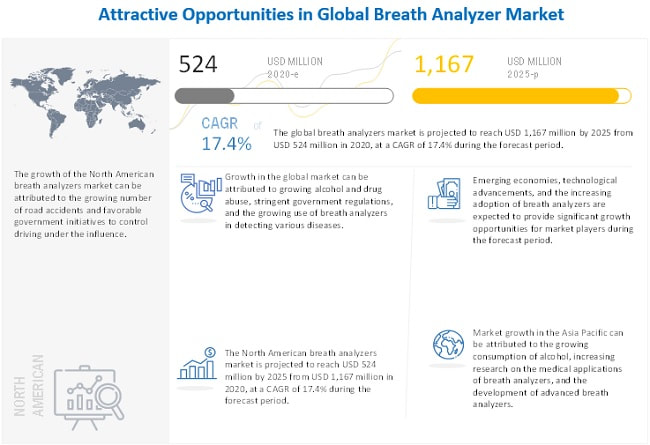

According to the new market research report “Breath Analyzer Market by Technology (Fuel Cell, Semicoductor Oxide Sensor, Others), End User (Law Enforcement Agencies, Enterprises, Individuals ), Application, Region (North America, Europe, APAC, RoW) – Global Forecast to 2025″, published by MarketsandMarkets™, the breathalyzers market is expected to reach USD 1,167 million by 2025 from USD 524 million in 2020, at a CAGR of 17.4% during the forecast period. Opportunities: Technological advancements; The breath analyzers market is technology-driven and is projected to grow at a significant rate in the coming years. Owing to the lucrative potential of the market, a number of players are focusing on developing novel technologies and are continuously introducing accurate and easy-to-use breath analyzers. In August 2019, Y Combinator, an investment company, invested in SannTek Labs to work on a new kind of breathalyzer. This breathalyzer is designed to detect blood alcohol levels as well as the type of cannabis a person has consumed in the past 3 to 4 hours. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=57484012 The Growth in the market can primarily be attributed to factors such as alcohol and drug abuse, stringent government regulations and increasing use of breath alyzers in detecting various diseases. By technology, the fuel cell segment is expected to account for the largest share of the market in 2020 Based on technology, the breath analyzers market is segmented into fuel cells, semiconductor oxide sensors, and other technologies (infrared spectroscopy and chemical crystals). In 2020, the fuel cells segment accounted for the largest share of the global market. Fuel cells are the most widely used technology in breath analyzers. Fuel cell-based breath analyzers offer an extremely high level of accuracy, sensitivity, and reliability. They are specifically tuned to detect alcohol and do not require multiple sensors. These analyzers are considered the gold standard of handheld alcohol testers for both personal and professional use. By application, the alcohol detection segment is expected to account for the largest share of the market in 2020 On the basis of application, the breath analyzers market is segmented into alcohol detection, drug abuse detection, and medical applications. The alcohol detection segment accounted for the largest market share in 2020. This segment is also projected to register the highest CAGR during the forecast period. The growth of this segment is primarily driven by stringent government regulations for driving under the influence (DUI). By end user, the law enforcement agencies segment is expected to account for the largest share of the breath analyzer market in 2020 Based on end users, the breathalyzers market segmented into law enforcement agencies, enterprises, and individuals. In 2020, the law enforcement agencies segment accounted for the largest share of the global market. Stringent safety laws against DUI and the rising scale of screening and evidential testing are driving the adoption of breath analyzers in law enforcement. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=57484012 Asia-Pacific to witness the highest growth rate in 2020 Based on region, the breath analyzer market is segmented into North America, Asia-Pacific, Europe and Rest of the world (RoW). Asia Pacific is expected to register the highest CAGR during the forecast period. The major factors driving the growth of the Asia Pacific market include as growing consumption of alcohol, increasing research on the medical applications of breath analyzers, and the development of advanced breath analyzers. The prominent players in the global breath analyzer market include Drägerwerk AG & Co. KGaA (Germany), MPD, Inc (US), Lifeloc Technologies (US), BACtrack, Inc. (US), Quest Products, Inc. (US), Akers Biosciences, Inc. (US), Intoximeter, Inc. (US), AK GlobalTech Corporation (US), Alcohol Countermeasure Systems Corporation (Canada), EnviteC-Wismar GmbH (Germany), Lion Laboratories Ltd. (UK) Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=57484012

