The growth of this market is majorly driven by factors such as the growing adoption of disposable filters and benefits such as ease of use and low cost of media and filters. However, factors such as the requirement of high capital investments for setting up production facilities are expected to restrain the growth of this market during the forecast period. Market Size Estimation; For the calculation of the global market value, the segmental revenue was arrived at based on the revenue mapping of major players active in the protein engineering market. This process involved the following steps: – Generating a list of the major global players operating in the depth filtration market – Mapping the annual revenue generated by major global players from their depth filtration business (or the nearest reported business unit/product category) – Mapping the revenue of major players to cover 70-80% of the global market as of 2018 – Extrapolating the value to 100% to arrive at the global market size Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=143876285 Cartridge filters segment accounted for the largest share of the market. Based on the product, segmented into cartridge filters, capsule filters, filter modules, filter sheets, plate and frame filters, accessories, and other products (includes caps, pads, pods, syringes, bags, and discs). The cartridge filters segment accounted for the largest share of the global depth filtration market in 2019. This can be attributed to the high dirt-holding capacity and long service life of these products. Final Product Processing was the largest application segment in the market Based on the application, segmented into final product processing, cell clarification, raw material filtration, diagnostics, and viral clearance. The final product processing segment is further categorized as small-molecule processing and biologics processing. The raw material filtration market is further segmented into media & buffer filtration and bioburden testing. In 2019, the final product processing segment accounted for the largest share of the depth filtration market due to the, expansion in generics production and the demand for high-quality final products. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=143876285 Geographical View in-detailed: The global depth filtration market is segmented into four major regions, namely, North America, Europe, the Asia Pacific, Latin America, and Middle-East & Africa. In 2019, North America accounted for the largest share of 38.0% of the global market, followed by Europe, with a share of 29.2%. The large share of the North American region can be attributed to a large number of pharmaceutical and biotechnology companies in the region and the presence of a well-established healthcare market. The Asia Pacific market, on the other hand, is expected to register the highest growth during the forecast period. Factors such as increasing research and development by pharmaceutical companies in China, India, and Japan are likely to support the growth of this market. Global Key Leaders: The major companies operating in the global depth filtration market include Merck KGaA (Germany), Danaher Corporation (US), Sartorius AG (Germany), GE Healthcare (US), 3M (US), Parker Hannifin Corporation (US), Porvair Filtration Group (UK), ErtelAlsop (US), Amazon Filters Ltd. (UK), Meissner Filtration Products, Inc. (US), Donaldson Comany, Inc. (US), Eaton Corporation (Ireland), Saint-Gobain Performance Plastics (France), Clariance Technique (Australia), Repligen Corporation (US), Microfilt India Pvt. Ltd. (India), Graver Technologies (US), Gusmer Enterprises (US), Filtrox AG (Switzerland), Pure Process (UK), Membrane Solutions (US), Allied Filter Systems Ltd. (UK), Pentair (US), Membracon (UK), and Phenomenex (US) Danaher (US) held the leading position in depth filtration market primarily due to its strong portfolio of depth filtration including filters and media. In addition, the company has strengthened its market position through the expansion of its product portfolio by collaboration and agreement and expansion.  The report “Gynecology Surgical Instruments Market by Product (Scissors, Forceps, Trocar, SIMS, CUSCO), Application (Laparoscopy, Colposcopy, Hysteroscopy, D&C, Ablation, Biopsy), & End User (Hospital, Clinic, Ambulatory Surgery Center) – Global Forecast”, analyzes and studies the major market drivers, restraints, opportunities, and challenges in North America, Europe, Asia, and Rest of the World (RoW). The Gynecology Surgical Instruments Market is expected to reach USD 2.44 Billion, at a CAGR of 7.1% The market is mainly driven by factors such as high incidence of gynecological diseases, increasing awareness programs, and rising government investments for providing advanced healthcare facilities & services, increasing disposable income in developing countries, and rising incidence of lifestyle disorders. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=122824797 Market Segmentation in Detailed: On the basis of products, segmented into forceps, scissors, needle holders, dilators, trocars, vaginal speculums, and other instruments. Forceps are expected to account for the largest share of the market, in 2016. The growth of the forceps segment is attributed to the increase in the number of gynecological surgeries and the repeated use of forceps in most gynecological surgeries. Based on application, the Gynecology Surgical Instruments Market is further segmented into laparoscopy, hysteroscopy, dilation and curettage, colposcopy, and other applications. Laparoscopy segment is expected to grow at the highest CAGR during the forecast period. Laparoscopy forms the largest and fastest-growing application segment of the market. This is mainly attributed to the various advantages of laparoscopy procedures, which includes less blood loss, shorter hospital stays, and fewer intraoperative & postoperative complications. On the basis of end user, categorized into hospitals, clinics, and ambulatory surgery centers. In 2016, hospitals and clinics were expected to be the major end-user segment in the market. The large share of this segment can be attributed to the increasing incidence of gynecological diseases and the need for timely diagnosis and treatment of these diseases, growing government involvement in increasing awareness regarding women’s health issues, and increase in funding and infrastructural development in hospitals. Geographical View in-detailed: The global gynecology surgical instrument market is dominated by North America, followed by Europe, Asia, and the Rest of the World (RoW). The market in Asia is expected to grow at the highest CAGR during the forecast period. Factors such as increasing awareness programs, high incidence of gynecological diseases, increasing number of hospitals, government initiatives focusing on women’s health, and improvements in the healthcare sector of Asian countries contribute to the growth of the market in Asia. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=122824797 Global Key Leaders: The Gynecology Surgical Instruments Market is highly fragmented with several big and emerging players. Key market players include B. Braun Melsungen AG (Germany), CooperSurgical Inc. (U.S.), Ethicon, Inc. (U.S.), KARL STORZ GmbH & Co. KG (Germany), KLS Martin Group (U.S.), MedGyn Products (U.S.), Olympus Corporation (Japan), Richard WOLF GmbH (Germany), Sklar Surgical Instruments (U.S.), and Tetra Surgical (Pakistan).  The report “Industrial Centrifuge Market by Type (Sediment, Clarifier, Decanter, Disc, Filter, Basket, Screen), Operation (Batch, Continuous), Design (Horizontal, Vertical), End User (Chemical, Power, Food, Wastewater, Pharmaceutical, Paper) and Region – Global Forecast to 2025″ is projected to reach USD 9.0 billion by 2025 from USD 7.2 billion in 2020, at a CAGR of 4.4% between 2020 and 2025. The increasing demand for centrifuges in process industries and the rising need for wastewater management solutions are the major factors driving the growth of this market. However, the high cost of centrifuges is expected to restrain the market growth during the forecast period. Growth Driver: Increasing demand for centrifuge from process industries; Industrial centrifuges are used for the separation of two- or three-phase systems and have a range of industrial applications. Many process industries are increasingly using various types of centrifuge equipment for the separation of two or three immiscible phases. Some of these industries include chemical processing, food processing (including dairy and beverage industry), metal processing, mining and mineral processing, pharmaceutical and biotechnology industries, fuel and biofuel industries, wastewater processing, and pulp and paper industries. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=59612221 Sedimentation centrifuges to dominated the industrial centrifuge market in 2019 On the basis of type, segmented into sedimentation centrifuges and filtering centrifuges. In 2019, the sedimentation centrifuge segment accounted for the largest share of the market. The wide range of industrial applications, the ability to achieve high speeds, increase in oil and gas explorations, and the rising need for wastewater treatment are the major factors contributing to the growth of this segment. The Clarifier segment accounted for the largest share of the sedimentation centrifuge market. On the basis of type, the sedimentation centrifuge market is segmented into clarifiers/thickeners, decanter centrifuges, disk stack centrifuges, hydrocyclones, and other sedimentation centrifuges. In 2019, the clarifier/thickener segment accounted for the largest share of the sedimentation centrifuges market. These centrifuges are used in a number of industries, including wastewater treatment, mining, power, beverages, food processing, pharmaceuticals and biotechnology, and chemicals. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=59612221 Geographical View in-detailed: In 2019, North America accounted for the largest share of the industrial centrifuge market, followed by Europe. The high demand for crude oil, a large number of shale oil and gas drilling activities, government initiatives to manage wastewater, flourishing food processing industry, technological advancements, and government support for the development of innovative centrifugation systems are the key factors driving the growth of the market in North America. Global Key Leaders: Prominent players in the Industrial Centrifuge Market are ANDRITZ AG (Austria), Alfa Laval Corporate AB (Sweden), GEA Group AG (Germany), Mitsubishi Kakoki Kaisha, Ltd. (Japan), Thomas Broadbent & Sons (UK), FLSmidth & Co. A/S (Denmark), Schlumberger Limited (US), Ferrum AG (Switzerland), Flottweg SE (Germany), SIEBTECHNIK TEMA (Germany), HEINKEL Drying & Separation Group (Germany), Gruppo Pieralisi – MAIP S.p.A. (Italy), SPX Flow Inc. (US), HAUS Centrifuge Technologies (Turkey), Elgin Separation Solutions (US), Comi Polaris Systems, Inc. (US), Dedert Corporation (US), US Centrifuge Systems (US), B&P Littleford (US), and Pneumatic Scale Angelus (US).  The report “Cell Harvesting Market by Type (Manual, Automated), Application (Biopharmaceutical, Stem Cell Research), End User (Biotechnology, Biopharmaceutical Companies, Research Institute), and Region (North America, Europe, APAC, Row) – Global Forecast”, the cell harvesters market is expected to reach USD 324.5 Million, at a CAGR of 8.7% The Cell harvesting is the process of harvesting cells from the culture media during upstream and downstream bio-processing. Cell harvesters are used extensively for the cell harvesting process and are compatible with a wide range of assays. Rising investments in regenerative medicine and cell-based research, growth of the biotechnology and bio-pharmaceutical industry, and increasing incidence of chronic and infectious diseases are the major factors that are driving the growth of this market. The objectives of this study are as follows:

Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=209513544 The manual cell harvesters segment dominated the market. On the basis of type, the market is segmented into manual and automated cell harvesters. In 2017, the manual cell harvesters segment accounted for the largest share of this market. The high share of the manual harvesters segment can be attributed to their ease of use and low price as compared to automated harvesters. The biotechnology & biopharmaceutical companies segment dominated the market. In the end user, the cell harvesting market is segmented into research institutes, biotechnology & biopharmaceutical companies, and other end users. In 2017, the biotechnology & biopharmaceutical companies segment accounted for the largest share of the cell harvesters market. The high share of this segment can be attributed to the high prevalence of chronic diseases. Biotechnology & biopharmaceutical companies conduct R&D activities to develop new products for the treatment of these diseases. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=209513544 Geographical View in-detailed: The global cell harvesting market is segmented into North America, Europe, Asia Pacific, and the Rest of the World (RoW). While North America held the largest share of the market in 2017, Asia Pacific is expected to register the highest CAGR during the forecast period. As increasing R&D expenditure helps in the development of new treatment solutions, supportive government policies for stem cell research and increasing public-private initiatives to encourage public adoption of stem cell-based treatment in the Asia Pacific countries are driving the growth of the market in this region. Global Key Leaders: Some of the major players operating in the cell harvesting market are PerkinElmer (US), Brandel (US), TOMTEC (US), Cox Scientific (UK), Connectorate (Switzerland), Scinomix (US), ADSTEC (Japan), and Terumo BCT (a part of Terumo Corporation) (Japan).  According to the new market research report “Pen Needles Market by Type (Standard Pen Needles, Safety Pen Needles), Length (4mm, 5mm, 6mm, 8mm, 10mm, 12mm), Therapy (Insulin, GLP 1, Growth Hormone), and Mode of Purchase (Retail, Non-Retail) – Global Forecast to 2026″, published by MarketsandMarkets™, the global market is expected to reach USD 2.2 Billion by 2026 from an estimated USD 1.3 Billion in 2021, at a CAGR of 11.2%.

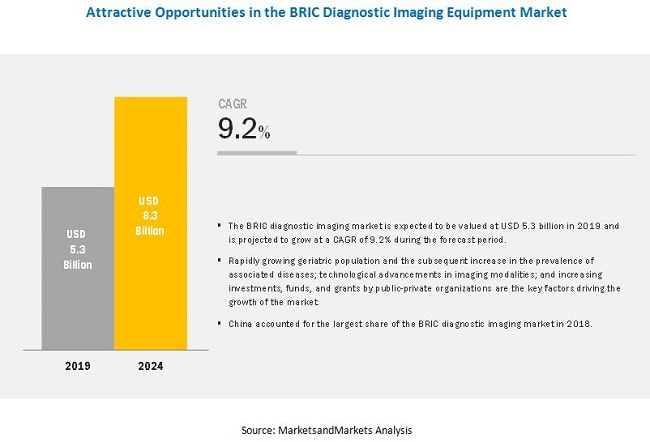

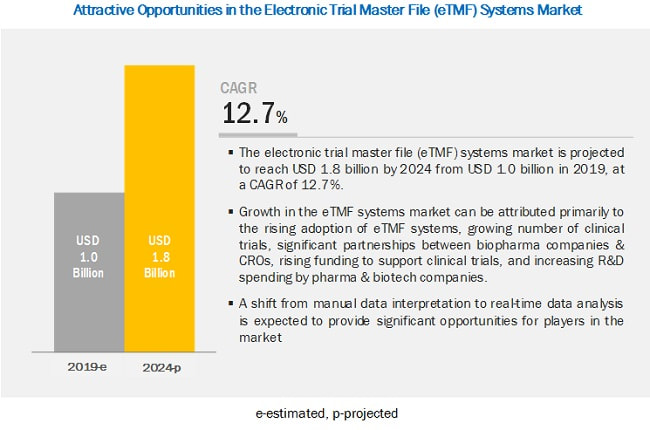

Browse in-depth TOC on “Pen Needles Market” 185 – Tables 56 – Figures 223 – Pages Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=75948613 The Growth in the market is largely driven by the growing prevalence of chronic diseases and the favorable reimbursement scenario in selected countries. On the other hand, the preference for alternative modes of drug delivery, poor reimbursement in developing countries, and needle anxiety are expected to restrain the overall market growth. Misuse of insulin pens and reuse of pen needles are the challenges faced by the market. The growing preference for biosimilar drugs and emerging markets are areas of opportunity in the market. The Type 2 diabetes, hypertension, and CVD significantly increase the risk for hospitalization and death in COVID-19 patients. Hence, managing these comorbidities has gained more focus for patients with existing conditions and those at the highest risk of contracting these conditions. This awareness has increased among healthcare professionals and patients and supported the growth of the management devices market. Hypoglycemia and hyperglycemia are both predictors for adverse outcomes in hospitalized patients. Hence the adoption of insulin delivery devices has increased. Pen needles are used in great quantities in diabetes management. So these would naturally be impacted by any change in overall product and service demand. The safety pen needles segment holds the highest CAGR during the forecast period. Based on type, the pen needles market is segmented into standard and safety pen needles. Safety pen needles are seen to be growing at the highest CAGR. Due to the rising awareness regarding the risks associated with blood-borne pathogen transmission, needle safety has become an issue of concern for hospitals, doctors, and patients, thus spurring the demand for safe needles. The 8mm segment is expected to account for the largest share of the pen needles market Based on length, the market is segmented into 4mm (5/32”), 5mm (3/16”), 6mm (1/4”), 8mm (5/16”), 10mm, and 12mm (1/2”). In 2020, the 8mm segment accounted for the largest share in the standard pen needles market. The large share of this segment is mainly attributed to the wide adoption of these needles among diabetes patients. The retail segment is expected to grow at the highest rate during the forecast period Based on the mode of purchase, the market is categorized into retail and non-retail. The retail segment accounted for the largest share during the forecast period. The significant discounts offered on online/retail purchases of pen needles, high convenience, increasing awareness on pen needles, and the favorable reimbursement scenario in North America and Europe are some of the key factors driving the growth of the retail segment. The therapy segment, insulin therapy is expected to grow at the highest CAGR in the market Based on therapy, the pen needles market is categorized into insulin therapy, glucagon-like peptide-1 (GLP-1) therapy, growth hormone therapy, and other therapies. In 2020, insulin therapy held maximum of the global market, primarily due to the high and growing diabetic population globally. This segment is also expected to grow at the highest rate during the forecast period. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=75948613 North America is expected to account for the highest share for players operating in the market Geographically, the pen needles market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Asia Pacific accounted for the highest growth of the market in 2020. The medical industry in the region has grown significantly over the years, and manufacturers are beginning to focus on providing well-established technologies to ensure sustainable and strong future revenue growth. Being a high-growth market, many manufacturers are also extending their global manufacturing bases to the APAC. With the low-cost manufacturing advantage, China and India are regarded as the most profitable manufacturing and R&D locations by most manufacturers. The rising demand for healthcare, driven by the rapid growth in the aging population, the growing prevalence of diabetes and other chronic diseases, drive market growth. Prominent players in the pen needles market include Becton, Dickinson and Company (US), Novo Nordisk A/S (Denmark), Ypsomed Holding AG (Switzerland), B. Braun Melsungen AG (Germany), Owen Mumford (UK), Terumo Corporation (Japan), Nipro Corporation (Japan) Allison Medical (US), AdvaCare Pharma (US), Berpu Medical Technology (China), ARKRAY (Japan), GlucoRx (UK), HTL-STREFA (Poland), UltiMed, (US), Hindustan Syringes and Medical Devices (India), Artsana Group (Italy), PromiseMed Diabetes Care (Canada), Montmed (Canada), Trividia Health (US), VOGT Medical Vertrieb (Germany), Van Heek Medical (Netherlands), Simple Diagnostics (US), Iyon (Turkey), Links Medical Products (US), and MHC Medical Products (US).  