0 Comments

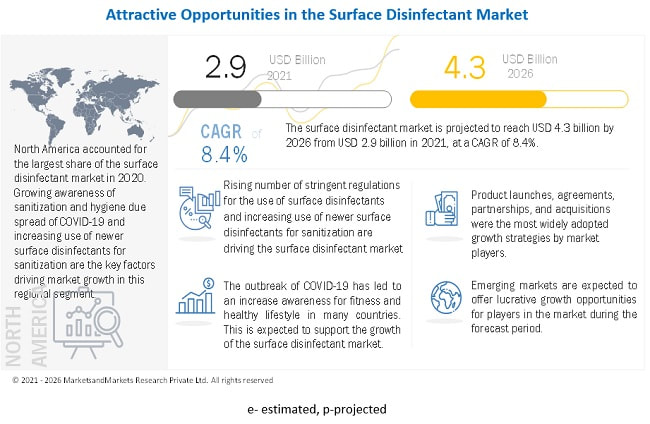

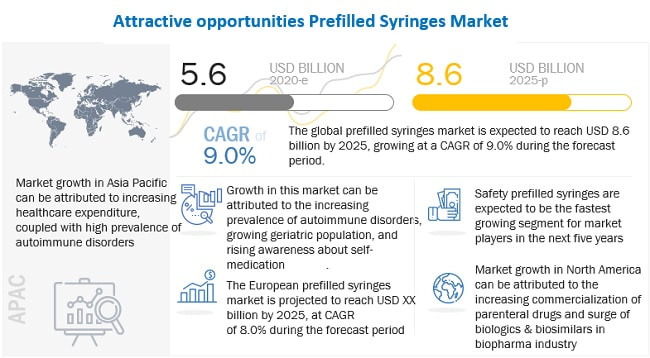

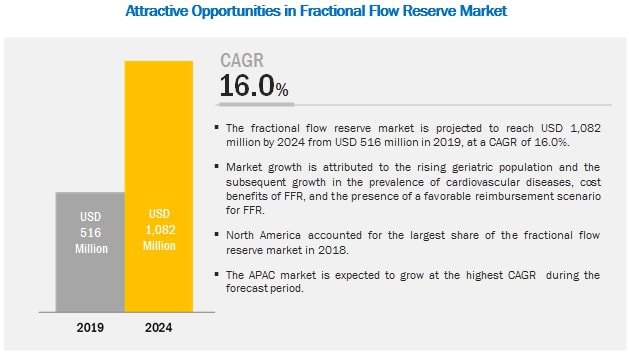

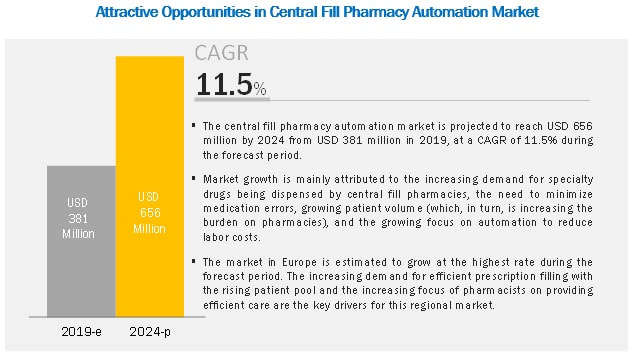

According to the new market research report “Surface Disinfectant Market by Composition (Quaternary Ammonium, Alcohols, Chlorine, Hydrogen Peroxide), Type (Liquids, Sprays, Wipes), Application (Surface, Instrument), End User (Hospitals, Diagnostic and Research Labs) – Global Forecast to 2025″, published by MarketsandMarkets™, is projected to reach USD 3.6 billion by 2025 from USD 3.1 billion in 2020, at a CAGR of 3.0% from 2020 to 2025. Driver: Rising number of stringent regulations for the use of surface disinfectants; Rising number of stringent regulations focus on the development of suitable policies for housekeeping services, which puts a premium on good housekeeping and sanitation. Such regulatory guidelines will help in improving the regular usage of surface disinfectants across healthcare settings. Opportunity: Increasing healthcare expenditure and focus in emerging economies; Emerging economies, such as India, Brazil, and South Africa, provide significant opportunities for players in the sterilization and disinfection markets. Emerging economies in the APAC region present lucrative investment opportunities for multinational infection control companies to offshore their business operations to these markets. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=2312860 The growth of this market is majorly driven by the increasing prevalence of hospital-acquired infections (HAIs) globally, presence of stringent regulations for the use of surface disinfectants (in hospitals, diagnostic laboratories, pharmaceutical & biotechnology companies, and research laboratories), and advancements in surface disinfectants. Alcohols segment accounted for the largest share of the surface disinfectants market. On the basis of composition, the market is segmented into alcohols, chlorine compounds, quaternary ammonium compounds, hydrogen peroxide, peracetic acid, and other compositions. In 2019, the alcohols segment accounted for the largest market share. The high use of alcohols on hard surfaces in hospitals and laboratories is driving the growth of this segment. Other segments, such as hydrogen peroxide and peracetic acid are expected to have higher growth rates due to their growing acceptance in surface disinfectant formulations. Liquids segment accounted for the largest share of the of the surface disinfectants market. On the basis of type, the market is segmented into liquids, wipes, and sprays. The liquids segment accounted for the largest market share in 2019. This can primarily be attributed to the wide usage of these disinfectants, especially in emerging and underdeveloped countries, due to their low cost. The hospital settings segment is expected to dominate the market in 2020. By end user, the surface disinfectants market is segmented into hospital settings, diagnostic laboratories, pharmaceutical & biotechnology companies, and research laboratories. In 2019, hospital settings accounted for the largest share of the market. The large share of this segment can be attributed to factors, such as the high prevalence of infections in hospitals, the increase in hospital reimbursements for surgeries performed in hospitals, and growing patient volume in these healthcare settings. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=231286043 The surface disinfection segment dominated the market in 2019. The surface disinfectants market, by application, is segmented into surface disinfection, instrument disinfection, and other applications. In 2019, the surface disinfection segment accounted for the largest share of the market. The large share of this segment can primarily be attributed to the large volume of disinfectants required to clean in-house surfaces in healthcare settings. Based on region, the surface disinfectant market is segmented into North America, Europe, the Asia Pacific, Latin America, and the Middle East and Africa. In 2019, North America commanded the largest share of the market. The large share of this market segment can be attributed majorly to the high prevalence of HAIs and the presence of stringent infection control regulations in the region. The major players operating in this surface disinfectant market are 3M Group (US), Cantel Medical Corporation (US), The Clorox Company (US), Ecolab Inc. (US), Procter & Gamble (US), Reckitt Benckiser Group plc. (UK), Diversey, Inc. (US), STERIS plc (US), CarrollCLEAN (US), Metrex Research, LLC. (US), Whiteley Corporation (Australia), GOJO Industries, Inc. (US), PAUL HARTMANN AG (Germany), Medline Industries, Inc. (US), Pharmax Limited (Canada), PDI Inc. (US), Betco (US), GESCO Healthcare Pvt. Ltd. (India), MEDALKAN (Greece), Ruhof (US), Contec Inc. (US), Cetylite, Inc. (US), Micro-Scientific, LLC (US), Pal International (UK), and BHC, Inc. (US). Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=231286043  According to the new market research report “Prefilled Syringes Market by Type [Conventional (Disposable, Reusable), Safety], Material (Glass, Plastic), Design (Single-Chamber, Dual-Chamber, Customized), Application (Diabetes, Cancer, Arthritis, Anaphylaxis, Ophthalmology) – Global Forecast to 2025″, published by MarketsandMarkets™, is estimated to be USD 5.6 billion in 2020 and projected to reach USD 8.6 billion by 2025, at a CAGR of 9.0%. Opportunity: Growing healthcare infrastructure across emerging markets; Emerging countries continue to suffer from insufficient healthcare funding, which adversely affects access to healthcare, quality, and, ultimately, the health status of citizens. According to the World Bank, approximately 400 million people lack access to essential healthcare services, mostly in Africa and South Asia. Furthermore, accelerating medical inflation, i.e., the cost of medical treatments and a higher prevalence of non-communicable lifestyle-related diseases such as cancer, diabetes, or cardiac syndromes, have resulted in funding gaps. According to a report published by Geneva Association, in the last two decades, the share of total aggregate global expenditure on healthcare in GDP has increased from about 8% to almost 10%, or an estimated USD 8 trillion per annum, which is driven by the accelerating cost of medical treatment, expanding treatment options and increasing customer demands. Moreover, the Global Burden of Disease Health Financing Collaborator Network (2017) estimates that global spending on health will almost triple to USD 24 trillion by 2040 with upper-middle-income countries are estimated to show the fastest increase at an average of 5.3% per year. This growth could be attributed to continued growth in GDP and the rise of the middle class and government spending. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=16618331 The Rising target disease population, rapid growth in generic products, rising adoption of self-medication and digitalization, affordable cost with increased efficiency, and technological advancements are the major factors driving the growth of the market. Furthermore, growing initiatives undertaken by leading market players to establish production facilities in both mature and developing markets are the key factors driving the growth of the prefilled syringes industry. The Prefilled Syringes Market includes major Tier I and II suppliers like Becton, Dickinson and Company (US), Gerresheimer (Germany), SCHOTT AG (Germany), and West Pharmaceutical Services, Inc. (US), and Nipro Corporation (Japan). These suppliers have their manufacturing facilities spread across regions such as North America and Europe. COVID-19 has impacted their businesses as well. Routine care for chronic diseases is an ongoing challenge amidst the global COVID-19 pandemic due to the change in routine care to virtual communication. Diabetes, chronic obstructive pulmonary disease, and hypertension were the most impacted conditions due to a reduction in access to care. Furthermore, currently, most global healthcare resources are focused on coronavirus disease (COVID-19), and this resource reallocation is expected to disrupt the continuum of care for patients with chronic diseases. Increasing adoption of self-administered injectable drugs is expected to result in the segment occupying the majority of the market share The conventional Prefilled Syringes Market is estimated to have the largest market share by value. Growth of this segment can be attributed to the the advantages offered, such as safe administration, ease of use for both healthcare professionals and end users, reduced risk of contamination of the product, less waste of costly API, ease of manufacturing, improved dosing accuracy, and enhanced product differentiation when compared to vials is expected to drive the market growth. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=16618331 Plastic Prefilled Syringes estimated to be the fastest-growing market Plastic prefilled syringes are estimated to be the fastest-growing segment in the Prefilled Syringes Market. The growth of this segment can be attributed to the rising development of newer polymers (which possess various physical and chemical properties such as high heat & break resistance, tolerance of freeze-drying & liquid nitrogen exposure, high transparency, and solvent resistance. Europe is estimated to be the largest market due to the rising prevalence of chronic diseases, growth of the biologics and biosimilars market, technological advancements, geographical expansion by key manufacturers, aging population, and high adoption of self-injection devices are driving the demand for self-injectable prefilled syringes. Asia Pacific likely to emerge as the largest Prefilled Syringes Market. Asia Pacific is estimated to be the fastest-growing market for prefilled syringes during the forecast period. The Asia Pacific market is driven principally by the increasing demand for self-administered treatments, high penetration of self-injection devices, growing aging population, increasing prevalence of diabetes, and huge patient population. Becton, Dickinson and Company (US), Gerresheimer (Germany), SCHOTT AG (Germany), and West Pharmaceutical Services, Inc. (US) are the key players in the global Prefilled Syringes Market Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=16618331  The report "Fractional Flow Reserve Market by Technology (Invasive Monitoring, Non-invasive Monitoring), Invasive Monitoring Product (Pressure Guidewires, FFR Measurement Systems), Application, and Region - Global Forecast to 2024", is projected to reach USD 1,081.8 million by 2024 from USD 516 million in 2019, at a CAGR of 16.0% during the forecast period. Driver: Rising geriatric population and the subsequent growth in the prevalence of CVD; Over the years, there has been a significant increase in the geriatric population across the globe. According to the UN World Population Ageing Report 2017, the global geriatric population (aged 60 years and above) is expected to reach 2.1 billion by 2050 from 962 million in 2017. As this population segment is highly susceptible to CVD and other target diseases, the demand for advanced diagnostic and treatment options is expected to increase in the coming years. Changing lifestyle, smoking, hypertension, high blood cholesterol levels, physical inactivity, high BMI, and high blood sugar levels are the leading risk factors for heart disease and stroke. With the rising prevalence of CVD, the number of related diagnostic and treatment procedures is expected to increase significantly across the globe in the coming years. In this scenario, the demand for fractional flow reserve is likely to increase as it provides various benefits, such as assessing if the stenosis is required, which in turn helps in avoiding surgeries (in cases where stenosis is not needed). Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=257837023 Leading Key Players and Analysis: The key players in the fractional flow reserve market are Abbott (US), Boston Scientific (US), ACIST Medical Systems (US), Koninklijke Philips N.V. (Netherlands), Opsens, Inc. (Canada), HeartFlow, Inc. (US), Siemens Healthineers (Germany), Pie Medical Imaging (Netherlands), CathWorks (Israel), and Medis Medical Imaging Systems BV (Netherlands). Abbott (US) held the leading position in the fractional flow reserve market. The company acquired a significant share in the FFR market through the acquisition of St. Jude Medical (US). This acquisition positioned Abbott as a major cardiology devices provider. The strategic acquisition of St. Jude Medical, a leading player in the cardiovascular and neuromodulation products market, strengthened the position of Abbott in the fractional flow reserve (FFR) market. Abbott focuses on continuous expansions to achieve optimal growth across industries and different geographic areas. It strives to maintain its position through innovation and product launches. For instance, the company invests a significant amount of its revenue in R&D activities to increase its presence in the market. It invested USD 2.30 billion, USD 2.26 billion, and USD 1.42 billion on R&D in 2018, 2017, and 2016, respectively Geographical Analysis in Detailed? Asia Pacific to register the highest CAGR during the forecast period North America dominated the FFR Market in 2018. The large share of the North American fractional flow reserve market can primarily be attributed to the high healthcare spending in the region, rising prevalence of CVD and lifestyle diseases, growth in the geriatric population, large number of ongoing research activities and product launches, availability of reimbursements, and the rapid adoption of technologically advanced imaging systems. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=257837023 Industry Segmentation: The invasive monitoring segment to account for the largest market share during the forecast period Based on technology, the fractional flow reserve market is segmented into invasive and non-invasive monitoring. The invasive monitoring segment accounted for the largest share of the market in 2018 and will continue to do so during the forecast period. Invasive FFR monitoring is considered the gold standard for determining the hemodynamic impact of coronary lesions. This technology utilizes pressure guidewires and monitoring systems for the measurement of fractional flow reserve. The pressure guidewire measures the flow and pressure of the blood before and after the blockage to produce a ratio. The single-vessel diseases segment will dominate the market during the forecast period. Based on application, the FFR Market is segmented into single-vessel diseases and multi-vessel diseases. In 2018, the single-vessel disease segment accounted for the larger share of the fractional flow reserve market. The large share of this segment can be attributed to the high prevalence of single-vessel coronary artery disease. The pressure guidewires segment is expected to grow at the highest CAGR during the forecast period On the basis of product, the invasive monitoring market is segmented into pressure guidewires and FFR monitoring systems. The pressure guidewires segment accounted for the largest share of the market in 2018. This can be attributed to the growth in the number of PCI procedures (as a result of the rising prevalence of CVD), strong recommendation for the use of guided revascularization by measuring FFR in specific clinical scenarios, and the single-use nature of pressure guidewires, which ensures repeat purchases. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=257837023 Central Fill Pharmacy Automation Market - Global Industry Leaders & Growth Strategies Adopted3/23/2022  According to the new market research report “Central Fill Pharmacy Automation Market by Product (Equipment (Medication Dispensing System, Automated Medication Compounding Systems, Workflow Management), Service (Process Optimization, Facility Design), Software), Vendor – Global Forecast to 2024″, published by MarketsandMarkets™, the Pharmacy Automation Market is projected to reach USD 656 million by 2024 from USD 381 million in 2019, at a CAGR of 11.5%. Recent Developments; - In 2018, TCGRx acquired Parata Systems, to expand the company’s existing growth initiatives with central fill, inventory control, and automated blister card packaging technologies. - In 2018, ARxIUM, Inc., launched cGMP RIVA IV Compounding system for 503B facilities. - In 2018, Swisslog Healthcare acquired Talyst Systems, LLC. With the aim of expanding Swisslog’s inpatient and outpatient pharmacy solutions along with the company’s field service network. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=87188549 The increasing demand for specialty drugs being dispensed by central fill pharmacies is one of the primary drivers propelling the growth of this market. Other factors such as the need to minimize medication errors, growing patient volume (which in turn is increasing the burden on pharmacies), and the growing focus on automation to reduce labor costs are also driving market growth. The equipment segment is expected to account for the largest share of the pharmacy automation market The central fill pharmacy automation market, by product and service, is segmented into equipment, services, and software. The equipment segment accounted for the largest market share in 2018. A number of automated systems are used in facilities offering the advantages of freeing up manpower, allowing greater throughput, and increasing the number of processed prescriptions. These facilities form an indispensable tool for central fill pharmacies to improve the prescription assembly, verification, and delivery back to the pharmacy. This contributes to the large share of the segment. The equipment vendors are increasing with the increasing demand for automation systems Based on vendor, the central fill pharmacy automation market is segmented into equipment vendors and consulting vendors. The equipment vendors segment is estimated to account for the largest market share in 2018. This is mainly attributed to their broad product portfolio, vast geographic presence, strong technical expertise, and easy access to spare parts (resulting in reduced downtime). Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=87188549 North America is expected to dominate the pharmacy automation market during the forecast period In 2018, North America dominated the central fill pharmacy automation market, followed by Europe, and this trend is expected to continue during the forecast period. The rising focus on providing value-based care to patients, increase in specialty medication dispensing, growing number of medication errors, and the need for automated systems for improved compounding and dispensing are major factors that have resulted in the increased adoption of central fill pharmacy automation equipment and services in North America. Prominent players in the central fill pharmacy automation market are ARxIUM, Inc. (US), RxSafe, LLC (US), TCGRX Pharmacy Workflow Solutions (US), McKesson Corporation (US), Omnicell, Inc. (US), ScriptPro (US), Kuka AG (Germany), Innovation (US), R/X Automation Solutions (US), Tension Packaging & Automation (US), Cornerstone Automation Systems, LLC (CASI, US), and QMSI (US) Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=87188549 According to the new market research report “Therapeutic Drug Monitoring Market by Product (Equipment (Immunoassay Analyzers), Consumables), Technology (Immunoassays, Chromatography-MS), Class of Drugs (Antibiotic Drugs, Bronchodilator Drugs), End User – Global Forecast to 2025″, published by MarketsandMarkets™, the TDM Market is projected to reach USD 2.0 billion by 2025 from USD 1.4 billion in 2020, at a CAGR of 6.9% from 2020 to 2025.