The report “BRIC Diagnostic Imaging Equipment Market by Modality ((X-Ray Imaging (Digital, Analog), MRI (High & Low Field), CT (Conventional, CBCT), Nuclear Imaging (SPECT, Hybrid PET)), End User (Hospitals, Imaging Centers) – Global Forecast to 2024″, is Diagnostic Imaging Equipment Market projected to reach USD 8.3 billion by 2024 from USD 5.3 billion in 2019, at a CAGR of 9.2% from 2019 to 2024. The Rapidly growing geriatric population coupled with the subsequent increase in the prevalence of associated diseases and increasing demand for early disease diagnosis are some of the key factors fueling market growth. Moreover, technological advancements in diagnostic imaging modalities and increasing investments, funds, and grants by public-private organizations are anticipated to further drive the growth of the diagnostic imaging market in BRIC countries. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=242 Hospitals were the largest end-user segment in the market in 2018; On the basis of end users, the hospitals segment commanded the largest share of the BRIC diagnostic imaging equipment market in 2018. The large share of this segment can be attributed to the rising number of diagnostic imaging procedures performed in hospitals, growing inclination toward the automation and digitization of radiology patient workflow, and increasing adoption of minimally invasive procedures. Geographical View in-detailed: On the basis of countries, segmented into Brazil, Russia, India, and China. China accounted for the largest share of the BRIC diagnostic imaging equipment market in 2018, followed by India. China has a dynamic and fast-growing healthcare industry with significant government emphasis on the modernization and expansion of the rural healthcare infrastructure. Moreover, rising geriatric population and associated diseases, easy accessibility to diagnostic imaging modalities, and rising adoption of advanced modalities are the key factors fueling the growth of the Chinese market. Global Key Leaders: The major players in the market include GE Healthcare (US), Siemens Healthineers (Germany), Koninklijke Philips N.V. (Netherlands), Canon Medical Systems Corporation (Japan), Carestream Health, Inc. (US), Hologic, Inc. (US), Hitachi, Ltd. (Japan), Neusoft Corporation (China), Allengers (India), CURA Healthcare (India), NP JSC Amico (Russia), SONTU Medical Imaging Equipment Co., Ltd. (China), FUJIFILM Holdings Corporation (Japan), and United Imaging Healthcare Co, Ltd. (China), among others. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=242 Koninklijke Philips N.V. (Netherlands) held the major share of the BRIC diagnostic imaging equipment market in 2018. As part of its strategy, Philips focuses on product launches and expansions to increase its market share in this highly competitive market. China offers significant opportunities for Philips due to its large patient pool and developing healthcare infrastructure. In order to deliver technologically advanced solutions at economical prices, the company established an AI lab in Shanghai, China. The company has also entered into partnerships & collaborations with various companies and organizations in the country to enhance its market share. Siemens Healthineers (Germany) held the second position in the BRIC diagnostic imaging equipment market in 2018. The company has a significant presence in BRIC nations and offers a number of modalities in the diagnostic imaging market. With a robust product portfolio, Siemens Healthineers holds a strong position in the diagnostic imaging market. To maintain its competitive position, the company focuses on new product launches and expansions as key organic growth strategies. In 2018, the company introduced the Mammomat Revelation Mammography System and NX Series Ultrasound machines in India. These developments have helped the company to expand its customer base and strengthen its geographical footprint across the globe. Siemens is considered as one of the key players in the global market due to its vast product portfolio and strong distribution channels. Moreover, the company invested around USD 6.6 billion, USD 5.7 billion, and USD 5.3 billion in R&D during 2018, 2017, and 2016, respectively.  