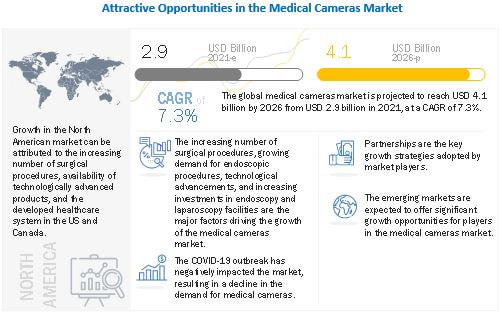

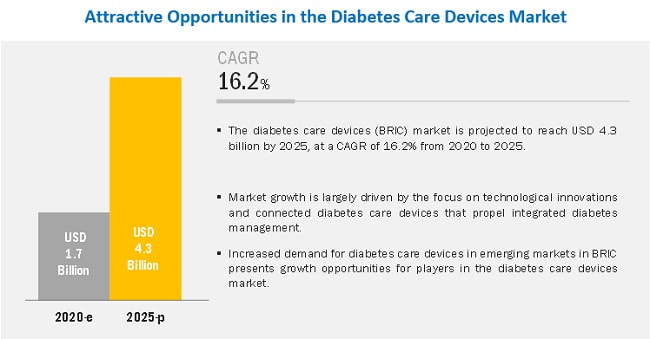

Driver: Increasing preference for precision medicine; Precision medicine is an evolving approach for disease treatment and prevention that considers individual variability in genes, environments, and lifestyles. Precision medicine involves selecting drugs wholly tailored to a patient based on disease condition and history. Although this practice is expanding into all disease areas, oncology has seen the most progress. Currently, cancer patients are being provided treatment through combination drugs, based on studies conducted on the patient’s parameters such as systems biology, analysis of the tumor, and gene expression data in the absence and presence of pharmacological perturbation. This approach, which is currently being tested in various settings, aims to revolutionize pharmacotherapy in oncology and other disease areas. TDM can be of immense value to advance this novel way of treating patients. Studies also reveal that drug therapies for major diseases benefit only 30–50% of patients, while nearly 7% of hospitalized patients experience adverse drug reactions. The personalization of drug therapy explores the patients’ response to drugs to maximize effects while minimizing the risk of adverse reactions due to toxicity or sub-therapeutic dosing. TDM has been proposed to adjust the drug dosage individually based on the pharmacokinetic profile obtained. At present, over 20 drugs are routinely monitored. The promising benefits offered by precision medicine are expected to propel the demand for TDM in this application. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=155350443 The TDM Market growth is largely driven by factors such as the rising number of organ transplant procedures, the use of TDM across various therapeutic fields, the increasing preference for precision medicine, a growing focus on R&D related to TDM, and technological advancements in immunoassay instruments. Increasing adoption in the treatment of autoimmune diseases is expected to provide a wide range of growth opportunities for players in the market. Consumables is expected to hold the largest share of the therapeutic drug monitoring market in 2020 On the basis of product, the market is segmented into equipment and consumables. In 2019, consumables segment accounted for the largest market share, primarily due to the repeat purchases of kits and reagents and the increasing number of immunoassay tests being performed across the globe. Immunoassays is expected to hold the largest share of the TDM Market in 2020 Based on technology, segmented into immunoassays and chromatography-MS. In 2019, immunoassays segment accounted for the largest market share, due to the increasing incidence of chronic and infectious diseases and technological innovation. Antiepileptic drugs is expected to hold the largest share of the therapeutic drug monitoring market in 2020 On the basis of class of drug, the market is segmented into antiepileptic drugs, antibiotic drugs, immunosuppressant drugs, antiarrhythmic drugs, bronchodilator drugs, psychoactive agents, and other drugs. During 2019, antiepileptic drugs held the largest share among the class of drug due to the high complexity and heterogeneity of epilepsy, lack of biological markers or specific clinical signs aside from the frequency of seizures to assess treatment efficacy or toxicity, and the highly complex pharmacokinetics of these drugs. Hospital laboratories segment commanded the largest share of the TDM Market in 2019 By end user, the market is segmented into hospital laboratories, commercial & private laboratories, and other end users. Hospital laboratories accounted for the largest share of the market in 2019. The large share of this segment can be attributed to factors such as the availability of advanced healthcare facilities in hospitals and the rising incidences of chronic diseases. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=155350443 North America commanded the largest share of the therapeutic drug monitoring market in 2019. On the basis of region, the market is segmented into North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. In 2019, North America commanded the largest share of the market. Increasing per capita healthcare expenditure and the presence of technologically advanced healthcare infrastructure in the region, coupled with initiatives taken by different government associations, are anticipated to boost the market growth in the region. The major players operating in this therapeutic drug monitoring market are Abbott Laboratories (U.S.), F. Hoffmann-La Roche (Switzerland), Siemens Healthineers (Germany), Thermo Fisher Scientific (U.S.), Danaher Corporation (U.S.), Bio-Rad Laboratories (U.S.), bioMérieux (France), BÜHLMANN Laboratories (Switzerland), SEKISUI MEDICAL (Japan), Randox Laboratories (Ireland), DiaSystem Scandinavia AB (Sweden), Cambridge Life Sciences Limited (United Kingdom), ARK Diagnostics, Inc. (U.S.), Chromsystems Instruments & Chemicals GmbH (Germany), Grifols (Spain), Exagen Inc. (U.S.), Theradiag (France), R-Biopharm AG (Germany), apDia Group (Belgium), BioTeZ Berlin-Buch GmbH (Belgium), Eagle Biosciences Inc. (U.S.), JASEM Laboratory Systems and Solutions A.S (Turkey), Aalto Scientific (U.S.), Immundiagnostik AG (Germany), and UTAK (U.S.) Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=155350443  According to the new market research report “Medical Cameras Market by Camera Type (Endoscopy Cameras, Ophthalmology Cameras, Dermatology Cameras), Resolution (HD Cameras, SD Cameras), Sensor (CMOS, CCD), End-Users (Hospitals & Ambulatory Surgery Centers, Specialty Clinics) – Global Forecast to 2026″, published by MarketsandMarkets™, is projected to reach USD 4.1 billion by 2026 from USD 2.9 billion in 2021, at a CAGR of 7.3% during the forecast period. Driver: The increasing number of surgical procedures; An increasing number of surgical procedures require medical cameras, which has considerably grown in recent years. The growing number of surgeries can be attributed to the rapidly growing geriatric population worldwide and the increasing prevalence of chronic diseases, leading to the increasing demand for medical equipment. Many countries across the world are facing the challenge of increasing senior populations. According to the United Nations (UN), in 2019, there were 703 million persons aged 65 years or over in the world. The senior population is estimated to double to 1.5 billion in 2050. Non-invasive surgeries (mainly using endoscopy and microscopy surgery cameras) are preferred for older people due to lesser complications than conventional surgeries. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=201071746 The growth is largely driven by the increasing number of surgical procedures, growing demand for endoscopic procedures, technological advancements, and increasing investments in endoscopy and laparoscopy facilities. Endoscopy Cameras accounted for the larger share of the share of global medical cameras market in 2020. Based on type, the medical cameras market is segmented into surgical microscopy cameras, endoscopy cameras, dermatology cameras, ophthalmology cameras, dental cameras, and other medical cameras. The Endoscopy cameras segment accounted for the largest share of global medical camera market. This can be attributed to the increasing number of endoscopy procedures across the globe. The CMOS Sensor segment accounted for the largest market share in 2020. Based on sensor, the medical cameras market is segmented into CMOS Sensor and CCD Sensor. CMOS Sensors accounted for the largest share of the global market in 2020. This can be attributed various advantages of CMOS sensors over CCD sensors, such as low power consumption, ease of integration, and faster frame rate. Moreover, the cost of manufacturing these sensors is lower than that of CCD sensors. The High-definition cameras accounted for largest market share in 2020 Based on resolution, segmented into standard-definition (SD) cameras and high-definition (HD) cameras. High-definition cameras accounted for the largest share of the global market in 2020. The large share of this segment can primarily be attributed to the greater demand for HD cameras among end users due to the significant requirement of high-quality images in medical specialties. Hospitals & ambulatory surgery centers are the largest end-users of the medical cameras market Based on end users, segmented into hospitals & ambulatory surgery centers and specialty clinics. Hospitals & ambulatory surgery centers accounted for the largest share of the global medical camera market in 2020. This can be attributed to the increasing number of hospitals, especially in India, China, and Africa, and growing government & private investments to upgrade healthcare infrastructures. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=201071746 North America dominates the global medical cameras market The market is divided into five regions, namely, North America, Europe, Asia Pacific, and Rest of the World. North America dominated the global market. The large share of the North American region is mainly attributed to the technological advancements in medical cameras, implementation of favorable government initiatives, and rise in the number of surgical procedures. The major players in the medical cameras market are Olympus Corporation (Japan), Richard WOLF GmbH (Germany), TOPCON CORPORATION (Japan), Sony Corporation (Japan), Stryker Corporation (US), Danaher Corporation (US), Canon Inc. (Japan), Carl Zeiss AG (Germany), Smith & Nephew (UK), Carestream Dental LLC (US), and Basler AG (Germany) Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=201071746  According to the new market research report “Diabetes Care Devices Market by Type (SMBG, CGMS, Lancets, Insulin Pumps, Insulin Pens, Insulin Syringes, Mobile Apps), Patient Care Settings (Hospitals & Specialty Clinics, Self & Home Care), and Country (Brazil, Russia, India, China) – Forecast to 2025″, published by MarketsandMarkets™, the Diabetes Care Devices ((BRIC) Market size is projected to reach USD 4.3 billion by 2025 from USD 1.7 billion in 2020, at a CAGR of 16.2% during the forecast period. Recent Developments:

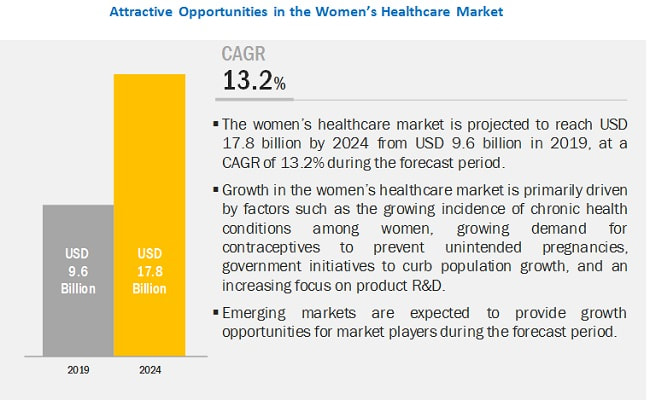

https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=375 Factors such as the increasing diabetic population, rising awareness of diabetes treatment and management, and favorable national health strategies are expected to drive the growth of the diabetes care devices (BRIC) market. The blood glucose monitoring systems segment is estimated to dominate the diabetes care devices market in 2020 Based on type, the diabetes care devices (BRIC) market has been segmented into blood glucose monitoring systems, insulin delivery devices, and diabetes management mobile applications. Under the blood glucose monitoring systems segment, the test strips segment is estimated to account for the largest share in 2020. The dominance of this segment can be attributed to the frequent requirement of test strips in blood glucose monitoring systems. Self/home healthcare is projected to witness the highest CAGR in the diabetes care devices (BRIC) market during the forecast period Based on end user, the diabetes care devices market has been segmented into hospitals & specialty clinics and self/home healthcare. The self/home healthcare segment is estimated to hold the largest share in 2020. This segment is also projected to grow at the highest CAGR during the forecast period. The rapid growth of the segment is attributed to the increasing awareness of diabetes self-monitoring and management, increasing recommendations from physicians for home healthcare for diabetes, and the increasing utility of home-based diabetes care devices to provide real-time insights regarding the condition due to the technological advancements of these systems. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=375 China to hold the largest share in the market in 2020, followed by India China is projected to hold the largest share in the diabetes care devices (BRIC) market during the forecast period. This can be attributed to the sharp increase in diabetes in the country, favorable national health strategies, and government-led endorsements of medical device companies. The prominent players in the diabetes care devices market include Medtronic plc (Ireland), B. Braun (Germany), DexCom, Inc. (US), Abbott (US), F. Hoffman-La Roche Ltd. (Switzerland), Ascensia Diabetes Care Holdings AS (Switzerland), LifeScan (US), AgaMatrix Holdings LLC (US), Acon Laboratories, Inc. (US), ARKRAY USA, Inc. (US), Novo Nordisk A/S (Denmark), Becton, Dickinson and Company (US), Sanofi (France), Terumo Corporation (Japan), SD Biosensor, Inc. (South Korea), MicroGene Diagnostic Systems Pvt. Ltd. (India), Ypsomed Holdings AG (Switzerland), Dr. Morepen (India), Sinocare, Inc. (China), Bionime Corporation (Taiwan), and Rossmax International Ltd. (Taiwan) Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=375 According to the new market research report “Prefilled Syringes Market by Type [Conventional (Disposable, Reusable), Safety], Material (Glass, Plastic), Design (Single-Chamber, Dual-Chamber, Customized), Application (Diabetes, Cancer, Arthritis, Anaphylaxis, Ophthalmology) – Global Forecast to 2025″, published by MarketsandMarkets™, is estimated to be USD 5.6 billion in 2020 and projected to reach USD 8.6 billion by 2025, at a CAGR of 9.0%. Opportunity: Growing healthcare infrastructure across emerging markets; Emerging countries continue to suffer from insufficient healthcare funding, which adversely affects access to healthcare, quality, and, ultimately, the health status of citizens. According to the World Bank, approximately 400 million people lack access to essential healthcare services, mostly in Africa and South Asia. Furthermore, accelerating medical inflation, i.e., the cost of medical treatments and a higher prevalence of non-communicable lifestyle-related diseases such as cancer, diabetes, or cardiac syndromes, have resulted in funding gaps. According to a report published by Geneva Association, in the last two decades, the share of total aggregate global expenditure on healthcare in GDP has increased from about 8% to almost 10%, or an estimated USD 8 trillion per annum, which is driven by the accelerating cost of medical treatment, expanding treatment options and increasing customer demands. Moreover, the Global Burden of Disease Health Financing Collaborator Network (2017) estimates that global spending on health will almost triple to USD 24 trillion by 2040 with upper-middle-income countries are estimated to show the fastest increase at an average of 5.3% per year. This growth could be attributed to continued growth in GDP and the rise of the middle class and government spending. Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=16618331 The Rising target disease population, rapid growth in generic products, rising adoption of self-medication and digitalization, affordable cost with increased efficiency, and technological advancements are the major factors driving the growth of the market. Furthermore, growing initiatives undertaken by leading market players to establish production facilities in both mature and developing markets are the key factors driving the growth of the prefilled syringes industry. The Prefilled Syringes Market includes major Tier I and II suppliers like Becton, Dickinson and Company (US), Gerresheimer (Germany), SCHOTT AG (Germany), and West Pharmaceutical Services, Inc. (US), and Nipro Corporation (Japan). These suppliers have their manufacturing facilities spread across regions such as North America and Europe. COVID-19 has impacted their businesses as well. Routine care for chronic diseases is an ongoing challenge amidst the global COVID-19 pandemic due to the change in routine care to virtual communication. Diabetes, chronic obstructive pulmonary disease, and hypertension were the most impacted conditions due to a reduction in access to care. Furthermore, currently, most global healthcare resources are focused on coronavirus disease (COVID-19), and this resource reallocation is expected to disrupt the continuum of care for patients with chronic diseases. Increasing adoption of self-administered injectable drugs is expected to result in the segment occupying the majority of the market share The conventional Prefilled Syringes Market is estimated to have the largest market share by value. Growth of this segment can be attributed to the the advantages offered, such as safe administration, ease of use for both healthcare professionals and end users, reduced risk of contamination of the product, less waste of costly API, ease of manufacturing, improved dosing accuracy, and enhanced product differentiation when compared to vials is expected to drive the market growth. Request Research Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=16618331 Plastic Prefilled Syringes estimated to be the fastest-growing market Plastic prefilled syringes are estimated to be the fastest-growing segment in the Prefilled Syringes Market. The growth of this segment can be attributed to the rising development of newer polymers (which possess various physical and chemical properties such as high heat & break resistance, tolerance of freeze-drying & liquid nitrogen exposure, high transparency, and solvent resistance. Europe is estimated to be the largest market due to the rising prevalence of chronic diseases, growth of the biologics and biosimilars market, technological advancements, geographical expansion by key manufacturers, aging population, and high adoption of self-injection devices are driving the demand for self-injectable prefilled syringes. Asia Pacific likely to emerge as the largest Prefilled Syringes Market. Asia Pacific is estimated to be the fastest-growing market for prefilled syringes during the forecast period. The Asia Pacific market is driven principally by the increasing demand for self-administered treatments, high penetration of self-injection devices, growing aging population, increasing prevalence of diabetes, and huge patient population. Becton, Dickinson and Company (US), Gerresheimer (Germany), SCHOTT AG (Germany), and West Pharmaceutical Services, Inc. (US) are the key players in the global Prefilled Syringes Market Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=16618331  The Research Report on “Women’s Health Care Market by Drugs (Prolia, Xgeva, Evista, Mirena, Zometa, Reclast, Nuvaring, Primarin, Actonel), Application (Female Infertility, Postmenopausal Osteoporosis, Endometriosis, Contraception, PCOS, Menopause) – Global forecast to 2024″, is projected to reach USD 17.8 billion by 2024 from USD 9.6 billion in 2019, at a CAGR of 13.2% during the forecast period. Market Size Estimation: Both top-down and bottom-up approaches were used to estimate and validate the total size of the women’s healthcare market. These methods were also used extensively to determine the size of various subsegments in the market. The research methodology used to estimate the market size includes the following:

Download PDF Brochure: https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=136585329 Industry Segmentation In Detailed: Prolia is the largest and fastest-growing segment of the market. Based on drug, the women’s healthcare market is segmented into EVISTA, XGEVA, Prolia, Mirena, Zometa, Reclast/Aclasta, Minastrin 24 Fe, NuvaRing, FORTEO, Premarin, ACTONEL, and ORTHO-TRI-CY LO (28). Prolia is the largest and fastest-growing segment of the market. Prolia has shown a considerable year-on-year growth primarily due to increasing unit demand. Prolia has witnessed positive market growth owing to the increasing prevalence of postmenopausal osteoporosis in the US. The postmenopausal osteoporosis segment is expected to grow at the highest CAGR during the forecast period. On the basis of application, the women’s healthcare market is segmented into hormonal infertility, postmenopausal osteoporosis, endometriosis, contraceptives, menopause, PCOS, and other applications. The postmenopausal osteoporosis segment is expected to grow at a higher CAGR during the forecast period. The growing prevalence of postmenopausal osteoporosis and a high risk of osteoporosis fractures are the prime factors that contribute towards the large share of this segment. Furthermore, the focus of pharmaceutical players on providing effective drugs for postmenopausal osteoporosis also supports the growth of this segment. The postmenopausal osteoporosis segment also holds the largest share of the market owing to these factors. Request Sample Pages: https://www.marketsandmarkets.com/requestsampleNew.asp?id=136585329 Leading Key Players and Analysis: The Women’s Health Care Market is fragmented in nature, with a large number of players, including tier 1 and mid-tier companies competing for market shares. The prominent players in the global market include Bayer AG (Germany), Allergan (Dublin), Merck & Co. (US), Pfizer Inc. (US), Amgen (US), Agile Therapeutics Inc. (US), Ferring Pharmaceuticals (US), Mylan N.V. (US), Lupin (India), Blairex Laboratories (US), and Apothecus Pharmaceutical (US). Amgen (US): Amgen (US) is one of the leading providers of the women’s healthcare market. The company’s sales and marketing activities are greatly focused on the US and Europe. The company provides Prolia and Xgeva for the treatment of osteoporosis in postmenopausal women. These drugs have shown a year-on-year double-digit value gain as well as volume growth, and constitute the largest share of the market. Amgen’s EVENITY, meant for the treatment of osteoporosis in postmenopausal women, is also in phase 3 of development. It is being developed in collaboration with UCB (Belgium). The company’s high brand recognition and focus on product innovation have helped it to maintain its foothold in the market. Geographical Analysis in Detailed: The global women’s healthcare market is segmented into five major regions, namely, North America, Europe, APAC, Latin America, and the Middle East & Africa. In 2018, North America (US and Canada) was the largest and the fastest-growing regional market for women’s healthcare. The major factors supporting market growth include the growing prevalence of PCOS and postmenopausal osteoporosis, increasing median age of first-time pregnancies, and increased healthcare spending in the US and Canada. Also, the high awareness and understanding regarding contraceptives among American women and the easy access to modern contraception as compared to developing countries propel the market growth in this region. Speak to Analyst: https://www.marketsandmarkets.com/speaktoanalystNew.asp?id=136585329 |

AuthorResearch Analyst in Healthcare Archives

August 2021

Categories |

RSS Feed

RSS Feed