The study involved four major activities in estimating the current size of the Electronic Trial Master File (eTMF) Systems Market. Exhaustive secondary research was done to collect information on the market and its different subsegments. The next step was to validate these findings, assumptions, and sizing with industry experts across the value chain through primary research. Both top-down and bottom-up approaches were employed to estimate the complete market size. After that, market breakdown and data triangulation procedures were used to estimate the market size of segments and sub-segments. The report “Electronic Trial Master File (eTMF) Systems Market by Component (Services, Software), End-User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations), Delivery Mode (On-Premise, Cloud-Based), and Region – Global Forecast to 2024″, the eTMF systems market is projected to reach USD 1.8 billion by 2024 from USD 1.0 billion in 2019, at a CAGR of 12.7%. The Growth in the Electronic Trial Master File Systems Market can be attributed primarily to the rising adoption of eTMF systems, rising number of clinical trials, partnerships between biopharma companies & CROs, increasing funding to support clinical trials, and the growth in the R&D spending by pharma & biotech companies. Emerging countries are expected to provide significant opportunities for players in the market. However, budget constraints, data privacy issues, and a dearth of skilled professionals will challenge market growth in the coming years Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=94357456 Market Segmentation in Detailed: Based on delivery mode, segmented into on-premise and cloud-based eTMF. In 2018, the cloud-based eTMF segment accounted for the largest share of the market. The large share of this segment is primarily due to the flexible, scalable, and affordable nature of this delivery mode. Based on end-user, the eTMF systems market is segmented into pharmaceutical & biotechnology companies, contract research organizations (CROs), and other end-users (medical device companies, academic research institutes, and consulting service companies). The pharmaceutical & biotechnology companies segment accounted for the largest market share in 2018. The increasing applications of eTMF software in clinical project management and the availability of substantial R&D budgets with large pharmaceutical & biotechnology companies will drive the adoption of eTMF systems in this end-user segment. Based on the component, the market is segmented into services and software. The services segment accounted for the largest market share in 2018. The large share of this segment can be attributed to their indispensable nature and repetitive requirement. End-users of eTMF systems rely heavily on service providers for consulting, data storage, implementing services, training, maintenance, and regular upgrades of solutions. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=94357456 North America dominated the eTMF systems market in 2018; this trend to continue during the forecast period Geographically, the Electronic Trial Master File Systems Market is divided into North America, Europe, Asia Pacific, and the Rest of the World (RoW). The North American market accounted for the largest share of the market in 2018, primarily due to the increasing government funding for clinical research and a large number of clinical trials. Several major global players are also based in the US, owing to which the country has become a center of innovation in the Electronic Trial Master File (eTMF) Systems Market. Veeva Systems (US), Oracle Corporation (US), Phlexglobal Limited (UK), TransPerfect Global Inc. (US), Aurea Software (US), LabCorp (US), ePharmaSolutions (US), Wingspan Technology, Inc. (US), MasterControl (US), SureClinical, Inc. (US), Dell EMC (US), Paragon Solutions (US), PharmaVigilant (US), Mayo Clinic (US), Database Integrations, Inc. (US), CareLex (US), Ennov (France), Forte Research (US), Freyr (US), Montrium (US), NCGS Inc. (US), SAFE-BioPharma (US), SterlingBio Inc. (US), BIOVIA Corp. (US), and arivis AG (Germany) are the key players in the eTMF systems market. |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed